01

Market Summery

Executive Summary and Global Market Analysis

Catalytic converter systems refer to exhaust treatment assemblies that convert harmful gases into less toxic emissions. This technology works using reactions that are brought about by a chemically coated substrate in exhaust channels. Stringent emission regulations have increased the degree of incorporation within automotive manufacturing environments. The shift towards electrified vehicles continues to fuel the need for emission control systems that work with hybrids. Urban freight growth further bolsters installation within different types of vehicles.

Diversification of the product line arises from its widespread use in both passenger cars and commercial trucks. Material choice varies depending on efficiency and regulatory standards. There is also demand arising from diesel after-treatment systems in heavy-duty vehicles. Improved substrate and thermal designs improve efficiency.

Intense competition results from engineering specialization and regulatory compatibility. The emphasis is placed on material optimization and increased durability of products. The innovation stream revolves around efficiency in emission reduction and lifecycle performance consistency.

03

Segment Analysis

Catalytic Converter Systems Market Segmentation

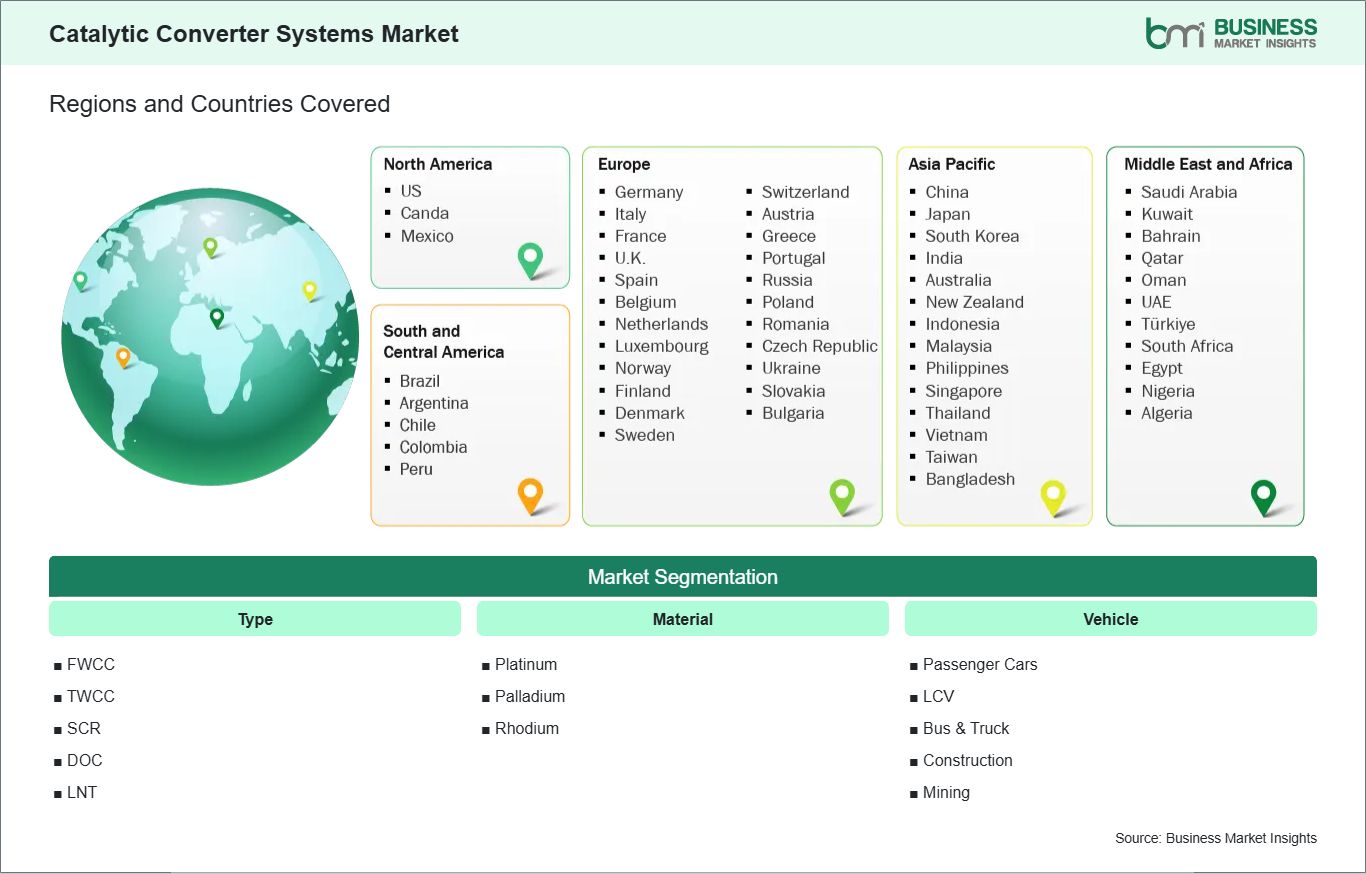

The catalytic converter systems market is segmented based on type, material, and vehicle, reflecting the increasing deployment of emission control technologies to meet stringent regulatory thresholds and improve exhaust treatment efficiency across automotive applications.

By Type

- FWCC - Supports full-flow catalytic conversion for balanced emission reduction across mixed operating conditions.

• TWCC - Enables dual-stage reaction pathways improving oxidation and reduction efficiency in exhaust streams.

• SCR - Utilizes selective catalytic reduction to significantly lower nitrogen oxide emissions in diesel systems.

• DOC - Facilitates oxidation of carbon monoxide and hydrocarbons in gasoline and diesel exhaust.

• LNT - Stores and periodically reduces nitrogen oxides under lean engine combustion conditions.

By Material

- Platinum - Enhances oxidation efficiency and thermal resistance in high-temperature exhaust environments.

• Palladium - Optimized for hydrocarbon conversion, particularly in gasoline engine applications.

• Rhodium - Provides strong nitrogen oxide reduction performance under variable load conditions.

By Vehicle

- Passenger Cars - Represents the largest adoption base driven by mass regulatory compliance requirements.

• LCV - Balances emission performance with cost efficiency in urban logistics operations.

• Bus and Truck - Requires high-durability systems for continuous heavy-load emission control.

• Construction - Supports emission reduction in off-road machinery operating under harsh conditions.

• Mining - Ensures robust exhaust treatment performance in extreme particulate-intensive environments.

04

Market Forces

Catalytic Converter Systems Market Drivers and Opportunities

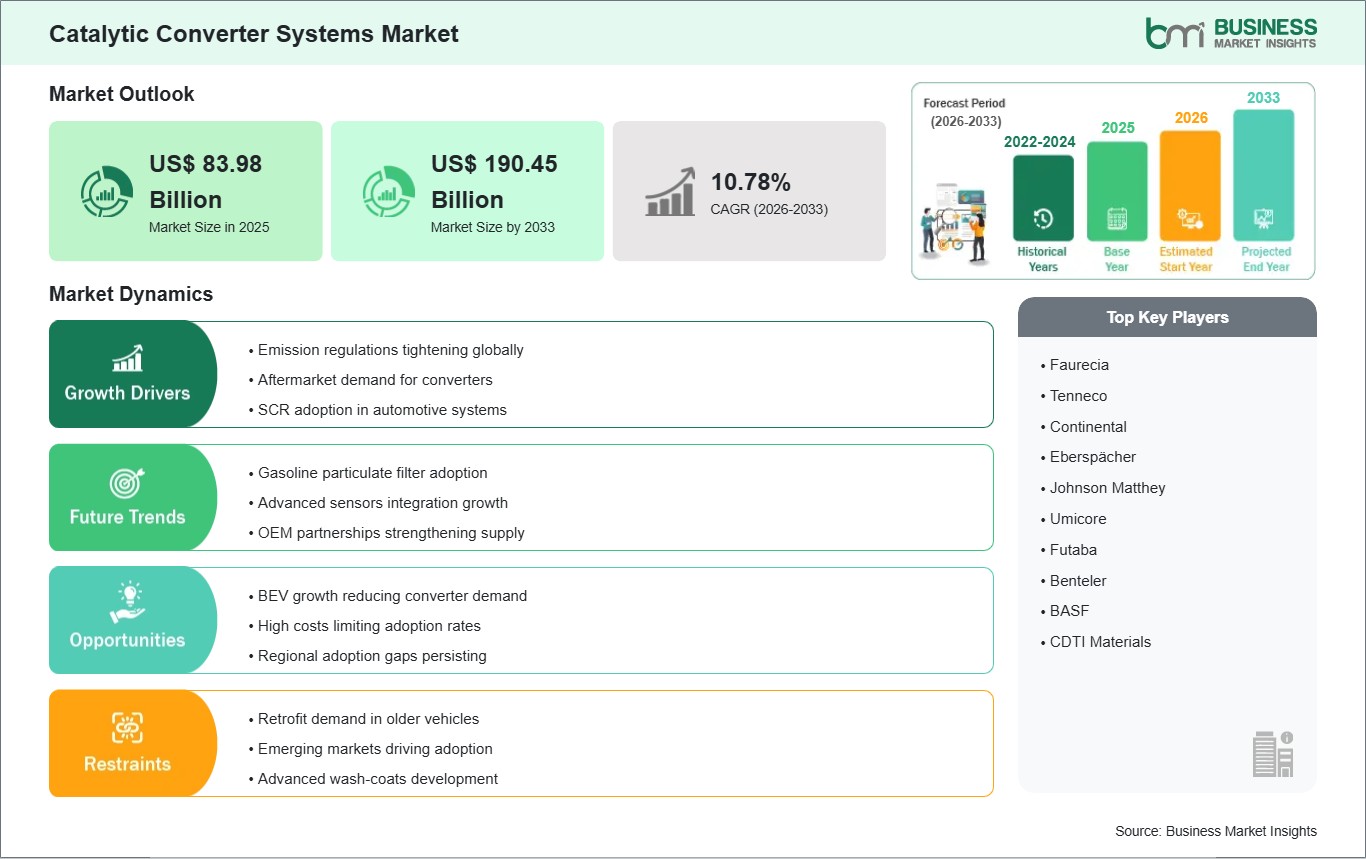

Emission regulations tightening globally

Governments across major automotive markets continue to strengthen emission control frameworks, compelling manufacturers to integrate advanced catalytic converter systems. This rule does not apply to just passenger vehicles but also extends to heavy-duty trucks, buses, and even industrial vehicles. Such standards have made it necessary for converter technologies that can effectively remove hydrocarbons, carbon monoxide, and nitrogen oxide in one step. In order to achieve compliance, there has been an upsurge in innovation and improvements in technology in terms of making better catalysts and substrates that are durable and effective in their work.

The significance of the regulations also comes from how they affect industry priorities in many ways. Apart from being required to comply with such laws, they have an effect on research and development efforts, materials that will be used, and even the supply chains of various organizations. The metals platinum, palladium, and rhodium still hold great importance in the development process of a catalytic converter, but the focus is now on using the metals efficiently and balancing costs and efficiency. Geographical variations also provide different approaches to this, with North America and Europe concentrating on highly developed systems whereas the Asia-Pacific region focuses on cost-efficient technology.

Retrofit demand in older vehicles

The installation of catalytic converters in old automobiles is becoming a viable approach. There are various fleets around the world whose cars were built before the enactment of emission regulations. With the use of catalytic converters, these companies will be able to maximize the life of the cars while ensuring that their emission levels meet the set standards. The adoption of such measures is facilitating innovations that enable converters to be installed into various engines.

Moving forward, it is anticipated that the demand for retrofitting will grow further because many cities will be imposing low emission areas and strict testing requirements. Fleets from the logistics, mining, and construction sectors may turn to retrofitting to stay flexible but avoid being penalized. Retrofitting will create opportunities for niche service providers and suppliers of aftermarket products, offering an additional way for the industry to grow. The effect will have two sides to it - the environmental advantage because of lowering emissions and the economic benefit of prolonging the usefulness of vehicles.

05

Size and Share Analysis

Catalytic Converter Systems Market Size and Share Analysis

The Catalytic Converter Systems Market is projected to grow from US$ 83.98 Billion in 2025 to US$ 190.45 Billion by 2033 , registering a CAGR of 10.78% from 2026 to 2033. The market expansion is supported by stringent emission compliance requirements, rising vehicle production volumes, and increasing integration of advanced exhaust after-treatment systems across global automotive manufacturing ecosystems.

By type, SCR systems account for a significant share due to their high efficiency in reducing nitrogen oxide emissions in diesel engines. DOC units maintain a strong position driven by widespread application in diesel oxidation processes across passenger and commercial vehicles. TWCC and FWCC systems sustain steady adoption, supported by compact design suitability and balanced emission control performance in modern vehicle platforms. LNT systems contribute a smaller but essential share in lean-burn engine configurations requiring advanced NOx trapping capability.

By material, palladium holds a dominant share supported by its strong catalytic activity in gasoline-based systems and cost-efficient performance characteristics. Platinum maintains a substantial position due to its durability and high-temperature oxidation stability across diesel applications. Rhodium remains critical despite lower volume usage, driven by its superior nitrogen oxide reduction efficiency in stringent emission environments.

By vehicle, passenger cars represent the leading share due to large-scale production volumes and continuous adoption of emission-compliant engine systems. Bus and truck segments maintain strong presence driven by regulatory enforcement across commercial transport fleets. LCV applications contribute steadily through logistics and delivery network expansion, while construction and mining vehicles sustain demand based on heavy-duty operational requirements and off-road emission compliance needs.

07

Report Coverage

Catalytic Converter Systems Market Report Coverage and Deliverables

The "Catalytic Converter Systems Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- The market size and forecast at global, regional, and country levels for all market segments covered under the scope

- The market trends, as well as drivers, restraints, and opportunities

- The market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Catalytic Converter Systems Market Geographic Insights

The catalytic converter systems market shows diverse regional adoption patterns influenced by evolving regulatory environments and transportation infrastructure maturity levels.

Adoption patterns around the world depend on how strictly emissions are enforced and how quickly industries develop. Highly developed nations exhibit well-planned adoption with the help of rigorous enforcement mechanisms. Newer economies exhibit slower adoption due to transportation system modernization.

North America is characterized by systematic enforcement of regulations driving system penetration on a wide scale within different types of vehicles. Cycles of technological advancement are further fueling upgrade requirements among older systems.

Asia Pacific demonstrates strong manufacturing concentration supporting large-scale system integration across vehicles. Expanding urban mobility and industrial activity are reinforcing emission control adoption. Infrastructure expansion continues influencing system deployment intensity.

Europe emphasizes strict emission compliance standards driving advanced catalytic adoption across all vehicle segments. Emerging regions in Latin America and Africa are gradually increasing integration supported by regulatory alignment and fleet renewal programs.

10

Industry Activity

Recent Developments

The catalytic converter systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the catalytic converter systems market are:

- In July 2022, Eberspacher, announced the opening of its new Purem production facility in Louisville, USA, expanding its diesel exhaust aftertreatment manufacturing footprint to support rising demand for emission control systems.

- In October 2023, Cummins Inc., announced that it completed the acquisition of select FORVIA Faurecia exhaust aftertreatment manufacturing plants in Indiana (USA) and Roermond (Netherlands), strengthening its emission solutions business.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

International Energy Agency (IEA) United States Environmental Protection Agency (US EPA) European Environment Agency (EEA) Ministry of Road Transport and Highways (MoRTH), India Society of Indian Automobile Manufacturers (SIAM) International Organization of Motor Vehicle Manufacturers (OICA) United Nations Environment Programme (UNEP) World Bank - Transport and Environment Data Repositories