01

Market Summery

Executive Summary and Global Market Analysis

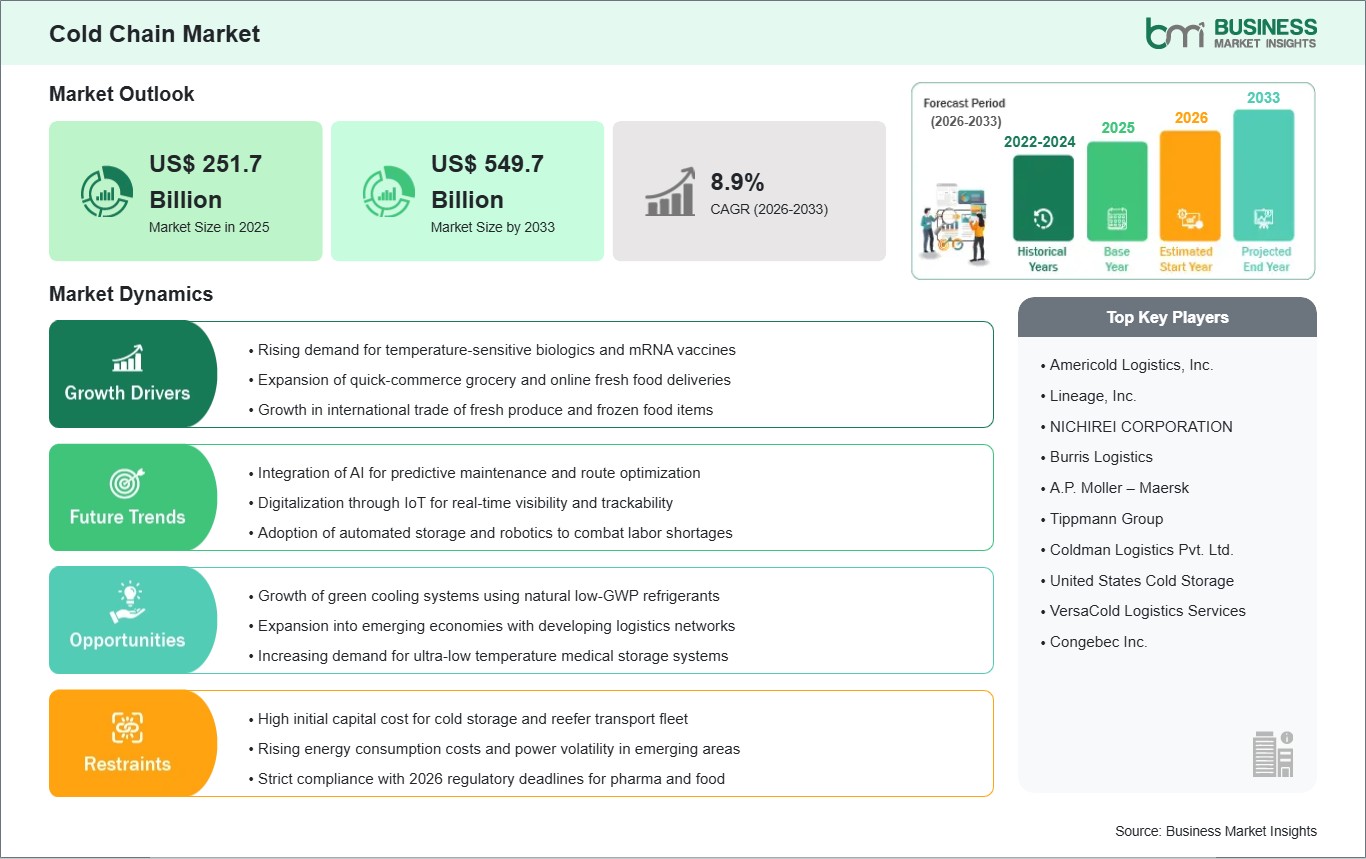

The Cold Chain market encompasses a specialized temperature-controlled supply chain designed to preserve the integrity and shelf life of perishable goods through seamless thermal and logistical management. This system integrates high-performance refrigerated storage, specialized transportation fleets, and sophisticated monitoring components to ensure that products ranging from fresh produce to life-saving biologics remain within strict temperature parameters from production to the final consumer. As global trade for temperature-sensitive items expands, the cold chain has become a critical pillar of modern infrastructure, safeguarding public health and food security.

