01

Market Summery

Executive Summary and Global Market Analysis

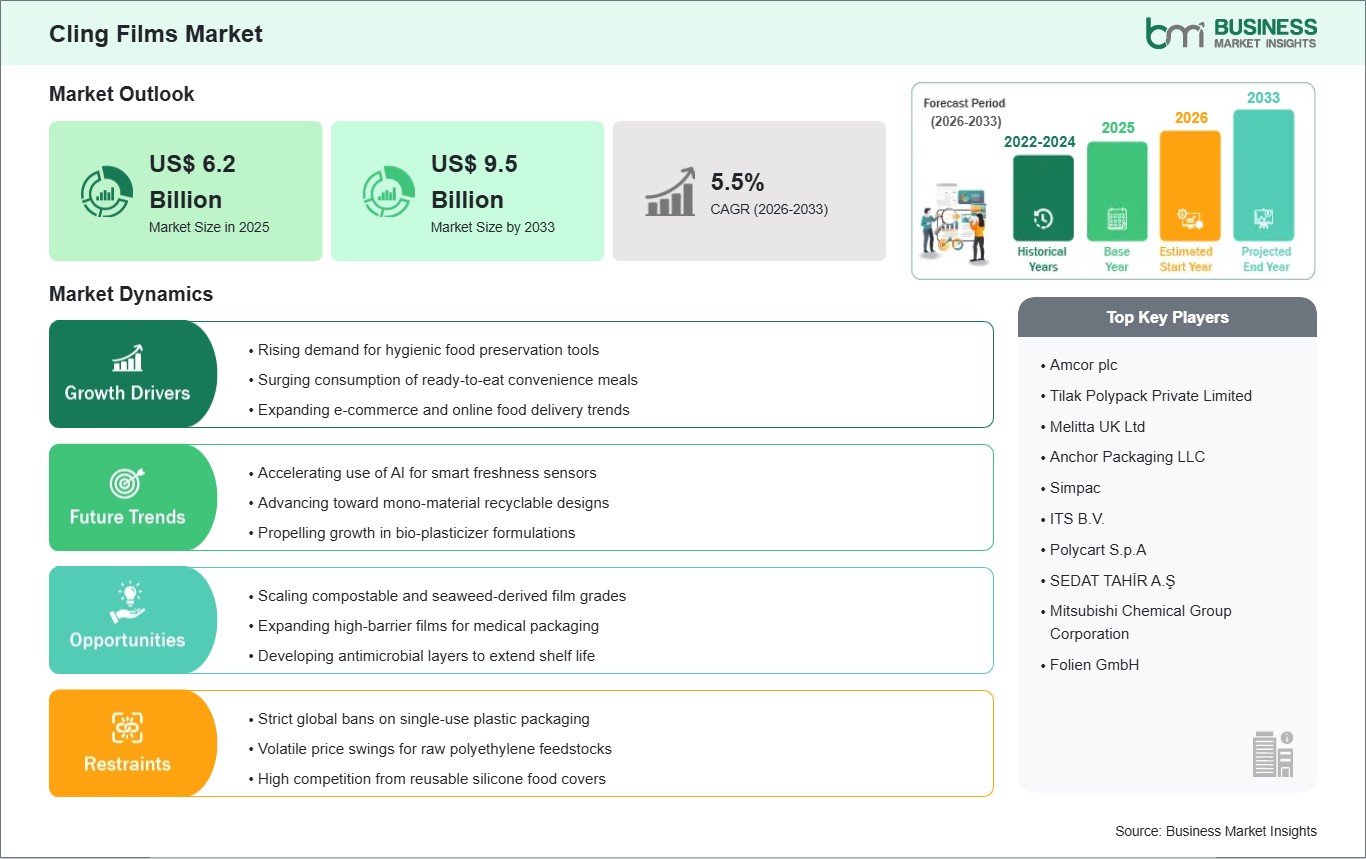

Cling films are considered critical packaging items for preserving goods, both perishable and non-perishable, through a thin, flexible, self-adhering barrier that is used essentially for maintaining freshness. They find their applications across several verticals, including the food and beverages industry, healthcare, consumer goods, and industrial logistics. Some of the key benefits associated with cling films are high transparency that provides excellent product visibility, good puncture resistance, and the ability to provide tight seals that avoid contamination and loss of moisture. Driving factors include growing demand globally for packaged food, expansion of organized retail, and increasing consumer awareness related to food hygiene and shelf-life extension. Besides, material science innovations, such as high-barrier nanocomposites and antimicrobial films, are improving service efficiency and reliability.

However, fluctuating prices for petroleum-based raw materials, increasing environmental regulations related to single-use plastics, and increasing energy prices in manufacturing could restrict market growth. The industry also suffers greatly from economic cycles, as well as the transition into reusable alternatives. Despite these challenges, the market holds lucrative opportunities driven by increased demand for biodegradable and compostable films, expansion in the network for food delivery in developing countries, and increased adoption of supply chain management on digital platforms for packaging inventory. Other than this, investment in bio-based polymers and sustainable manufacturing processes will also open new opportunities for market growth.

03

Segment Analysis

Cling Films Market Segmentation

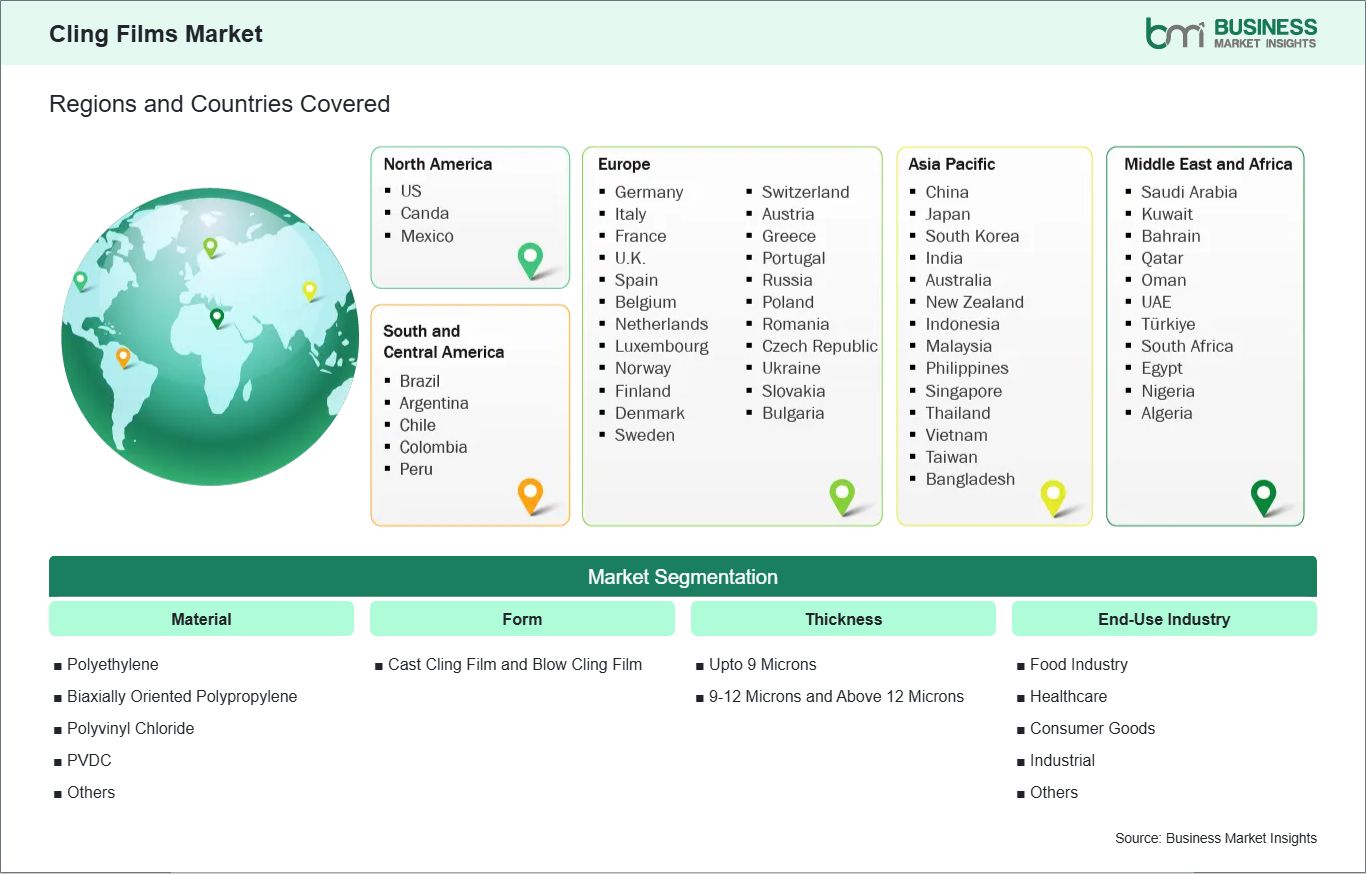

Key segments that contributed to the derivation of the Cling Films market analysis are material, form, thickness, and end-use industry.

- By Material, the market is segmented into Polyethylene (High-Density Polyethylene, Low-Density Polyethylene, Linear Low-Density Polyethylene, and Ultra-Low Density Polyethylene), Biaxially Oriented Polypropylene, Polyvinyl Chloride, PVDC, and Others.

- By Form, the market is segmented into Cast Cling Film and Blow Cling Film.

- By Thickness, the market is segmented into Up to 9 Microns, 9–12 Microns, and Above 12 Microns.

- By End-Use Industry, the market is segmented into Food Industry (Bakery and Confectionery, Meat Poultry and Seafood, Dairy Products, Fruits and Vegetables, and Others) Healthcare, Consumer Goods, Industrial, and Others.

04

Market Forces

Cling Films Market Drivers and Opportunities

Rising Demand for Food Safety and Waste Reduction

The rapid growth of the global food retail and processing sectors has emerged as a pivotal factor positively driving the cling films market. With urbanization and the increasing preference for ready-to-eat and convenience foods, consumers and retailers alike require effective packaging solutions to prevent contamination and extend product longevity. Cling films provide a cost-effective method for sealing fresh produce and proteins, which is essential for meeting modern food safety standards.

For instance, according to the Food and Agriculture Organization (FAO), approximately one-third of all food produced globally is lost or wasted, highlighting a critical need for preservation technologies. Cling films, by providing an airtight and moisture-resistant barrier, directly address these concerns by reducing spoilage during transit and storage. This robust expansion in food safety requirements directly supports the growth of the cling films market as the need for hygienic, efficient global packaging solutions continues to increase to meet consumer expectations and supply chain demands worldwide.

Development of Sustainable and Bio-based Film Solutions

The ongoing shift toward environmental sustainability has become a powerful opportunity for growth in the cling films market. As international regulations on single-use plastics become more stringent and global supply chains focus on "green" logistics, businesses are increasingly seeking biodegradable and recyclable alternatives to traditional PVC and PE films. Air-permeable but compostable films, derived from renewable resources like corn starch or PLA, have emerged as a crucial enabler of this transition.

In recent years, trade liberalization and environmental policies have encouraged the flow of eco-friendly packaging materials between developed and emerging economies. High-value, sustainable cling films are increasingly sought after in the European and North American markets due to strict plastic waste directives. Moreover, multinational companies are diversifying their packaging strategies to include bio-based materials to remain resilient in the face of changing environmental laws. This shift involves the need for advanced material solutions that can support complex, time-critical supply chains while minimizing carbon footprints. As companies adapt to circular economy models and sustainable inventory practices, the demand for innovative, eco-friendly cling films is expected to grow steadily.

05

Size and Share Analysis

Cling Films Market Size and Share Analysis

The cling films market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within material, form, thickness, and end use industry, offering insights into their contribution to overall market performance.

For instance, Polyvinyl Chloride films are dominating the market because of their clarity and stretching properties. But Polyethylene films with advanced recyclable properties and safety for home usage tend to acquire a loyal consumer base. Polypropylene films have biodegradable properties and find their uses in industrial applications.

The cast cling films are usually employed in high-speed industrial processing, requiring a certain level of transparency along with a uniform thickness. This type is very commonly employed in different sectors because of the efficient production process accompanied by large-scale processing capabilities.

The medical and healthcare industry employs specific cling films that are used to wrap medical devices. This segment benefits from increasing global healthcare standards and the rising demand for tamper-evident packaging in clinical environments.

07

Report Coverage

Cling Films Market Report Coverage and Deliverables

The "Cling Films Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Cling Films market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Cling Films market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Cling Films market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Cling Films market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Cling Films Market Geographic Insights

The geographical scope of the Cling Films market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

Asia-Pacific is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. Asia-Pacific is experiencing robust growth, driven by the rapid expansion of organized retail, growing international food trade volumes, and the rising demand for packaged convenience foods. Major economies like China and India are leading the way, fueled by increasing industrial output, strategic logistics investments, and the development of large-scale food processing zones.

The region is also witnessing increased adoption of advanced packaging technologies, including antimicrobial and anti-fog films, particularly relevant for the fruits and vegetables and meat poultry segments. Cling film capacity expansion, alongside manufacturing modernization efforts by regional players, is enhancing operational efficiency and reducing costs. Additionally, the surge in manufacturing activity and exports, coupled with the growth of modern supermarkets, is positioning Asia-Pacific as a key hub in the global flexible packaging ecosystem. The rise of regional trade agreements and strong infrastructure development across major logistics corridors further solidifies the region’s dominant market position. North America is driven by mature food processing industries and high demand for hygienic, ready-to-eat packaging in the US.

10

Industry Activity

Recent Developments

The Cling Films market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the cling films market are:

- In October 2025, RecyClass approved that Multilayer Films containing Mitsubishi Chemical’s SoarnoL™ ethylene-vinyl alcohol copolymer (EVOH) resins are fully compatible with Polyethylene (PE) flexibles recycling. This approval applies to multi-layer PE films containing ≤10 weight percent (wt%) SoarnoL™, and to multi-layer PE films containing up to 3 wt% Soaresin™, which is a special recycling compatibilizer designed for use in EVOH multi-layer packaging.

- In April 2024, Berry Global Group, Inc. announced the acquisition of F&S Tool, a specialized provider of high-output, high-efficiency hot runner injection and high-volume compression molding applications. F&S Tool operates a 90,000 square foot facility located in Erie, Pennsylvania, with 11 issued/pending patents and 105 dedicated employees focused on disruptive technologies to serve a broad spectrum of plastics manufacturers. This acquisition will further enhance Berry’s global tooling capability and bring proprietary technologies in the closures and bottles space, specifically targeting high-end growth markets.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations