01

Market Summery

Executive Summary and Global Market Analysis

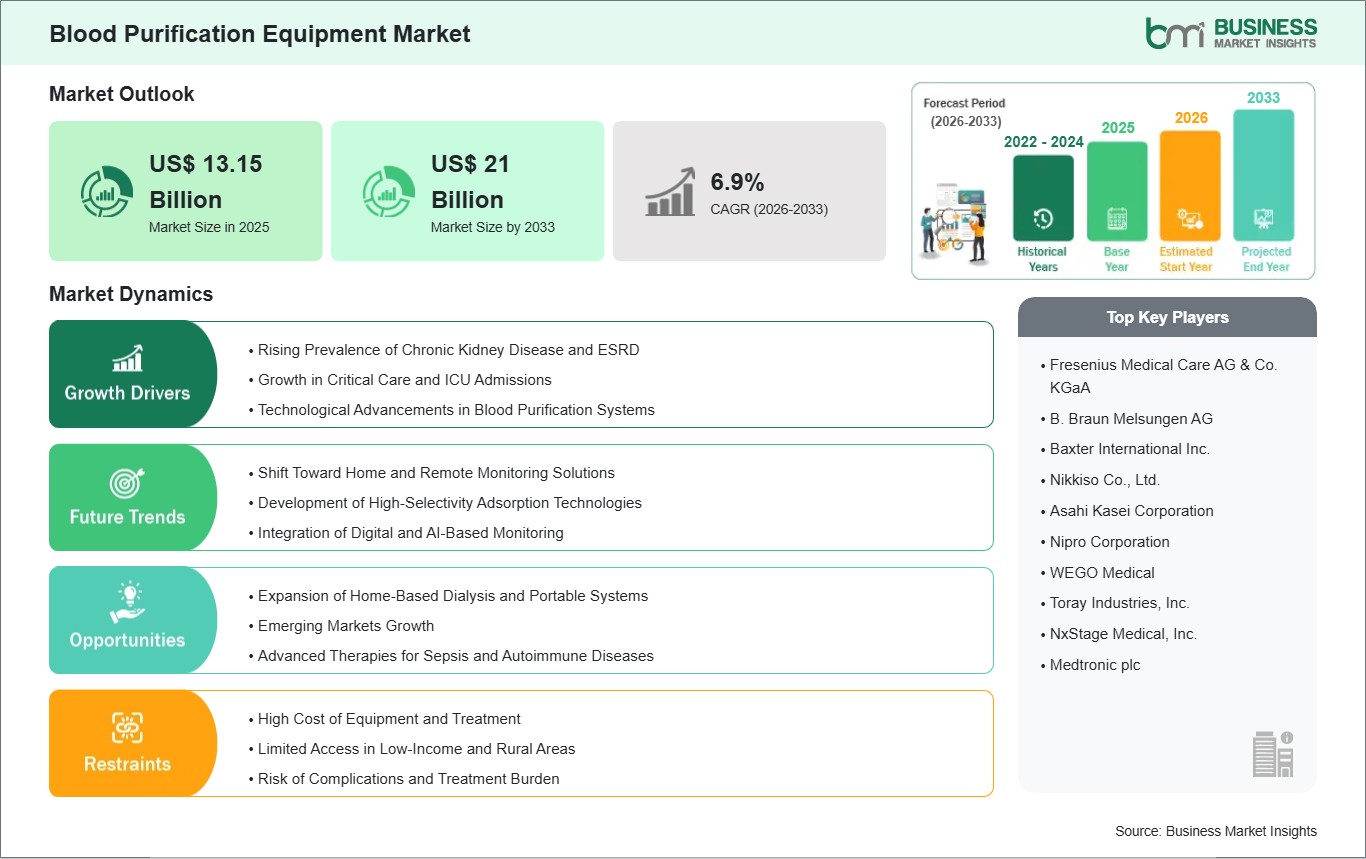

The global market for blood purification equipment is gradually expanding. The growth is largely attributed to the increasing incidence of chronic kidney disease (CKD), end, stage renal disease (ESRD), acute kidney injury, and sepsis globally. Blood purification methods that include hemodialysis, continuous renal replacement therapy (CRRT), hemoperfusion, and plasmapheresis are vital in the removal of toxins, excess fluids, and inflammatory mediators from the blood of, for instance, critically ill patients.

The rising incidence of diabetes and hypertension two major risk factors for kidney failure has a patient population of those requiring long, term dialysis and extracorporeal blood purification therapies that has been hugely expanded. Among the improvements that are driving up the treatment efficiency, patient comfort, and clinical outcomes are technological advancements such as upgraded dialysis membranes, portable and home, based dialysis systems, and sophisticated adsorption technologies. Healthcare facilities and dialysis centers continue to be the major end users, whereas the home care sector is gradually capturing a larger share of the market as the patient, centric care and cost reduction are more and more emphasized.

The market is dominated by North America and Europe where advanced therapies are readily adopted due to the presence of a well, developed healthcare infrastructure. Asia Pacific, on the other hand, is progressively becoming a significant market for the industry backed by a large patient base, the expansion of dialysis networks, and increasing healthcare investments. The market trajectory is still upbeat, justified by clinical needs, technological innovations, and the increasing worldwide incidence of renal and critical care conditions.

03

Segment Analysis

Blood Purification Equipment Market Segmentation

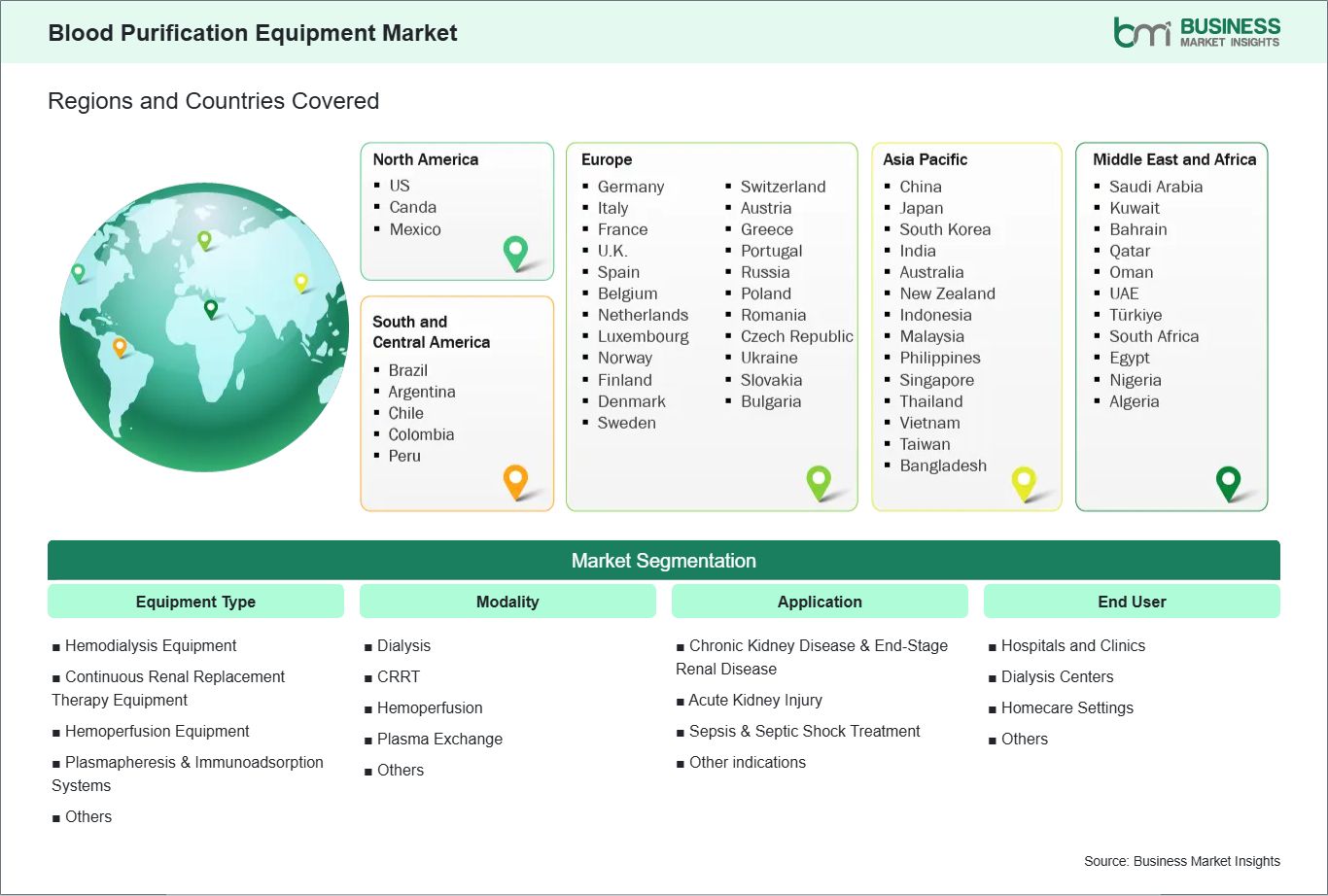

By equipment type, the blood purification equipment market is segmented into hemodialysis equipment, continuous renal replacement therapy (CRRT) equipment, hemoperfusion equipment, plasmapheresis and immunoadsorption systems, others. The hemodialysis equipment segment dominated the market in 2024.

- By modality, the market is segmented dialysis (intermittent, conventional), CRRT, hemoperfusion, plasma exchange, others. The dialysis (intermittent, conventional)segment held the largest share of the market in 2024.

- By application, the market is segmented into chronic kidney disease and end-stage renal disease (ESRD), acute kidney injury, sepsis and septic shock treatment, other indications. The chronic kidney disease and end-stage renal disease (ESRD) segment held the largest share of the market in 2024.

- By end user, the market is segmented into hospitals and clinics, dialysis centers, homecare settings, others. The dialysis centers segment held the largest share of the market in 2024.

04

Market Forces

Blood Purification Equipment Market Drivers and Opportunities

Rising Prevalence of Chronic Kidney Disease and Critical Illnesses

The market for blood purification systems has grown rapidly due to the enormous increase in the number of patients with chronic kidney disease, end stage renal disease, sepsis and acute kidney injury. Worldwide, diabetes and high blood pressure (hypertension) represent the two most important factors increasing the number of people with kidney failure and therefore requiring dialysis and blood purification treatments. Patients with advanced kidney disease must rely on lifelong or long-term treatments to remove toxins from their bodies and maintain metabolic balance. Blood purification technology is being used more often in intensive care units to help treat critically ill patients with inflammation by regulating their inflammatory mediators, treat patients with organ systems that have been damaged by infection or multiple organ failure and lower their risk of developing sepsis. The growth of the elderly population is driving this trend because older people are at higher risk of developing renal failure and other serious medical conditions that require external blood purification devices. Likewise, the ability of doctors and medical facilities to diagnose kidney diseases earlier and provide more people with access to services for treating these conditions have increased the number of patients being treated and are having an impact on the equipment utilized to treat patients. Hospitals and dialysis clinics continue to invest in the latest blood purification technologies to achieve better patient outcomes, increase operational efficiency and support increased patient demand. In conclusion, the rising number of patients with chronic kidney disease and increased reliance on medical devices for maintaining the viability of their kidneys will be the two major contributing factors to sustained market growth.

Expansion of Home-Based and Advanced Blood Purification Technologies

The blood purification equipment market is quickly expanding into this area of innovation (home-based therapies and advanced purification technologies). Healthcare systems want to relieve the burden on the hospital system by lowering treatment costs and improving Patient Quality of Life. As a result, healthcare systems are interested in home hemodialysis and Portable Dialysis Systems because of their ability to provide patients with the greatest amount of flexibility, convenience, and independence. This is particularly important for patients requiring long-term dialysis. New technological innovations, such as compact machines, automated systems, novel membrane materials, and smart monitoring capabilities, are increasing the safety and accessibility of blood purification at home.

Additionally, new advanced therapies such as hemoperfusion, immunoadsorption, and cytokine adsorption, along with a growing body of clinical research and clinical adoption in Critical Care, are gaining acceptance as important components of the treatment of conditions such as sepsis, auto imune disorders, and inflammatory syndromes. Because of the rapid growth of these advanced therapies in clinical practice, emerging markets throughout Asia Pacific, Latin America, and the Middle East, will provide substantial opportunities for Manufacturers who continue to offer patients advanced, cost-efficient technology that provides both improved clinical outcomes and increased long-term Market Share.

05

Size and Share Analysis

Blood Purification Equipment Market Size and Share Analysis

By equipment type, the blood purification equipment market is segmented into hemodialysis equipment, continuous renal replacement therapy (CRRT) equipment, hemoperfusion equipment, plasmapheresis and immunoadsorption systems, others. The hemodialysis equipment segment dominated the market in 2024. Hemodialysis is the most widely utilized one in the world, which is in line with standardized clinical guidelines and physical infrastructures.

By modality, the market is segmented into dialysis (intermittent, conventional), CRRT, hemoperfusion, plasma exchange, others. The dialysis (intermittent, conventional) segment held the largest share of the market in 2024. It constitutes the regular treatment of ESRD patients in hospitals and outpatient dialysis facilities. Its clinical effectiveness being firmly established, patients undergoing the treatment on a routine basis, and a wide range of developed regions being covered by reimbursement schemes are the major factors that nourish the conquest in the market.

By application, the market is segmented into chronic kidney disease and end-stage renal disease (ESRD), acute kidney injury, sepsis and septic shock treatment, other indications. The chronic kidney disease and end-stage renal disease (ESRD) segment held the largest share of the market in 2024. Rise in demand for blood purification therapy of renal diseases. This is attributable to the aging populations and lifestyle, related conditions, in particular, that have become more prevalent.

By end user, the market is segmented hospitals and clinics, dialysis centers, homecare settings, others. The dialysis centers segment held the largest share of the market in 2024. The segment growth is driven by the high patient volumes, specialized infrastructure, and routine use of blood purification equipment for scheduled treatments.

07

Report Coverage

Blood Purification Equipment Market Report Coverage and Deliverables

The "Blood Purification Equipment Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Blood Purification Equipment market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Blood Purification Equipment market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Blood Purification Equipment market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Blood Purification Equipment market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Blood Purification Equipment Market Geographic Insights

The geographical scope of the Blood Purification Equipment market report is divided into five regions: North America, Asia Pacific, Europe, Middle East and Africa, and South and Central America. The Blood Purification Equipment market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific Blood Purification Equipment market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The number of patients with chronic kidney disease (CKD) and end-stage renal disease (ESRD) is increasing in Asia-Pacific because of diabetes, high blood pressure, an aging society, and many other factors. Countries like China, India, Japan, and South Korea have some of the biggest CKD/ESRD populations and many more dialysis facilities are being developed and invested in. Governments in Asia-Pacific have also been taking steps to enhance their renal healthcare services; they have opened new dialysis centers and improved their reimbursement policy for renal services. The market has experienced significant growth due to the introduction of compact hemodialysis machines, newer technologies like continuous renal replacement therapy (CRRT) systems, and advanced hemoperfusion devices. Additionally, the continuing rise of intensive care units is likely to support further applications of blood purification processes for AKI and sepsis. While there is continued growth in the use of home-based dialysis because of a need to alleviate pressure on hospitals and provide convenience to patients, the Asia-Pacific blood purification equipment market remains a promising opportunity for investors due to the growing number of individuals with unmet clinical needs.

10

Industry Activity

Recent Developments

The Blood Purification Equipment market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the blood purification equipment market are:

- In October 2024, CytoSorbents Corporation announced the US Food and Drug Administration (FDA) has accepted its De Novo medical device application for DrugSorb-ATR and initiated substantive review. The goal of DrugSorb-ATR, an investigational medical device, is to reduce the severity of perioperative bleeding in patients on ticagrelor (Brilinta, AstraZeneca) undergoing coronary artery bypass graft (CABG) surgery.

- In June 2024, CytoSorbents Corp has launched its PuriFi hemoperfusion machine in the European Union (EU), following approval and certification under the EU Medical Device Regulation (MDR).

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade Indicators

World Trade Organization (WTO)

Centers for Disease Control and Prevention (CDC)

World Health Organization (WHO)

(International Monetary Fund )IMF

International Trade Administration (ITA)

Company website

Company annual reports

Company investor presentations