01

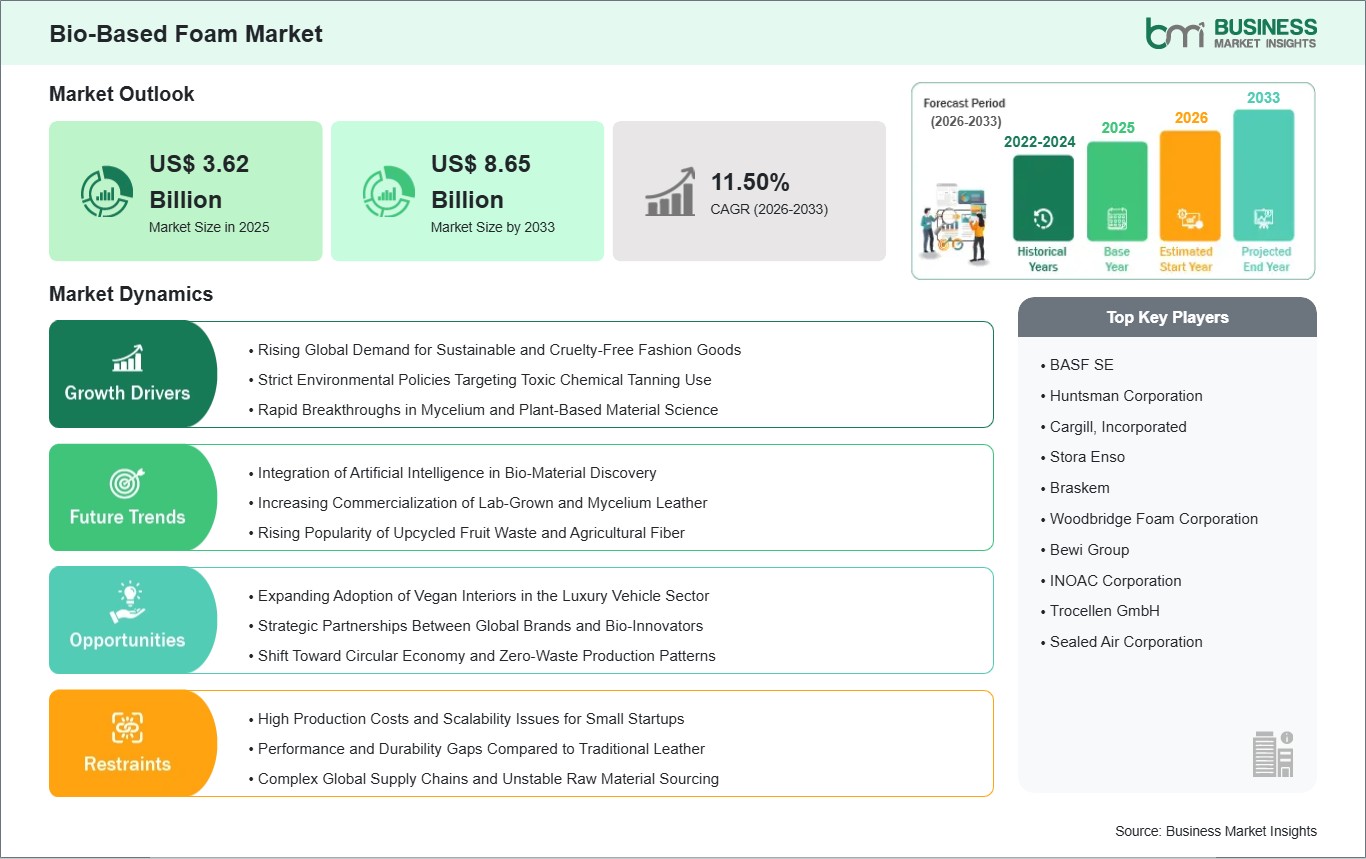

Market Summery

Executive Summary and Global Market Analysis

Bio-based foams are lightweight, porous materials produced from renewable biological feedstocks, including vegetable oils (soy, castor), starches, sugarcane, and cellulose, as alternatives to conventional petroleum-based hydrocarbons. These eco-friendly foams are stepping in as sustainable alternatives to traditional petroleum-based plastics. From bio-polyurethane and polylactic acid foams to bio-polyethylene and starch-based cushioning, these products are reshaping industries. They not only help reduce plastic waste but also offer superior thermal insulation for greener buildings and provide lightweight, protective packaging for delicate goods shipped worldwide. The market is gaining momentum due to the surge in demand for plastic-free packaging, tougher government rules on producer responsibility, and heightened corporate commitments to carbon neutrality. Additionally, the adoption of advanced microbial fermentation and CO2-polyol synthesis, which convert waste gases into valuable foam components, is significantly enhancing the sustainability of the chemical supply chain.

However, several challenges may impede market growth. High initial procurement and production costs, especially for specialty biopolymers such as polyhydroxyalkanoates (PHAs), hinder adoption in cost-sensitive retail and industrial sectors. Regulatory barriers, including changing standards for compostability and bio-content verification, prolong time-to-market and raise development expenses for manufacturers. Additionally, the industry faces constraints from feedstock volatility and material performance limitations. Reliance on seasonal crops can disrupt supply chains, and certain bio-foams fail to meet the flame retardancy or long-term moisture resistance required for aerospace and marine applications.

Despite these hurdles, the market holds immense opportunities in the universal mandate for circular economy practices and the accelerating deployment of low-carbon automotive interiors as OEMs shift toward fully electric fleets. The expansion of home-compostable e-commerce void-fill and the development of next-generation mycelium-based foams that offer carbon-negative profiles are expected to create significant opportunities for market growth.

03

Segment Analysis

Bio-Based Foam Market Segmentation

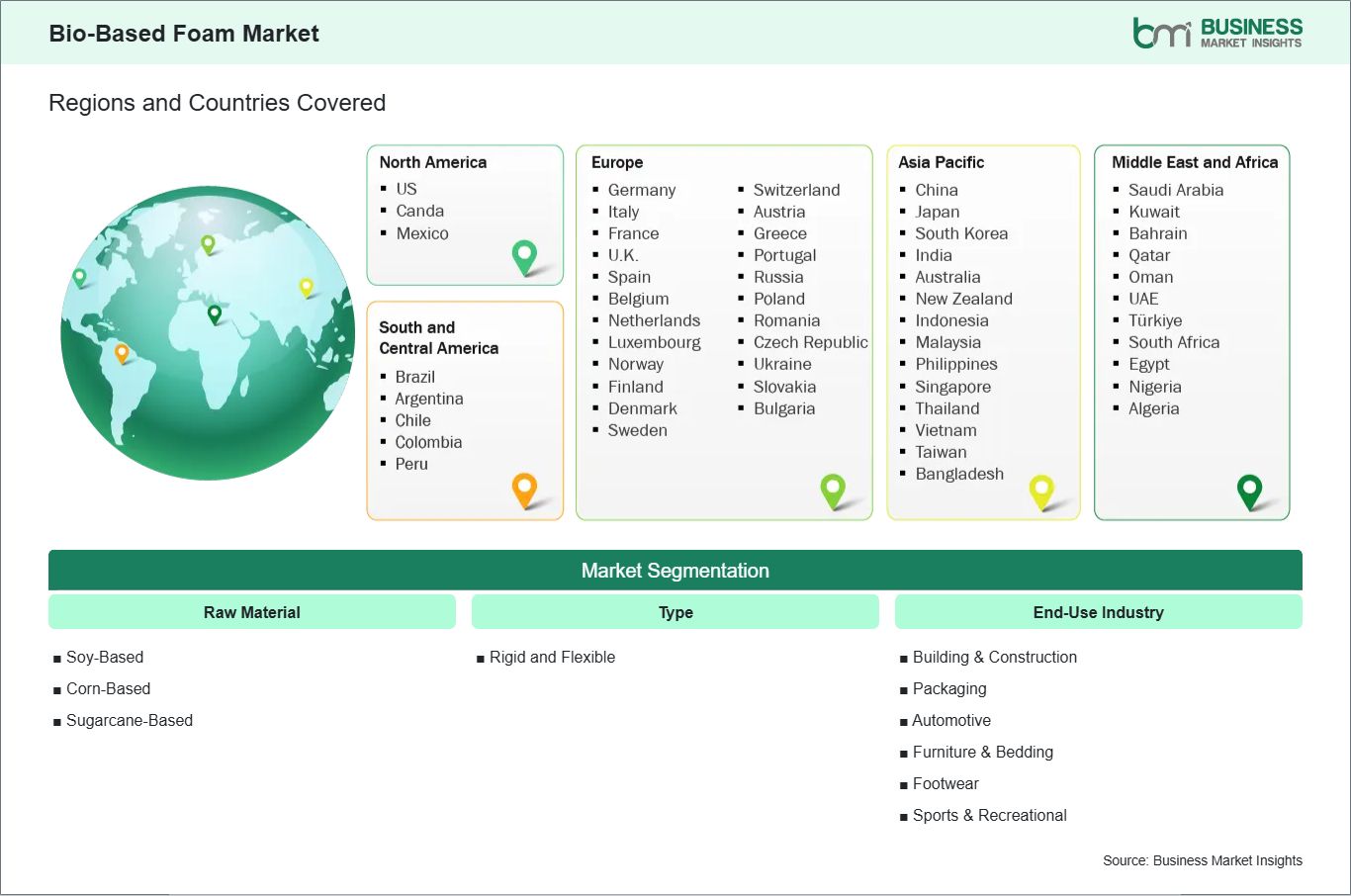

Key segments that contributed to the derivation of the Bio-Based Foam market analysis are raw material, type, and end-use industry.

- By Raw Material, the market is segmented into Soy-Based, Corn-Based, and Sugarcane-Based.

- By Type, the market is divided into Rigid and Flexible.

- By End-Use Industry, the market is categorized into Building &Construction, Packaging, Automotive, Furniture & Bedding, Footwear, and Sports &Recreational

04

Market Forces

Bio-Based Foam Market Drivers and Opportunities

Environmental Stewardship and the Lightweighting Imperative

The primary driver for the Bio-Based Foam Market is the intensifying global push for environmental sustainability combined with the industrial mandate for lightweight, high-performance materials. As traditional petroleum-based foams face increasing scrutiny for their non-biodegradability and significant carbon footprint, industries such as packaging, automotive, and construction are rapidly pivoting toward renewable alternatives. This transition is heavily supported by stringent government regulations and "Green Building" certifications that incentivize the use of bio-derived polyols, sourced from soy, castor oil, and sugarcane, to reduce greenhouse gas emissions.

In the automotive sector specifically, the shift is fueled by the need for lightweight components that enhance fuel efficiency and battery range in electric vehicles. Furthermore, the burgeoning e-commerce sector has created a massive demand for biodegradable protective packaging, as both brands and consumers seek to eliminate microplastic pollution and reduce the volume of plastic waste entering landfills.

Advanced Material Science and Circular Economy Models

A significant high-value opportunity lies in the technical advancement of next-generation bio-foams, such as mycelium-based and algae-derived formulations. These materials offer unique properties like natural fire resistance, high shock absorption, and antimicrobial capabilities, making them ideal for specialized applications in the medical, defense, and high-end furniture sectors. There is also a major growth frontier in the integration of circular economy principles, where agricultural waste and industrial by-products are upcycled into high-quality foam feedstocks. This not only lowers production costs but also provides a "cradle-to-cradle" solution that appeals to eco-conscious global brands.

Additionally, the development of 3D-printed bio-foams presents an opportunity for hyper-customized, waste-free manufacturing of orthopedic cushions, footwear soles, and complex acoustic panels. Manufacturers who focus on improving the moisture resistance and durability of bio-based flexible foams, ensuring they meet the rigorous performance standards of traditional materials, are positioned to lead the mainstream adoption of renewable foam technologies.

05

Size and Share Analysis

Bio-Based Foam Market Size and Share Analysis

The Bio-Based Foam market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within raw material, type, and end-use industry, offering insights into their contribution to overall market performance.

Based on Raw Material, the Soy-Based subsegment holds a significant market share, particularly in the production of Flexible foams. Soy-based polyols are indispensable for the Furniture &Bedding and Automotive sectors, where they serve as a sustainable alternative to traditional polyurethane for seat cushions and mattresses. A notable trend in 2026 is the use of high-oleic soybean oil to enhance the oxidative stability and durability of these foams, ensuring they meet the long-term performance standards of the premium automotive market. These innovations are particularly vital in EV interiors, where they empower manufacturers to reduce cabin VOC emissions while lowering the overall carbon footprint of the vehicle.

07

Report Coverage

Bio-Based Foam Market Report Coverage and Deliverables

The "Bio-Based Foam Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Bio-Based Foam market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Bio-Based Foam market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Bio-Based Foam market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Bio-Based Foam market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Bio-Based Foam Market Geographic Insights

The geographical scope of the Bio-Based Foam market report is divided into five regions: North America, Asia Pacific, Europe, Middle East &Africa, and South &Central America.

The Asia-Pacific Bio-Based Foam Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. This region is emerging as the fastest-growing market globally. The expansion is primarily fueled by the region's massive manufacturing capacity and a rising focus on reducing the carbon footprint of exported goods. China is a significant regional contributor, leveraging its vast agricultural feedstocks for soy and starch-based polyols. India is also witnessing a surge in innovation, with domestic researchers developing bio-derived foams for FMCG packaging to combat plastic pollution and groundwater leaching.

Growth is further bolstered by the rising demand for energy-efficient insulation in the building and construction sectors and the adoption of lightweight, bio-based acoustic foams in the automotive industry. The integration of AI-driven material engineering to enhance the mechanical strength and thermal resistance of bio-foams, alongside the expansion of e-commerce requiring sustainable "void-fill" solutions, solidifies Asia-Pacific as a critical driver for the global scaling of the bio-based foam industry.

10

Industry Activity

Recent Developments

The Bio-Based Foam market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Bio-Based Foam market are:

- In April 2025, Temprecision International launched a plant-based foam called Temprecision® Advance Foam. Its renewable biomass materials led to the achievement of OK biobased certification from TÜV Austria with a 4-star rating, the highest available for OK biobased certifications. Temprecision® Advance Foam is a groundbreaking innovation crafted from renewable sourced materials. It is a plant-based, biobased, low-carbon footprint, high-performance foam.

- In October 2025, Braskem launched I'm green™ EVA 21% bio-based foam at K 2025, offering enhanced softness and flexibility for footwear soles and insoles. The foam is made from renewable materials, combining high performance with a reduced carbon footprint. This launch, alongside collaborations with brands like Veja, highlights the growing adoption of sustainable bio-based foam solutions in consumer products .

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

International Energy Agency World Bank – Global Trade Indicators World Trade Organization (WTO) Automotive Electronics CouncilECIAARAIElectronic Components Industry Association (ECIA)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations