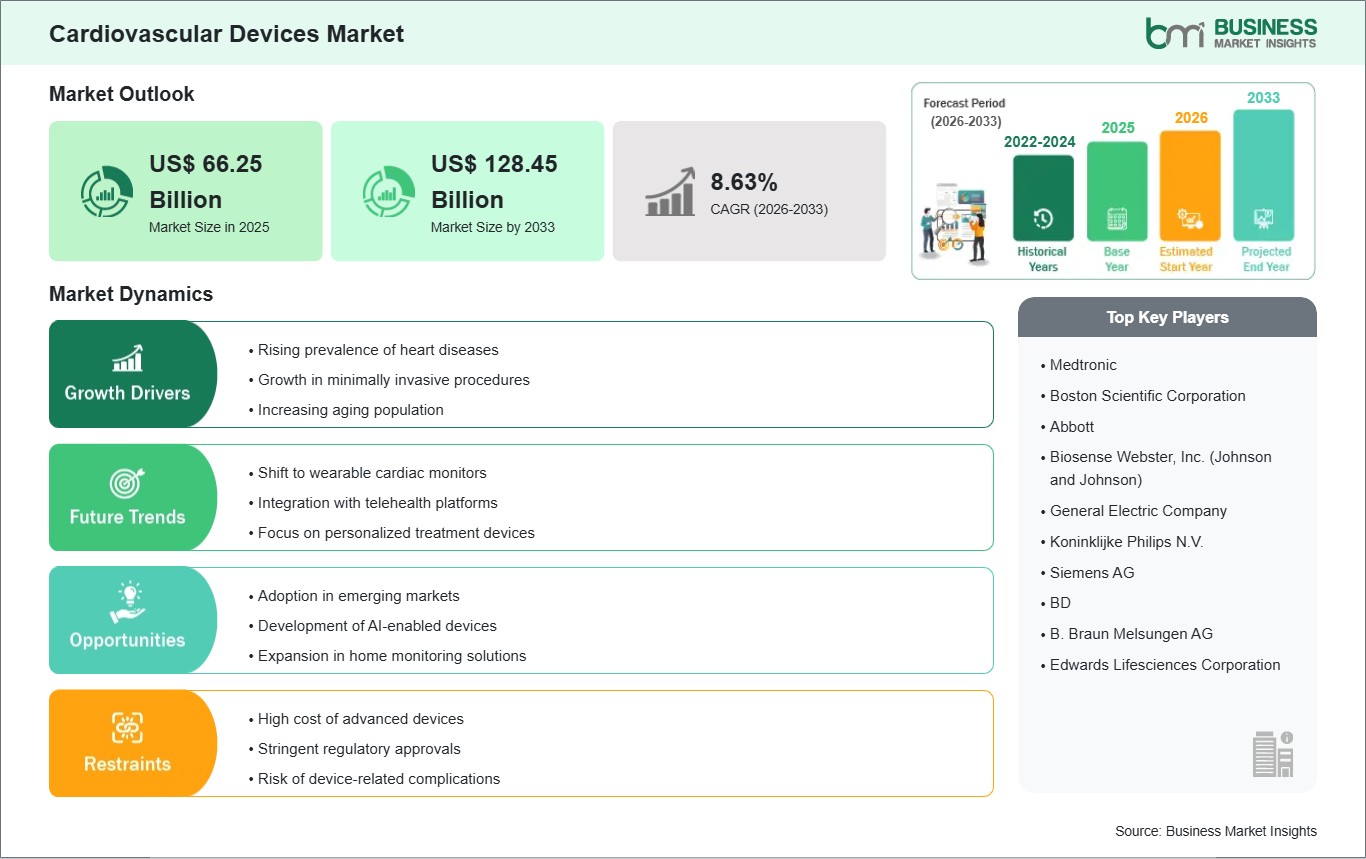

The Cardiovascular Devices Market size is expected to reach US$ 128.45 Billion by 2033 from US$ 66.25 Billion in 2025. The market is estimated to record a CAGR of 8.63% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Cardiovascular devices encompass diagnostic, monitoring, and interventional solutions used to detect, manage, and treat heart and vascular conditions. The portfolio ranges from ECGs, cardiac ultrasound, and CT imaging software to implantable pacemakers/ICDs, stents, ablation catheters, transcatheter valves, and structural heart innovations, enabling minimally invasive therapies and continuous patient monitoring across care settings. As cardiovascular disease remains the leading cause of mortality worldwide, demand for devices that improve workflow efficiency, precision, and patient outcomes continues to rise, buoyed by aging populations, expanding transcatheter eligibility, and AI-enabled imaging and automation.

Despite the rising graph, there are numerous challenges and restraints in the market. First, regulatory complexity for high-risk implantables and novel energy modalities (e.g., pulsed field ablation, transcatheter replacements) requires rigorous clinical evidence and post-market surveillance. Second, cost and reimbursement variability can limit the adoption of advanced devices (e.g., TAVR/TMVR, leadless pacing) in lower-income regions. Lastly, operational constraints stemming from staff shortages and the need for accelerated training in cath labs and echo suites, even as case volumes for structural heart and electrophysiology procedures expand.

Despite these headwinds, lucrative opportunities persist, rapid uptake of AI-enhanced cardiology (automation in echo/CT, autonomous imaging workflows), next-generation transcatheter valves across mitral and tricuspid positions, wearable and handheld diagnostics for earlier detection, and software-driven planning tools that improve decision-making and reduce unnecessary invasive diagnostics. Vendors investing in integrated hardware–software platforms, clinical evidence, and scalable manufacturing are well-positioned to capture share across imaging, electrophysiology, interventional cardiology, and structural heart therapies.

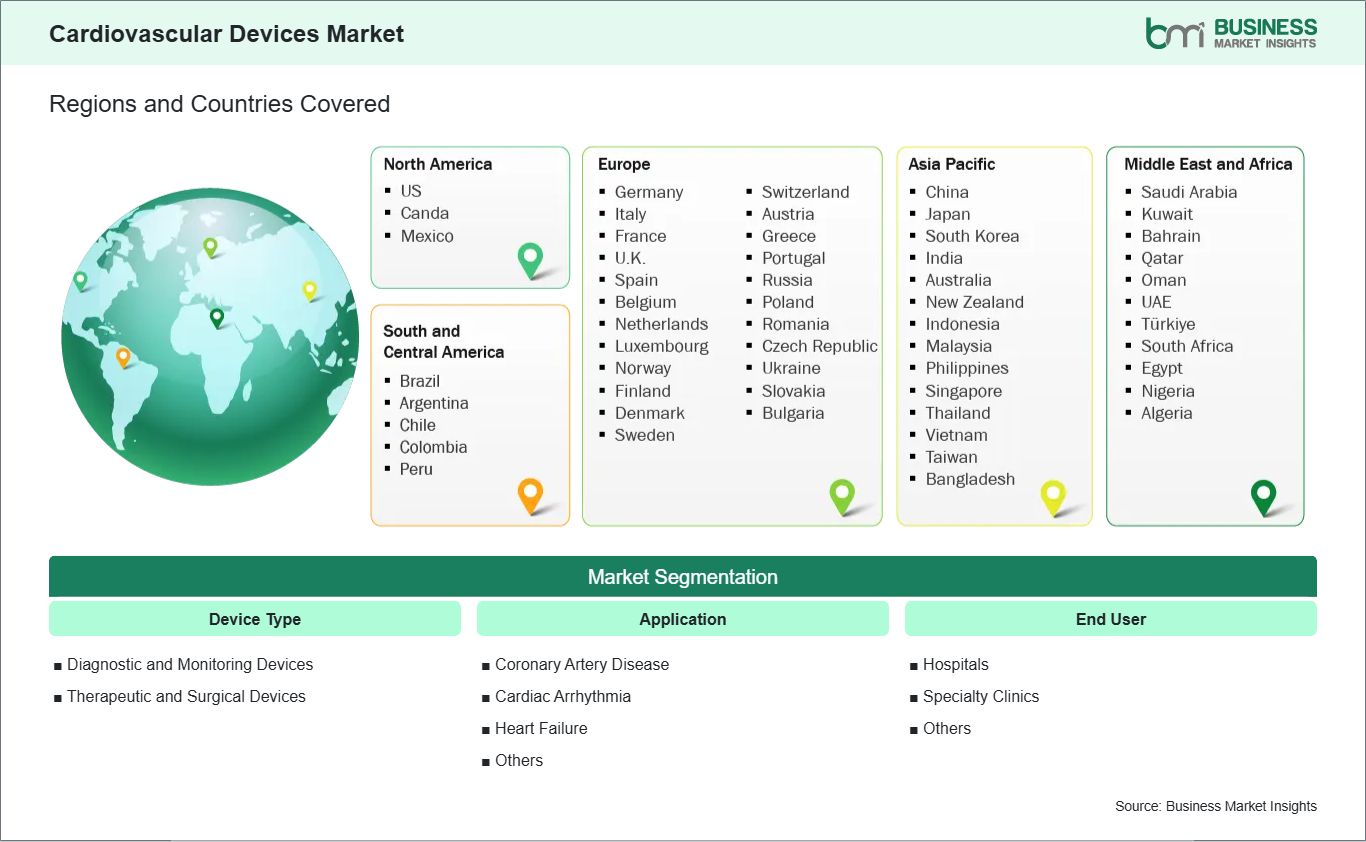

Key segments that contributed to the derivation of the Cardiovascular Devices market analysis are device type, application, and end user.

By Device Type, the market is segmented into Diagnostic and Monitoring Devices (Electrocardiogram, Remote Cardiac Monitoring, and Others) and Therapeutic and Surgical Devices (Ventricular Assist Devices, Cardiac Rhythm Management Devices, Catheters, Stents, Heart Valves, and Others).

By Application, the market is segmented into Coronary Artery Disease, Cardiac Arrhythmia, Heart Failure, and Others.

By End User, the market is segmented into Hospitals, Specialty Clinics, and Others.

Cardiovascular Devices Market Drivers and Opportunities:

Rising Prevalence of Cardiovascular Diseases

Cardiovascular diseases continue to be the leading cause of mortality worldwide, a trend that shows no signs of slowing down as populations age and lifestyle-related risk factors become more prevalent. Sedentary behavior, unhealthy dietary patterns, rising obesity rates, and the increasing global burden of diabetes all contribute to the steady expansion of cardiac conditions. As a result, healthcare systems across both developed and emerging markets are experiencing persistent pressure to enhance their cardiovascular care capabilities.

This growing epidemiological burden is fueling sustained demand for a wide range of diagnostic and therapeutic medical devices. Traditional tools such as ECG machines and Holter monitors remain essential, while remote patient monitoring technologies are becoming increasingly important for continuous assessment and early detection of abnormalities. On the interventional side, minimally invasive products—including drug-eluting stents, implantable cardiac devices, and transcatheter heart valves—are seeing rapid adoption due to their ability to reduce recovery times and improve patient outcomes.

Hospitals and clinics are placing greater emphasis on preventive care, early diagnosis, and advanced therapeutic solutions, which in turn drives investment in innovative devices and integrated digital platforms. Collectively, these factors ensure a strong and resilient foundation for market growth across all global regions.

Expansion of Minimally Invasive and Transcatheter Therapies

The shift toward less invasive procedures represents one of the most significant and lucrative growth avenues within the cardiovascular devices market. As healthcare providers increasingly favor approaches that minimize trauma and accelerate recovery, technologies such as transcatheter aortic valve replacement (TAVR), transcatheter mitral and tricuspid repair or replacement, and emerging modalities like pulsed field ablation (PFA) for atrial fibrillation are fundamentally reshaping clinical practice. These innovations allow cardiologists and cardiac surgeons to treat complex structural heart conditions without the need for open-heart surgery, greatly reducing perioperative risks and postoperative complications.

One of the most notable advantages of these minimally invasive solutions is their ability to expand treatment eligibility to high-risk and elderly patients who were previously considered unsuitable for traditional surgical interventions. This not only improves patient outcomes but also significantly increases the addressable market for device manufacturers. Furthermore, the integration of AI-driven imaging, pre-procedural planning, and real-time navigation tools enhances procedural precision, shortens procedure times, and contributes to better long-term outcomes. Together, these advancements open substantial new revenue opportunities for companies investing in structural heart and electrophysiology portfolios, reinforcing the sector’s strong growth trajectory.

Cardiovascular Devices Market Size and Share Analysis:

The Cardiovascular Devices market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within device type, application, and end user, offering insights into their contribution to overall market performance.

For instance, within device type, therapeutic and surgical devices, particularly heart valves, are gaining traction as transcatheter solutions expand beyond aortic into mitral and tricuspid positions, supported by clinical evidence and improved delivery systems. In terms of application, cardiac arrhythmia stands out due to the rising adoption of advanced ablation technologies, including pulsed field ablation, and next-generation cardiac rhythm management devices that enable safer, faster procedures. Among end users, hospitals remain the primary setting for complex interventions and integrated care, leveraging hybrid operating rooms and advanced imaging suites to support structural heart and electrophysiology procedures.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Medtronic

Boston Scientific Corporation

Abbott

Biosense Webster, Inc. (Johnson and Johnson)

General Electric Company

Koninklijke Philips N.V.

Siemens AG

BD

B. Braun Melsungen AG

Edwards Lifesciences Corporation

Get more information on this report

Cardiovascular Devices Market Report Coverage and Deliverables:

The Cardiovascular Devices Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

Cardiovascular Devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Cardiovascular Devices market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Cardiovascular Devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Cardiovascular Devices market

Detailed company profiles, including SWOT analysis

The geographical scope of the Cardiovascular Devices market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

North America continues to advance with strong adoption of AI-enabled imaging and transcatheter therapies, supported by robust clinical infrastructure and regulatory clarity. Europe emphasizes compliance with evolving MDR standards while accelerating investments in structural heart and electrophysiology solutions. Asia Pacific is witnessing rapid growth in cath-lab installations and minimally invasive procedures, driven by expanding healthcare access and vendor partnerships. The Middle East & Africa is focusing on capacity-building initiatives and collaborations to improve diagnostic imaging and interventional capabilities. South & Central America is modernizing cardiovascular care through infrastructure upgrades and training programs, enabling broader access to advanced therapies.

Get more information on this report

Cardiovascular Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the Cardiovascular Devices market across device type, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Cardiovascular Devices market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Cardiovascular Devices market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Cardiovascular Devices market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Cardiovascular Devices market segments by device type, application, end user, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Cardiovascular Devices market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Cardiovascular Devices Market News and Key Development:

The Cardiovascular Devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Cardiovascular Devices market are:

In July 2025, Boston Scientific Corporation received U.S. Food and Drug Administration (FDA) approval to expand the instructions for use (IFU) labeling for the FARAPULSE™ Pulsed Field Ablation (PFA) System.

In December 2025, Edwards Lifesciences announced that the company's SAPIEN M3 mitral valve replacement system is the first transcatheter therapy utilizing a transseptal approach to receive U.S. Food and Drug Administration (FDA) approval for the treatment of mitral regurgitation (MR).

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Cardiovascular Devices Market

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Cardiovascular Devices Market?

The Cardiovascular Devices Market is valued at US$ 66.25 Billion in 2025, it is projected to reach US$ 128.45 Billion by 2033.

What is the CAGR for Cardiovascular Devices Market by (2026 - 2033)?

As per our report Cardiovascular Devices Market, the market size is valued at US$ 66.25 Billion in 2025, projecting it to reach US$ 128.45 Billion by 2033. This translates to a CAGR of approximately 8.63% during the forecast period.

What segments are covered in this report?

The Cardiovascular Devices Market report typically cover these key segments-

Device Type (Diagnostic and Monitoring Devices [Electrocardiogram (ECG), Remote Cardiac Monitoring, Others], Therapeutic and Surgical Devices [Ventricular Assist Devices (VAD), Cardiac Rhythm Management (CRM) Devices, Catheters, Stents, Heart Valves, Others])

What is the historic period, base year, and forecast period taken for Cardiovascular Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Cardiovascular Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Cardiovascular Devices Market?

The Cardiovascular Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic

Boston Scientific Corporation

Abbott

Biosense Webster, Inc. (Johnson and Johnson)

General Electric Company

Koninklijke Philips N.V.

Siemens AG

BD

B. Braun Melsungen AG

Edwards Lifesciences Corporation

Who should buy this report?

The Cardiovascular Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Cardiovascular Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Cardiovascular Devices Market

Get Free Sample For Cardiovascular Devices Market