However, the industry faces significant challenges, including the high capital expenditure required for automated cryogenic storage and the escalating energy costs associated with maintaining sub-zero environments. Technical restraints such as the "last-mile" delivery gap in developing regions and the environmental impact of traditional refrigerants also present hurdles to rapid scaling. Furthermore, fluctuating global trade policies and stringent regulatory compliance for pharmaceutical transport add layers of operational complexity.

Despite these deterrents, the market is rife with lucrative opportunities driven by the rapid digitalization of logistics through IoT and AI-powered predictive analytics. The surge in e-commerce grocery platforms, the global transition toward sustainable "green" cooling technologies, and the rising demand for personalized medicine and mRNA vaccines continue to create high-growth avenues for market participants.

03

Segment Analysis

Cold Chain Market Segmentation

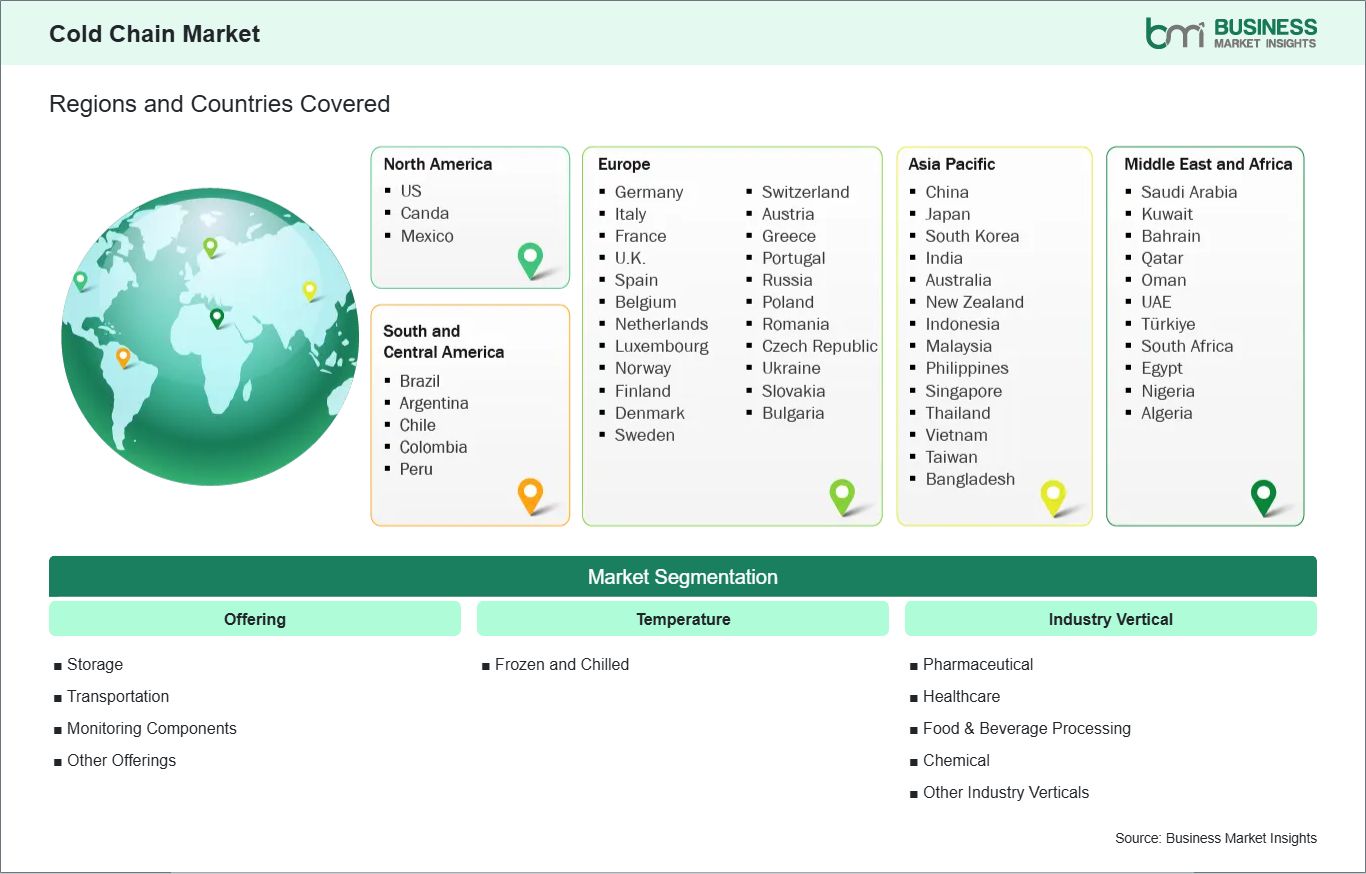

Key segments that contributed to the derivation of the Cold Chain market analysis are offering, temperature, and industry vertical.

- By Offering, the market is segmented into Storage, Transportation, Monitoring Components, and Others.

- By Temperature, the market is divided into Frozen and Chilled.

- By Industry Vertical, the market is categorized into Pharmaceutical, Healthcare, Food &Beverage Processing, Chemical, and Others.

04

Market Forces

Cold Chain Market Drivers and Opportunities

Rising Demand for Biologics and Specialized Pharmaceutical Logistics

A primary driver for the cold chain market is the exponential growth of the biopharmaceutical sector, which increasingly relies on ultra-low temperature storage and transport. Unlike traditional small-molecule drugs, modern biologics, including monoclonal antibodies, cell therapies, and mRNA vaccines, are protein-based and inherently unstable. They are highly sensitive to even minor thermal excursions, which can lead to protein denaturation, loss of potency, or the formation of hazardous degradation products. The global pharmaceutical pipeline is now heavily weighted toward these temperature-sensitive products, necessitating a sophisticated logistical infrastructure that far exceeds standard refrigeration capabilities.

This shift has necessitated a move from standard cooling to precision thermal management within the supply chain. High-value therapeutics demand specialized cryogenic storage and precisely controlled refrigerated environments throughout their entire lifecycle. The rise of personalized medicine and advanced therapy medicinal products further intensifies this demand, as these treatments often require a complex "vein-to-vein" cold chain that must remain unbroken across diverse climates and international borders. Consequently, pharmaceutical companies are aggressively seeking partnerships with logistics providers that offer compliant hubs and high-performance active packaging. This operational imperative to protect sensitive medical products is compelling providers to expand their specialized fleets and warehouse capacities, serving as a sustained catalyst for market growth as healthcare systems prioritize the delivery of advanced biologics.

Integration of AI and IoT for "Smart" Cold Chain Visibility

The emergence of the Artificial Intelligence of Things (AIoT) presents a transformative opportunity for market players to transition from passive cooling to active, intelligent management. Traditional cold chains often suffered from visibility gaps during transit, where temperature deviations were only discovered upon arrival, frequently resulting in the total loss of cargo. By integrating IoT sensors and advanced tracking technologies, operators can now achieve real-time visibility into temperature, humidity, vibration, and location data. When paired with AI-driven predictive analytics, this data allows systems to detect anomalies and anticipate equipment failure or thermal breaches before they occur, allowing for proactive intervention.

The strategic potential of this "Smart Cold Chain" is immense, offering the ability to significantly reduce operational overhead and product waste through optimized energy usage and intelligent route planning. AI algorithms can analyze external environmental factors and logistical data to determine the most efficient delivery paths, ensuring that perishable goods reach their destination well within their viable window. Furthermore, the use of automated intelligence in warehouses enables autonomous decision-making, such as shifting inventory to different thermal zones based on real-time sensor feedback. As companies face increasing pressure to meet sustainability targets and regulatory requirements, AIoT provides the necessary tools to minimize waste and reduce the environmental footprint of refrigeration. This transition toward a data-centric model not only protects product integrity but also allows logistics providers to offer high-value, tech-enabled services in a competitive global economy.

05

Size and Share Analysis

Cold Chain Market Size and Share Analysis

The Cold Chain market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within offering, temperature, and industry vertical, offering insights into their contribution to overall market performance.

Under Offering, the storage sub-segment is currently holding a significant revenue share due to the massive global investment in automated refrigerated warehouses.

Within the temperature category, the frozen sub-segment accounts for a substantial portion of the market, as it remains indispensable for the long-term preservation of meat, seafood, and specific chemical reagents.

Regarding industry verticals, the food & beverage processing sub-segment leads in terms of volume, driven by the global consumption of frozen ready-to-eat meals and the stabilization of perishable produce exports.

07

Report Coverage

Cold Chain Market Report Coverage and Deliverables

The "Cold Chain Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Cold Chain market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Cold Chain market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Cold Chain market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Cold Chain market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Cold Chain Market Geographic Insights

The geographical scope of the Cold Chain market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

In North America, the industry is increasingly focused on the integration of high-level automation and the regionalization of supply networks to mitigate the risks associated with global trade volatility. This transition is supported by a robust framework of specialized logistics hubs that prioritize rapid distribution and high-fidelity monitoring. Across Europe, market activities are heavily steered by rigorous environmental mandates and sustainability initiatives, which have accelerated the adoption of natural refrigerants and the electrification of transportation fleets to meet carbon-neutrality objectives.

The Asia-Pacific region is characterized by extensive infrastructure expansion and the modernization of traditional retail systems, driven by high rates of urbanization and a burgeoning demand for organized food delivery networks. This shift necessitates significant investment in multi-modal cold chain facilities to connect production centers with dense urban populations. In the Middle East & Africa, market growth is anchored by the strategic establishment of smart logistics gateways and the expansion of pharmaceutical-grade storage to support national healthcare security and the distribution of sensitive medical supplies. Meanwhile, South & Central America are prioritizing the enhancement of export-oriented cold chain corridors, utilizing advanced tracking technologies to ensure that agricultural and seafood products meet the stringent quality standards required for international trade. This collective regional progress ensures a resilient global network capable of supporting the increasingly complex requirements of temperature-sensitive commerce.

10

Industry Activity

Recent Developments

The Cold Chain market is evaluated by gathering qualitative and quantitative data post-primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Cold Chain market are:

- In October 2025, Carrier Transicold spotlighted [R]eCool, an innovative electric retrofit solution for Vector® refrigeration units, during the Solutrans exhibition in Lyon. Originally unveiled in 2023 as one of the transport refrigeration industry's first engineless retrofit cooling solutions, the [R]eCool system enabled operators to convert diesel-powered refrigerated units on semi-trailers to hybrid or fully electric operation. This development played a vital role in modernizing the Cold Chain by substantially reducing diesel emissions, lowering fuel expenditures, and minimizing noise levels. By enhancing the value of existing fleets, Carrier Transicold, a part of Carrier Global Corporation, provided a sustainable pathway for logistics providers to maintain high-efficiency Cold Chain operations while adhering to increasingly stringent environmental regulations.

- In January 2025, UPS completed the acquisition of Frigo-Trans and its sister company BPL, both of which provided specialized, complex healthcare logistics solutions across Europe. These acquisitions significantly enhanced the end-to-end capabilities available to UPS Healthcare customers, who increasingly required temperature-controlled and time-critical logistics solutions on a global scale. The Frigo-Trans network featured temperature-controlled warehousing ranging from cryopreservation to ambient storage, alongside a robust Pan-European Cold Chain transportation infrastructure. When combined with the time-critical freight forwarding capabilities of BPL, this development further strengthened the comprehensive Cold Chain solutions offered to healthcare customers across the European market.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

Internet Society CISA International Energy Agency World Bank – Global Trade Indicators World Trade Organization (WTO) International Trade Administration (ITA) Company website Company annual reports Company investor presentations