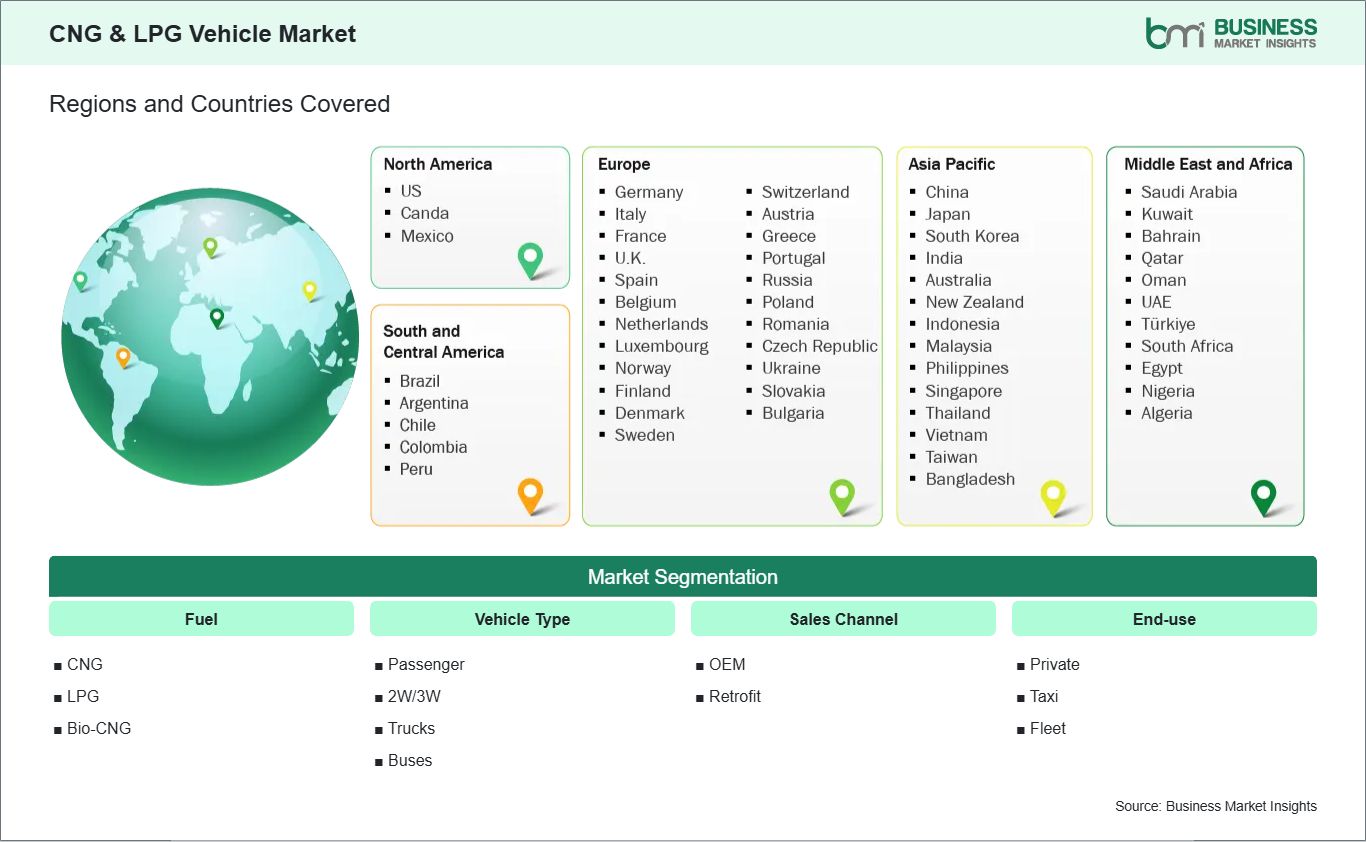

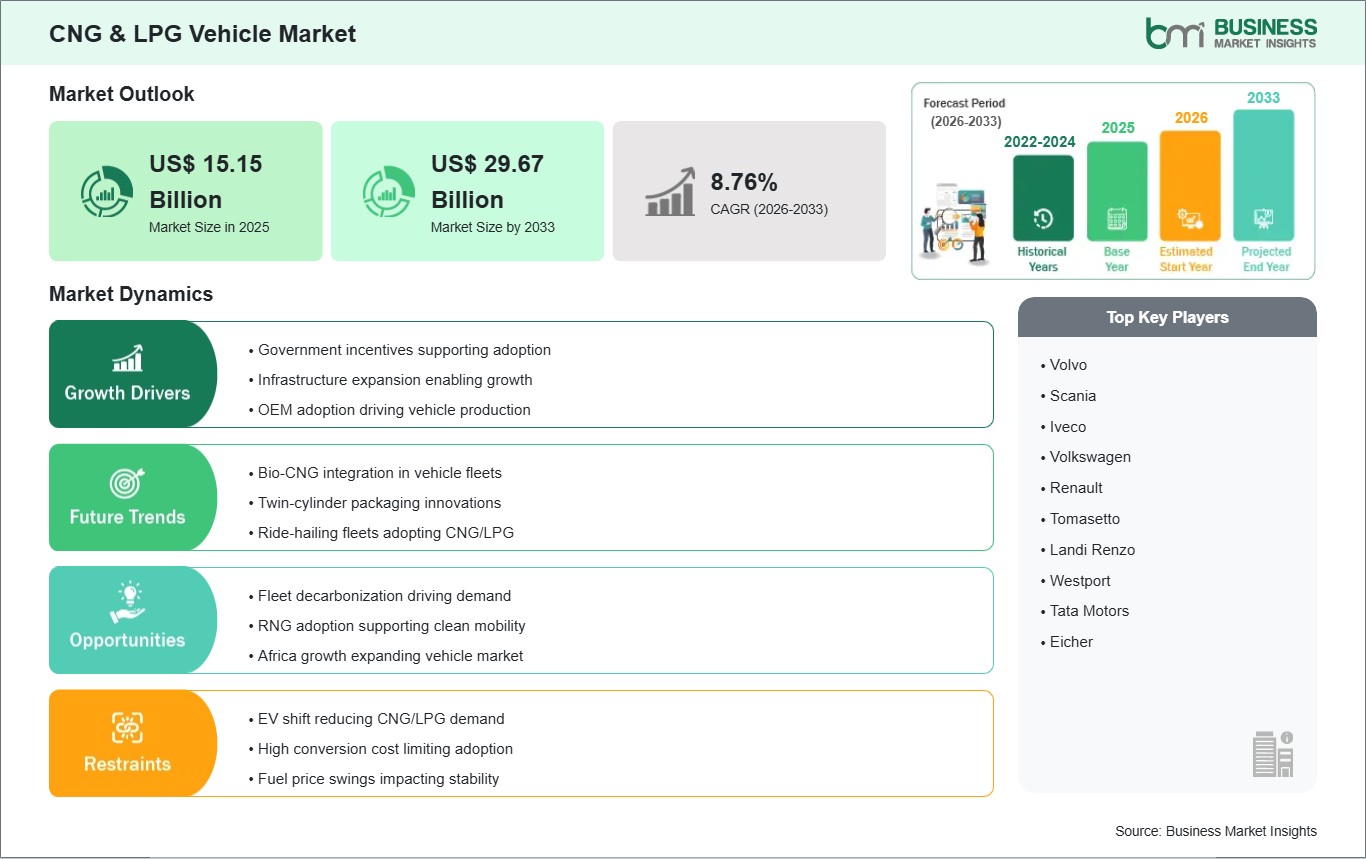

CNG & LPG Vehicle Market Segmentation

The CNG and LPG vehicle market is segmented based on fuel, vehicle type, sales channel, end-use, and cylinder type, reflecting the growing shift toward cleaner and more cost-effective mobility solutions across global transportation systems.

By Fuel

- CNG (Compressed Natural Gas): Dominates adoption due to lower emissions, cost efficiency, and strong government support for cleaner transportation.

- LPG (Liquefied Petroleum Gas): Widely used in passenger and commercial vehicles, offering easy availability and lower conversion cost compared to conventional fuels.

- Bio-CNG: Emerging segment driven by sustainability goals, produced from organic waste and gaining traction as a renewable alternative fuel.

By Vehicle Type

- Passenger Vehicles: Represent a significant share due to increasing adoption of CNG/LPG cars for daily commuting and reduced fuel expenses.

- 2W/3W Vehicles: Growing rapidly, especially in developing markets, supported by affordability and urban mobility needs.

- Trucks: Increasing adoption in logistics and freight transport to reduce operating costs and emissions compliance pressure.

- Buses: Widely deployed in public transportation systems as governments push for cleaner mass transit solutions.

By Sales Channel

- OEM (Original Equipment Manufacturer): Accounts for a major share as manufacturers increasingly offer factory-fitted CNG/LPG vehicles with improved efficiency and safety.

- Retrofit: Continues to grow due to cost advantages, allowing existing petrol vehicles to be converted into CNG/LPG-compatible systems.

By End Use

- Private: Strong demand driven by individual vehicle owners seeking fuel savings and lower emissions.

- Taxi: High adoption due to intensive usage patterns and significant operational cost benefits.

- Fleet: Expanding rapidly with logistics companies and ride-hailing services focusing on cost efficiency and sustainability goals.

By Cylinder Type

- Type I: Full steel cylinders, widely used due to durability and low cost.

- Type II: Steel cylinder with composite wrapping for reduced weight and improved performance.

- Type III: Fully composite cylinders with aluminum liner, offering higher weight reduction and efficiency.

- Type IV: All-composite cylinders with plastic liner, providing maximum weight savings and advanced performance for modern vehicles.