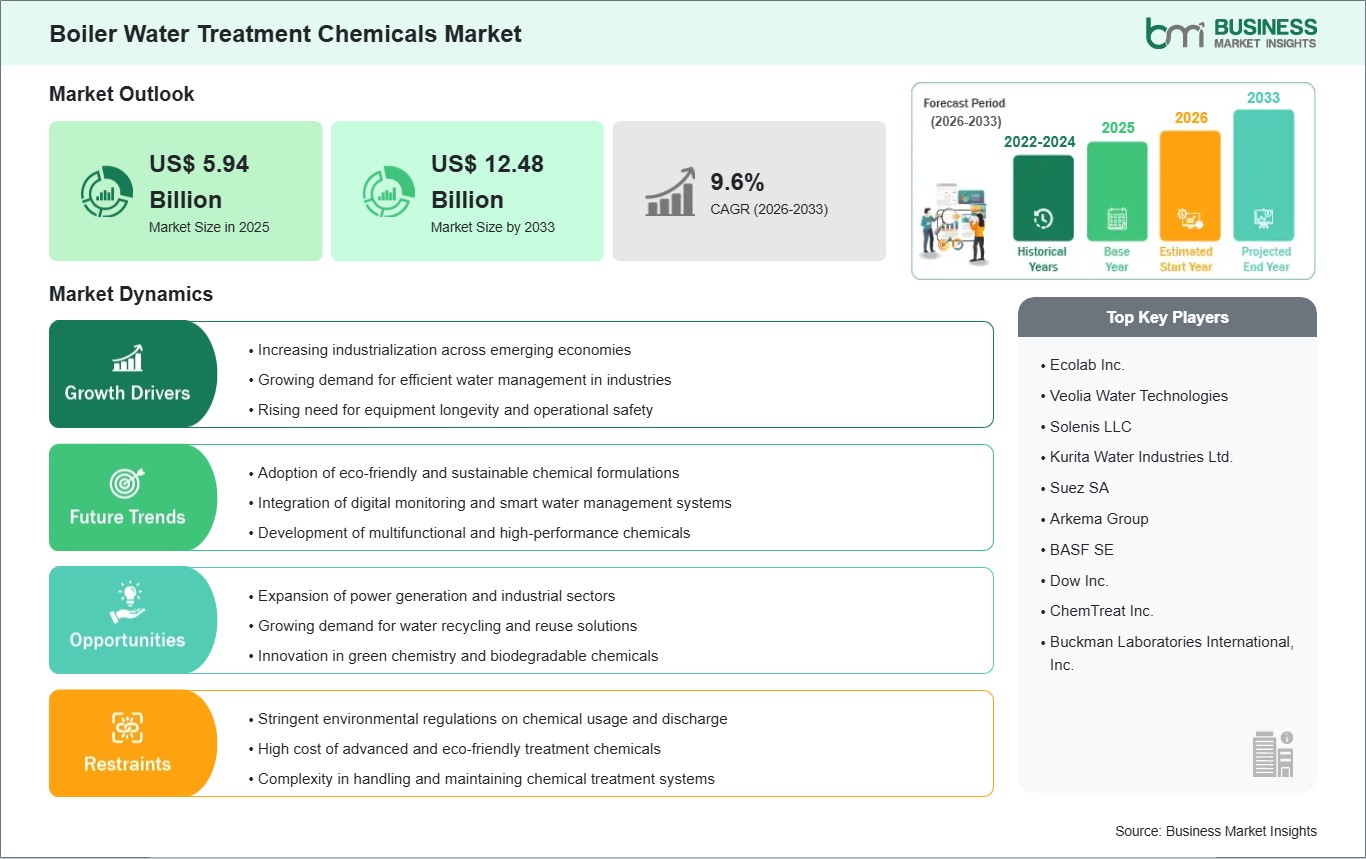

The Boiler Water Treatment Chemicals Market size is expected to reach US$ 12.48 Billion by 2033 from US$ 5.94 Billion in 2025. The market is estimated to record a CAGR of 9.72% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global boiler water treatment chemicals market is driven by the increasing need for efficient water management, equipment longevity, and operational safety across industrial processes. These chemicals play a critical role in preventing corrosion, scaling, and microbial growth in boilers, ensuring optimal heat transfer efficiency and reducing maintenance costs. Industries such as power generation, oil & gas, and manufacturing heavily rely on boiler systems, thereby sustaining consistent demand for treatment solutions.

Growing industrialization, especially in emerging economies, is increasing the deployment of boilers, which in turn fuels demand for water treatment chemicals. Additionally, stricter environmental regulations and water discharge norms are pushing industries to adopt advanced chemical formulations that improve efficiency while minimizing environmental impact.

Competitive dynamics in this market are centered on product innovation, sustainability, and compliance with environmental standards. Manufacturers are investing in eco-friendly formulations, multifunctional chemicals, and digital monitoring solutions that optimize chemical dosing and performance. Partnerships with industrial operators and service providers are also becoming common to deliver integrated water treatment solutions. Regulatory frameworks emphasize safe handling, environmental compliance, and performance validation, shaping product development and commercialization strategies.

Boiler Water Treatment Chemicals Market - Strategic Insights:

Get more information on this report

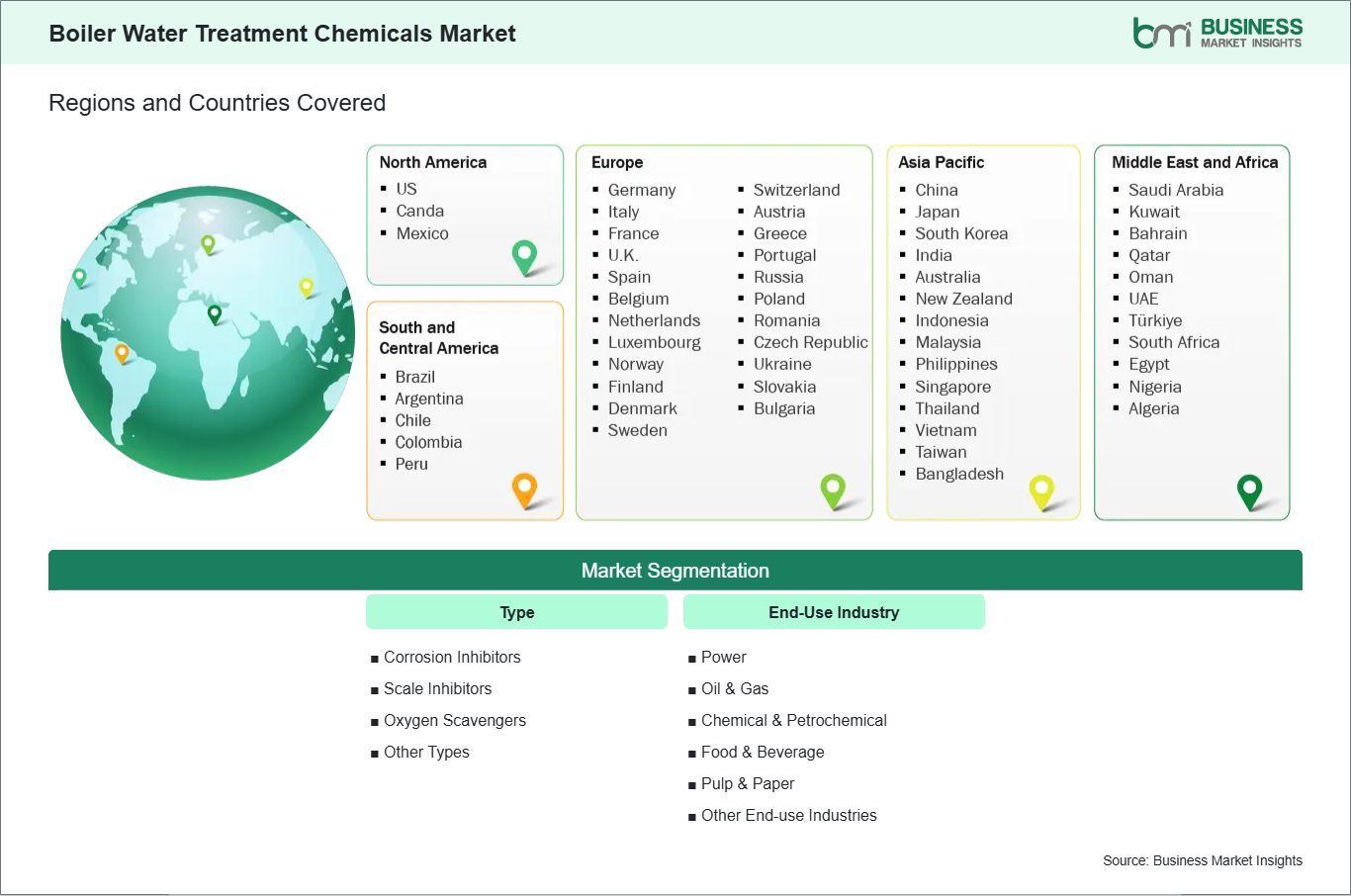

Boiler Water Treatment Chemicals Market Segmentation Analysis:

Key segments that contributed to the derivation of the boiler water treatment chemicals market analysis are type and end-use industry.

By type, the boiler water treatment chemicals market is segmented into corrosion inhibitors, scale inhibitors, oxygen scavengers, and other types. The corrosion inhibitors segment dominated the market in 2025.

Based on end-use industry, the boiler water treatment chemicals market is categorized into power, oil & gas, chemical & petrochemical, food & beverage, pulp & paper, and other end-use industries. The power segment dominated the market in 2025.

Boiler Water Treatment Chemicals Market Drivers and Opportunities:

Increasing Industrialization

Industrialization is a primary factor leading to the growth of the boiler water treatment chemicals market. Various industries that produce steam or use steam in their thermal processes, including Power generation, Oil & Gas production, Chemical processing, and Food manufacturing, rely on boiler systems for these processes. Since boilers require high-quality water in order to work effectively, treatment chemicals are essential for ensuring efficient boiler operation through the avoidance of performance issues or system failure. Corrosion and scaling are two of the most widespread problems facing industrial boiler systems. The problems associated with these two types of damage can result in reduced efficiency of heat transfer through the boiler, increased energy usage, and excessive capital expenditures for replacement equipment that may have been prevented with the appropriate treatment program. To help ensure the integrity of a boiler system, many industrial operators apply corrosion inhibitors, scale inhibitors, and oxygen scavengers to their systems. As manufacturers continue to expand capacity, there will be increased demand for boiler water treatment chemicals.

Strong industrial and energy sector growth throughout the developing world, particularly in Asia Pacific, has been evident over the past several years. The installation of boilers has been accelerating as a result of various government initiatives to improve infrastructure and increase industrial output. Due to the growth in global energy consumption, the number of thermal power plants will also continue to grow, thereby continuing to support growth in the boiler water treatment chemicals market.

Increasing operational efficiency and reducing costs are also important factors driving demand for boiler water treatment chemicals. Industrial operations are utilizing these types of chemicals with increased frequency than in the past to meet these objectives.

Stringent Environmental Regulations

Increasingly strict environmental regulation, sustainability initiatives and eco-friendly chemicals are offering tremendous potential for commercial development of the global market for chemicals used in the treatment of boiler feed water. Across the world, governments and regulating agencies are passing and enforcing very strict policies regarding water use, wastewater discharge and the chemical safety. These regulations create an incentive for all types of industries to develop and utilize advanced treatment solutions that will not only improve boiler operations but also reduce environmental harm.

Reducing the discharge of harmful chemicals into our water supplies is one of the most significant drivers of regulation related to boiler chemical treatment. Many of the traditional chemicals used to treat boiler feed water contain one or more materials that can either be hazardous to the environment and/or difficult to degrade, which has resulted in a greatly increased demand for "green" biodegradable alternatives. In response, many companies are working to develop "green chemistry" processes that are environmentally compliant and help maintain high levels of treatment, thereby creating opportunities for both innovation and product differentiation.

In addition to sustainable chemical treatment options, regulatory guidelines are also becoming more stringent regarding the efficient use of water. As more and more industries are required to recycle and reuse water, they must also adopt more advanced water treatment systems. The many companies developing advanced chemicals for the treatment of boiler feed water are designing those chemicals to perform effectively with recycled water systems so that they can maintain a consistent level of chemical treatment despite changes in the quality of the feed water to the system.

Another growth opportunity tied to regulatory compliance is the digital transformation. Companies are implementing "smart" water management systems, and increasingly, businesses of all sizes implementing IoT and digital technologies focused on the management of water and its use during boiler operations.

Boiler Water Treatment Chemicals Market Size and Share Analysis:

The Boiler Water Treatment Chemicals Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within type and end-use industry, offering insights into their contribution to overall market performance.

By type, the corrosion inhibitors subsegment dominated the market in 2025, driven by their critical role in preventing metal degradation and extending boiler life.

Based on end-use industry, the power subsegment dominated the market in 2025, driven by the extensive use of boilers in thermal and nuclear power plants.

Boiler Water Treatment Chemicals Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Ecolab Inc.

Veolia Water Technologies

Solenis LLC

Kurita Water Industries Ltd.

Suez SA

Arkema Group

BASF SE

Dow Inc.

ChemTreat Inc.

Buckman Laboratories International, Inc.

Get more information on this report

Boiler Water Treatment Chemicals Market Report Coverage and Deliverables:

The "Boiler Water Treatment Chemicals Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Boiler Water Treatment Chemicals Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Boiler Water Treatment Chemicals Market trends, as well as drivers, restraints, and opportunities

Boiler Water Treatment Chemicals Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Boiler Water Treatment Chemicals Market

Detailed company profiles, including SWOT analysis

Boiler Water Treatment Chemicals Market Geographic Insights:

The geographical scope of the Boiler Water Treatment Chemicals Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America represents a mature market characterized by advanced industrial infrastructure and strict environmental regulations. Industries in the United States and Canada are increasingly adopting high-performance and environmentally compliant treatment chemicals. The focus in this region is on sustainability, operational efficiency, and the integration of digital monitoring technologies for optimized chemical usage.

Europe also demonstrates steady growth, driven by stringent environmental policies and a strong emphasis on energy efficiency. Countries such as Germany, the UK, and France are focusing on reducing emissions and improving water management practices. This has led to increased adoption of eco-friendly and innovative boiler treatment solutions.

In Asia Pacific, countries such as China and India are witnessing strong growth in power generation, manufacturing, and infrastructure development. The increasing number of thermal power plants and industrial facilities is significantly boosting demand for boiler water treatment chemicals. Government initiatives supporting industrial expansion and energy security further contribute to market growth in this region.

In the Middle East & Africa, the market is supported by the expansion of oil & gas and desalination industries. Boiler systems are widely used in these sectors, creating demand for reliable treatment chemicals. Meanwhile, South & Central America is experiencing gradual growth due to rising industrial activities and investments in energy infrastructure.

Across all regions, factors such as regulatory compliance, water scarcity, and the need for energy-efficient operations are shaping market trends. Manufacturers are tailoring their products and strategies to meet regional requirements, ensuring sustained growth in the global market.

Get more information on this report

Boiler Water Treatment Chemicals Market Research Report Guidance:

The report includes qualitative and quantitative data in the Boiler Water Treatment Chemicals Market across type, end-use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Boiler Water Treatment Chemicals Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Boiler Water Treatment Chemicals Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Boiler Water Treatment Chemicals Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Boiler Water Treatment Chemicals Market segments by type, end-use industry, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Boiler Water Treatment Chemicals Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Boiler Water Treatment Chemicals Market News and Key Development:

The Boiler Water Treatment Chemicals Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the boiler water treatment chemicals market are:

In July 2025, Kurita Water Industries Ltd. announced the launch of a new eco‑friendly boiler water treatment chemical line in Japan, designed to reduce scaling and corrosion while minimizing environmental impact.

In November 2025, ChemTreat Inc. (a subsidiary of Danaher Corporation) expanded its boiler water treatment portfolio in North America, introducing advanced oxygen scavenger and scale inhibitor solutions.

Key Sources Referred:

U.S. Environmental Protection Agency (EPA)European Chemicals Agency (ECHA)World Health Organization (WHO)International Energy Agency (IEA)Indian Ministry of Environment, Forest and Climate Change (MoEFCC)Occupational Safety and Health Administration (OSHA)United Nations Environment Programme (UNEP)International Trade Administration

The List of Companies - Boiler Water Treatment Chemicals Market

Ecolab Inc.

Veolia Water Technologies

Solenis LLC

Kurita Water Industries Ltd.

Suez SA

Arkema Group

BASF SE

Dow Inc.

ChemTreat Inc.

Buckman Laboratories International, Inc.

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Boiler Water Treatment Chemicals Market?

The Boiler Water Treatment Chemicals Market is valued at US$ 5.94 Billion in 2025, it is projected to reach US$ 12.48 Billion by 2033.

What is the CAGR for Boiler Water Treatment Chemicals Market by (2026 - 2033)?

As per our report Boiler Water Treatment Chemicals Market, the market size is valued at US$ 5.94 Billion in 2025, projecting it to reach US$ 12.48 Billion by 2033. This translates to a CAGR of approximately 9.72% during the forecast period.

What segments are covered in this report?

The Boiler Water Treatment Chemicals Market report typically cover these key segments-

Type (Corrosion Inhibitors, Scale Inhibitors, Oxygen Scavengers, Other Types)

End-Use Industry (Power, Oil & Gas, Chemical & Petrochemical, Food & Beverage, Pulp & Paper, Other End-use Industries)

What is the historic period, base year, and forecast period taken for Boiler Water Treatment Chemicals Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Boiler Water Treatment Chemicals Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Boiler Water Treatment Chemicals Market?

The Boiler Water Treatment Chemicals Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Ecolab Inc.

Veolia Water Technologies

Solenis LLC

Kurita Water Industries Ltd.

Suez SA

Arkema Group

BASF SE

Dow Inc.

ChemTreat Inc.

Buckman Laboratories International, Inc.

Who should buy this report?

The Boiler Water Treatment Chemicals Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Boiler Water Treatment Chemicals Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Boiler Water Treatment Chemicals Market

Get Free Sample For Boiler Water Treatment Chemicals Market