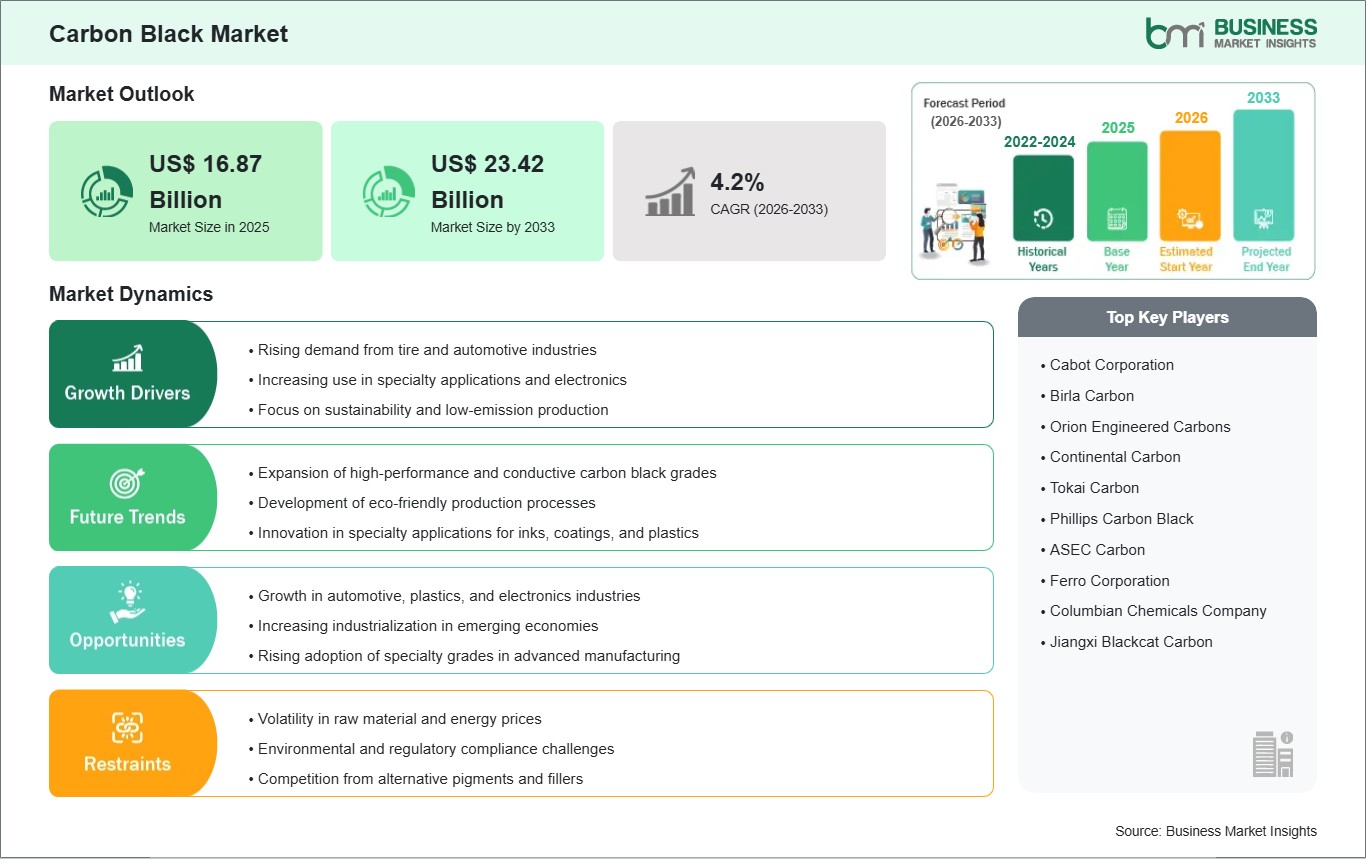

The Carbon Black Market size is expected to reach US$ 23.42 Billion by 2033 from US$ 16.87 Billion in 2025. The market is estimated to record a CAGR of 4.19% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global carbon black market is expanding steadily due to rising demand from automotive, plastics, and coatings industries. Carbon black is a reinforcing agent in rubber, pigment in inks and coatings, and filler in plastics. Growth in tire production, automotive components, and industrial plastics is fueling demand globally.

Advancements in furnace, thermal, and acetylene production processes improve product consistency, particle size, and performance. Specialty grades with enhanced surface area, conductivity, and pigment properties are increasingly used in high-performance applications such as conductive plastics, electronics, and advanced coatings.

Regulatory emphasis on sustainable production, environmental safety, and emission control is driving low-emission manufacturing innovations. Manufacturers are investing in eco-friendly carbon black solutions to comply with regulations and cater to sustainability-conscious industries.

Carbon Black Market - Strategic Insights:

Get more information on this report

Carbon Black Market Segmentation Analysis:

Key segments that contributed to the derivation of the carbon black market analysis are type, application, and grade.

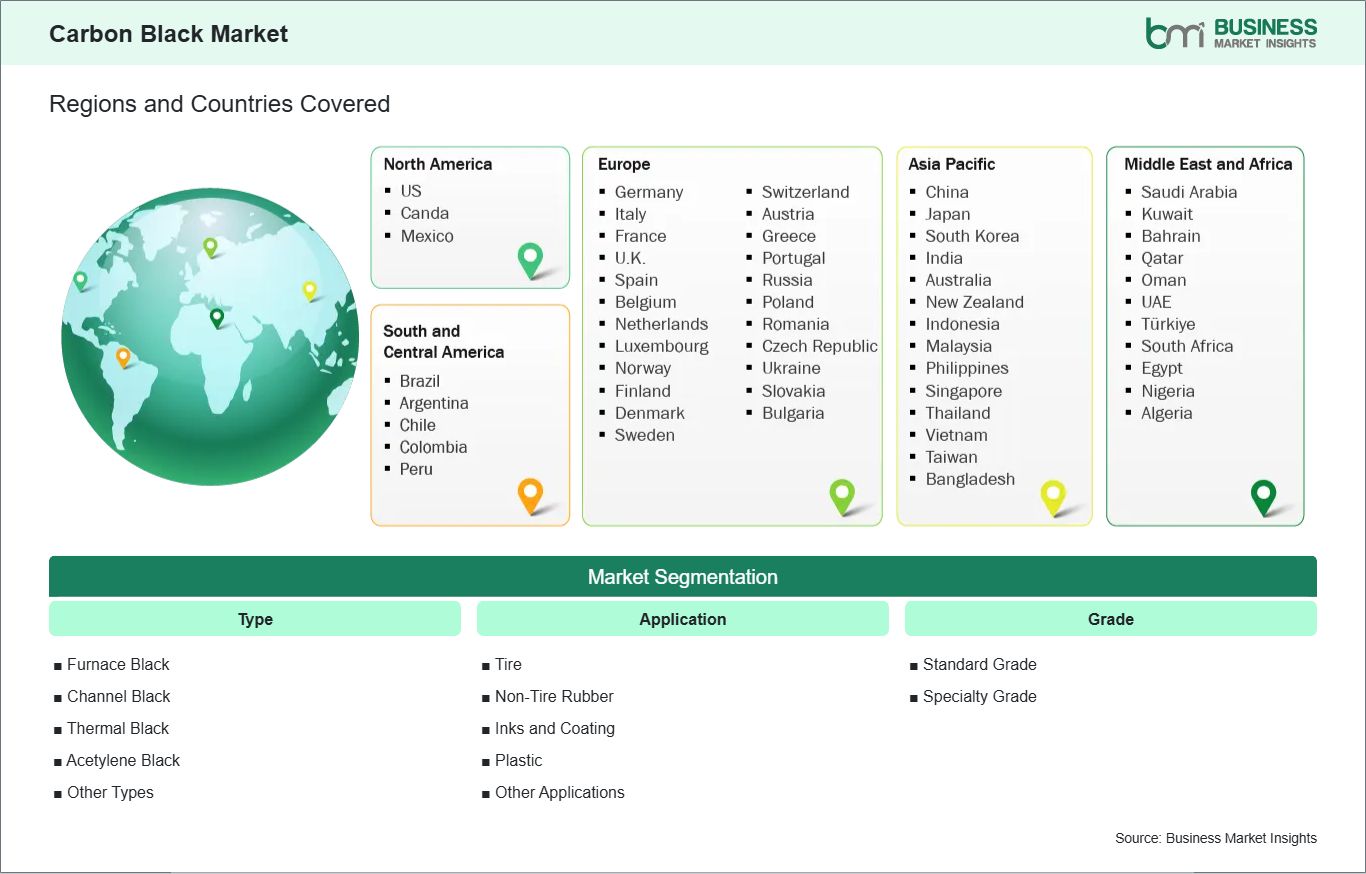

By type, the carbon black market is segmented into furnace black, channel black, thermal black, acetylene black, and other types. Furnace black dominated the market in 2025.

By application, the carbon black market is segmented into tire, non-tire rubber, inks and coatings, plastics, and other applications. Tire dominated the market in 2025.

By grade, the carbon black market is segmented into standard grade and specialty grade. Standard grade dominated the market in 2025.

Carbon Black Market Drivers and Opportunities:

Rising Demand from Tire and Automotive Industries

The main drivers of the global market for carbon black are the tire and automotive sectors. Carbon black is used as a reinforcing filler in tires through the enhancement of tensile strength, abrasion resistance and durability of both tires and their data. As the automotive sector continues to grow around the world, and especially in the developing world, so will the global demand for tires as it pertains to the production of passenger vehicles, commercial trucks, and off-road vehicles using carbon black as the basis of those vehicles. As well, as the trend towards electric vehicles creates greater need for specialized and high-end tires using specialty carbon black grades, manufacturers are continuing to spend large sums of money on producing lightweight and fuel-efficient tires while adhering to safety and durability standards. To this end, carbon black will continue to help tire manufacturers reach the aforementioned performance targets; therefore, securing a steady growth market for carbon black. Similarly, in regards to non-tire rubber products, such as belts, hoses and gaskets, they utilize carbon black to achieve enhanced strength and durability. The increase in industrial and commercial activity, infrastructure and machinery construction and production will continue to lead to increased demand for these end-use products. Emerging economies, particularly in Asia Pacific where automotive production has exploded, will play a key role in driving the growth of the carbon black market.

As with tires, carbon black contributes to increasing thermal effects and UV resistance in rubber components made from carbon black-based materials for outdoor applications and or high-end applications. Therefore, through the same reasons stated above, the automotive market will have significant expansion potential in both the industrial and commercial use of carbon-black-based materials.

Growth in Specialty Applications and Sustainability Initiatives

The increasing adoption of specialty carbon black in high-performance applications presents a significant market opportunity. Specialty grades, characterized by controlled particle size, high surface area, and tailored conductivity, are used in electronic devices, conductive plastics, coatings, and inks. The expansion of electronic and advanced manufacturing sectors, particularly in North America and Asia Pacific, is fueling demand for these high-value products.

In addition to performance-driven applications, sustainability initiatives are influencing market growth. Environmental regulations targeting emissions and pollutants in carbon black production are encouraging manufacturers to adopt cleaner, low-emission processes. Companies investing in eco-friendly production techniques, such as gas-phase or furnace black processes with emission reduction controls, are better positioned to serve environmentally conscious clients and comply with regulatory standards.

Carbon black is also increasingly integrated into high-performance plastics and polymer composites, where it enhances mechanical strength, conductivity, and UV resistance. The growing need for electrically conductive materials in batteries, electronics, and EV components is driving specialty carbon black adoption.

Furthermore, the inks and coatings industry presents another growth avenue, with carbon black serving as a primary pigment in printing inks, paints, and industrial coatings. Rising demand for packaging, printing, and high-quality coating applications globally is supporting market expansion.

Overall, the combination of specialty applications, regulatory compliance, and environmental sustainability is enabling manufacturers to innovate and diversify their product portfolios, creating new revenue streams and long-term growth opportunities for the carbon black market.

Carbon Black Market Size and Share Analysis:

The Carbon Black Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within type, application, and grade, offering insights into their contribution to overall market performance.

By type, the furnace black subsegment dominated the market in 2025, due to widespread use in rubber reinforcement.

In terms of application, the tire subsegment dominated the market in 2025, driven by global automotive production.

By grade, the standard grade subsegment dominated the market in 2025, owing to high demand from conventional tire and rubber applications.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Cabot Corporation

Birla Carbon

Orion Engineered Carbons

Continental Carbon

Tokai Carbon

Phillips Carbon Black

ASEC Carbon

Ferro Corporation

Columbian Chemicals Company

Jiangxi Blackcat Carbon

Get more information on this report

Carbon Black Market Report Coverage and Deliverables:

The "Carbon Black Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Carbon Black Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Carbon Black Market trends, as well as drivers, restraints, and opportunities

Carbon Black Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Carbon Black Market

Detailed company profiles, including SWOT analysis

Carbon Black Market Geographic Insights:

The geographical scope of the Carbon Black Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America represents a mature market with well-established automotive, plastics, and electronics sectors. The United States and Canada have high demand for specialty carbon black in coatings, inks, and conductive materials. Regulatory emphasis on environmental compliance and sustainable production practices supports the adoption of cleaner carbon black products.

Europe also exhibits steady growth due to stringent environmental regulations, strong automotive production, and emphasis on industrial efficiency. Germany, France, and Italy are key markets, with a focus on high-performance and specialty carbon black applications. Asia Pacific market is growing due to rapid industrialization, robust automotive production, and high demand for tires and rubber products. Countries such as China, India, and Japan are leading consumers of carbon black for both tire and non-tire applications. The expansion of the automotive and electronics industries in the region is driving demand for standard and specialty carbon black products.

The Middle East & Africa region is witnessing gradual growth driven by tire production, industrial rubber, and plastics manufacturing. Emerging automotive and industrial sectors in the Gulf Cooperation Council (GCC) countries are supporting market expansion.

South & Central America, particularly Brazil and Mexico, is experiencing moderate growth due to increasing industrialization and automotive production. Across all regions, industrial demand, regulatory compliance, and specialty application adoption shape the competitive dynamics of the carbon black market.

Get more information on this report

Carbon Black Market Research Report Guidance:

The report includes qualitative and quantitative data in the Carbon Black Market across type, application, grade, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Carbon Black Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Carbon Black Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Carbon Black Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Carbon Black Market segments by type, application, grade, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Carbon Black Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Carbon Black Market News and Key Development:

The Carbon Black Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the carbon black market are:

March 2025: Cabot Corporation expanded specialty carbon black portfolio with high-conductivity grade for automotive and electronics.

July 2025: Birla Carbon expanded Indian plant capacity to meet tire and rubber industry demand.

Key Sources Referred:

International Rubber Study GroupUS Environmental Protection AgencyEuropean Chemicals AgencyChina National Chemical Information CenterInternational Energy AgencyInternational Trade Administration

The List of Companies - Carbon Black Market

Cabot Corporation

Birla Carbon

Orion Engineered Carbons

Continental Carbon

Tokai Carbon

Phillips Carbon Black

ASEC Carbon

Ferro Corporation

Columbian Chemicals Company

Jiangxi Blackcat Carbon

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Carbon Black Market?

The Carbon Black Market is valued at US$ 16.87 Billion in 2025, it is projected to reach US$ 23.42 Billion by 2033.

What is the CAGR for Carbon Black Market by (2026 - 2033)?

As per our report Carbon Black Market, the market size is valued at US$ 16.87 Billion in 2025, projecting it to reach US$ 23.42 Billion by 2033. This translates to a CAGR of approximately 4.19% during the forecast period.

What segments are covered in this report?

The Carbon Black Market report typically cover these key segments-

Type (Furnace Black, Channel Black, Thermal Black, Acetylene Black, Other Types)

Application (Tire, Non-Tire Rubber, Inks and Coating, Plastic, Other Applications)

Grade (Standard Grade, Specialty Grade)

What is the historic period, base year, and forecast period taken for Carbon Black Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Carbon Black Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Carbon Black Market?

The Carbon Black Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Cabot Corporation

Birla Carbon

Orion Engineered Carbons

Continental Carbon

Tokai Carbon

Phillips Carbon Black

ASEC Carbon

Ferro Corporation

Columbian Chemicals Company

Jiangxi Blackcat Carbon

Who should buy this report?

The Carbon Black Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Carbon Black Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Carbon Black Market

Get Free Sample For Carbon Black Market