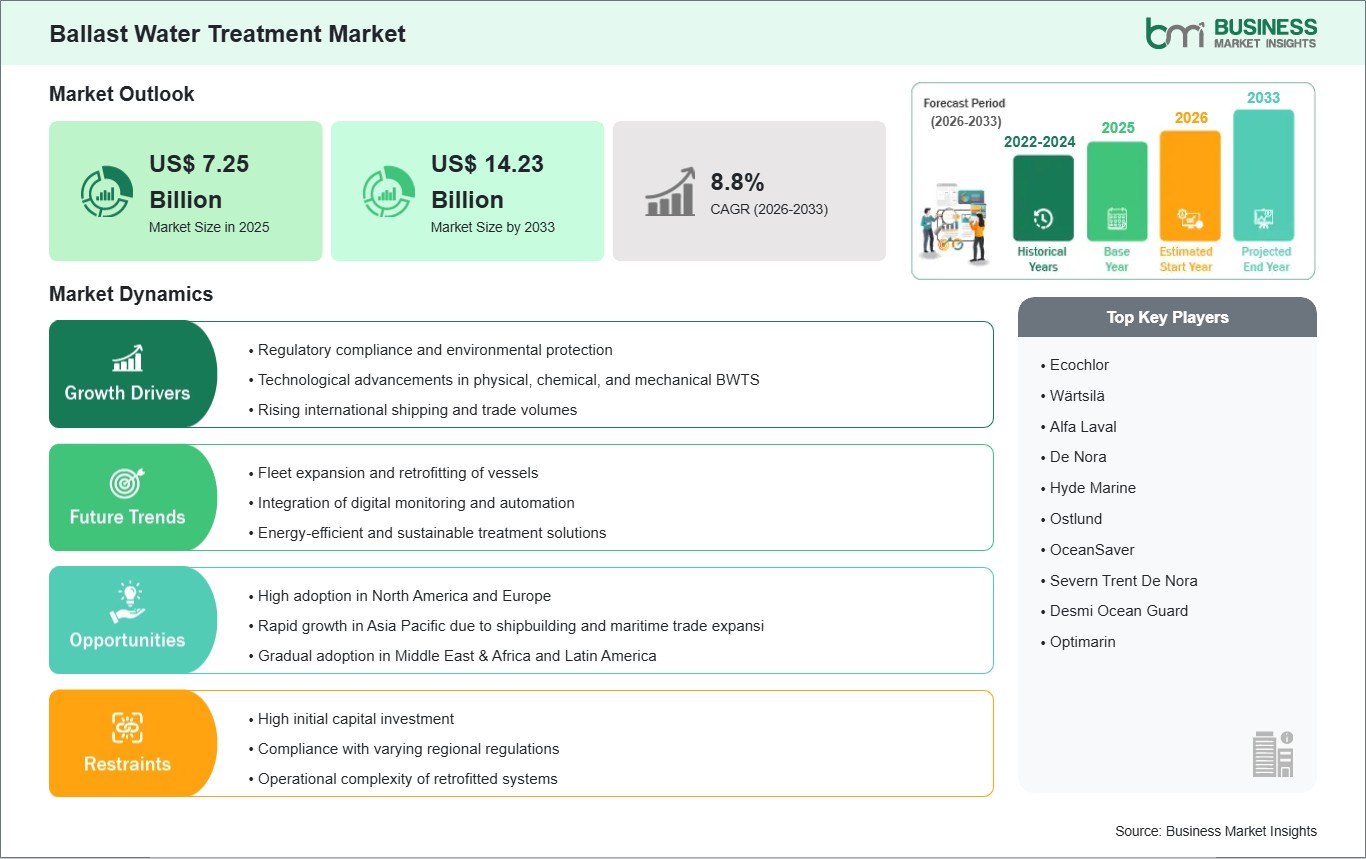

The Ballast Water Treatment Market size is expected to reach US$ 14.23 Billion by 2033 from US$ 7.25 Billion in 2025. The market is estimated to record a CAGR of 8.79% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global ballast water treatment market is defined by increasing regulatory mandates, growing maritime trade, and environmental concerns related to the transfer of invasive aquatic species. Ballast water treatment systems (BWTS) are critical for mitigating the ecological impact of ships discharging untreated ballast water in ports worldwide. Stringent regulations from the International Maritime Organization (IMO) and regional authorities are driving the adoption of BWTS technologies across new and existing vessels.

Market growth is supported by rising international shipping activities, expanding fleet sizes, and retrofitting requirements for existing vessels. Compliance with ballast water management standards requires installation of advanced physical, chemical, or mechanical treatment systems, which protect marine ecosystems and align with environmental sustainability goals.

Competitive dynamics focus on technology innovation, efficiency, and regulatory compliance. Manufacturers are developing systems that optimize energy consumption, reduce operational complexity, and minimize environmental impact. Strategic partnerships with shipbuilders and shipping companies facilitate market penetration and accelerate adoption. Additionally, service-based offerings such as maintenance, calibration, performance monitoring, and repair further drive market engagement and recurring revenue streams.

Ballast Water Treatment Market - Strategic Insights:

Get more information on this report

Ballast Water Treatment Market Segmentation Analysis:

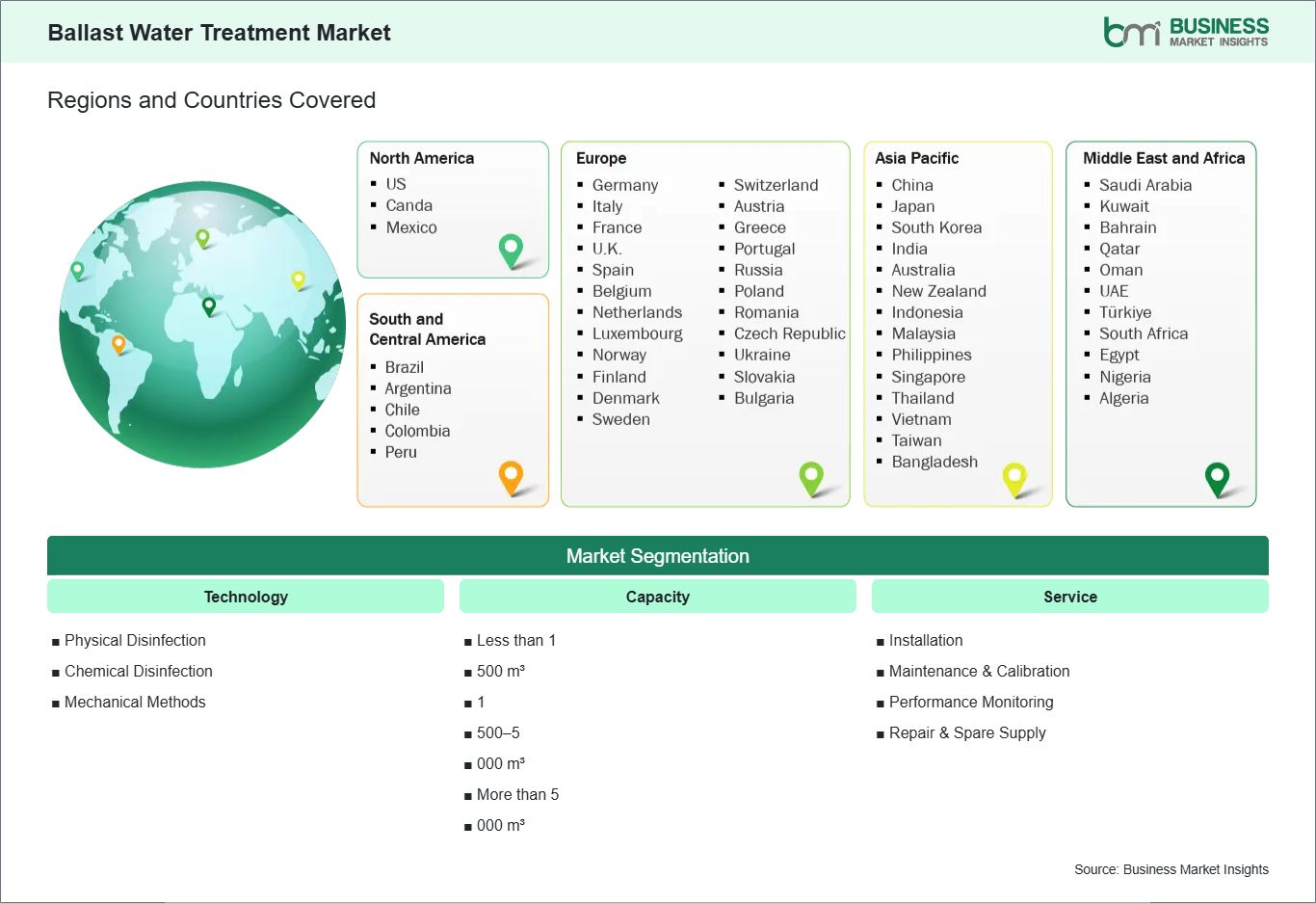

Key segments that contributed to the derivation of the ballast water treatment market analysis are technology, capacity, and service.

By technology, the ballast water treatment market is segmented into physical disinfection, chemical disinfection, and mechanical methods. The physical disinfection segment dominated the market in 2025.

Based on capacity, the ballast water treatment market is segmented into less than 1,500 m³, 1,500–5,000 m³, and more than 5,000 m³. The 1,500–5,000 m³ segment dominated the market in 2025.

In terms of service, the market is segmented into installation, maintenance & calibration, performance monitoring, and repair & spare supply. The installation segment dominated the market in 2025.

Ballast Water Treatment Market Drivers and Opportunities:

Regulatory Compliance and Environmental Concerns

The ballast water treatment market is fundamentally shaped by global regulatory frameworks designed to protect marine ecosystems. The International Maritime Organization (IMO) Ballast Water Management Convention is the cornerstone of these efforts, requiring all ships to install and operate ballast water treatment systems (BWTS) to prevent the transfer of invasive aquatic species. This regulation has created a mandatory compliance environment, ensuring that vessels across international waters adhere to strict discharge standards. Complementing IMO’s global mandate, regional authorities such as the U.S. Coast Guard (USCG) and the European Union have introduced their own stringent rules, reinforcing the need for advanced treatment technologies.

To meet these requirements, shipping companies are adopting physical, chemical, and mechanical BWTS solutions, with a growing emphasis on minimizing ecological impact and operational complexity. UV-based disinfection, electro-chlorination, and filtration systems are increasingly favored for their effectiveness and sustainability. Rising global trade volumes and fleet expansion further amplify the demand for retrofitting older vessels, ensuring they remain compliant with evolving standards. Beyond regulatory pressure, many shipping companies are integrating BWTS into their broader sustainability strategies, positioning themselves as environmentally responsible operators. This dual motivation—compliance and corporate stewardship—creates a strong, sustained demand for ballast water treatment systems. As environmental concerns intensify and regulatory frameworks tighten, the market is expected to grow steadily, driven by the convergence of ecological responsibility and operational necessity.

Fleet Expansion and Service-Based Solutions

The rapid expansion of global shipping fleets and the increasing size of vessels are opening new avenues for ballast water treatment market players. Larger vessels, such as container ships and bulk carriers, require high-capacity treatment systems capable of handling significant ballast volumes. This trend not only drives demand for advanced technologies but also creates opportunities across different capacity segments, including retrofits for older vessels. Retrofitting is particularly important, as many ships built before the IMO convention must now be upgraded to remain compliant, ensuring a steady stream of installations.

Beyond system sales, service-based solutions are emerging as a critical growth driver. Installation, maintenance, calibration, performance monitoring, and spare part supply represent recurring revenue streams that strengthen customer relationships. Advanced monitoring systems, integrated with digital platforms, allow real-time compliance tracking, reducing the risk of fines and operational downtime. Automation and digitalization are also enhancing efficiency, reliability, and ease of operation, making BWTS more attractive to shipowners focused on cost control and sustainability.

As shipping companies prioritize operational efficiency alongside regulatory adherence, the demand for service-integrated ballast water treatment systems is expected to rise. Providers offering comprehensive packages—combining technology, installation, and ongoing support—are well-positioned to capture long-term value. In essence, fleet growth, retrofitting needs, and the shift toward service-driven models are creating a robust ecosystem where ballast water treatment is not just a regulatory requirement but a strategic investment in operational resilience and environmental responsibility.

Ballast Water Treatment Market Size and Share Analysis:

The Ballast Water Treatment Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within technology, capacity, and service, offering insights into their contribution to overall market performance.

By technology, the physical disinfection subsegment dominated the market in 2025, driven by ease of use and environmental compliance.

Based on capacity, the 1,500–5,000 m³ subsegment dominated the market in 2025, driven by the prevalence of medium-sized vessels requiring standardized treatment systems.

In terms of service, the installation subsegment dominated the market in 2025, reflecting the high demand for new installations and retrofitting of existing fleets.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Ecochlor

Wärtsilä

Alfa Laval

De Nora

Hyde Marine

Ostlund

OceanSaver

Severn Trent De Nora

Desmi Ocean Guard

Optimarin

Get more information on this report

Ballast Water Treatment Market Report Coverage and Deliverables:

The "Ballast Water Treatment Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Ballast Water Treatment Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Ballast Water Treatment Market trends, as well as drivers, restraints, and opportunities

Ballast Water Treatment Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Ballast Water Treatment Market

Detailed company profiles, including SWOT analysis

Ballast Water Treatment Market Geographic Insights:

The geographical scope of the Ballast Water Treatment Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The adoption of ballast water treatment systems (BWTS) varies significantly across regions, influenced by factors such as fleet size, vessel age, regulatory enforcement, and the intensity of maritime trade. In North America, the U.S. Coast Guard (USCG) has implemented some of the strictest ballast water discharge standards globally. These regulations have accelerated BWTS adoption among both domestic vessels and international ships calling at U.S. ports. Shipowners operating in this region prioritize compliance to avoid heavy fines and operational restrictions, making North America one of the most mature markets for BWTS implementation.

In Europe, compliance with the International Maritime Organization (IMO) Ballast Water Management Convention is reinforced by the European Union’s environmental initiatives. European authorities emphasize sustainability and ecological protection, driving the adoption of advanced BWTS technologies such as UV radiation and electro-chlorination. The region’s strong regulatory framework, combined with its extensive shipping activity, ensures steady demand for both new installations and retrofits.

The Asia Pacific region represents the largest and fastest-growing market for BWTS. As the global hub for shipbuilding and maritime trade, countries like China, Japan, and South Korea are witnessing rapid fleet expansion. New vessel construction in these nations increasingly integrates BWTS at the design stage, while older fleets are being retrofitted to meet international compliance. The sheer scale of maritime activity in Asia Pacific makes it a critical driver of global BWTS demand.

Meanwhile, emerging markets in the Middle East & Africa and South & Central America are gradually adopting BWTS. These regions are focusing on compliance for new vessels and retrofits, motivated by international trade participation and ecological risk reduction. Although adoption rates are slower compared to North America, Europe, and Asia Pacific, regulatory alignment with IMO standards is fostering steady growth. Collectively, these regional dynamics highlight how regulatory enforcement, fleet modernization, and sustainability priorities shape BWTS adoption worldwide.

Get more information on this report

Ballast Water Treatment Market Research Report Guidance:

The report includes qualitative and quantitative data in the Ballast Water Treatment Market across technology, capacity, service, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Ballast Water Treatment Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Ballast Water Treatment Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Ballast Water Treatment Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Ballast Water Treatment Market segments by technology, capacity, service, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Ballast Water Treatment Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Ballast Water Treatment Market News and Key Development:

The Ballast Water Treatment Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the ballast water treatment market are:

In August 2025, Ecochlor announced the launch of a new chemical-free ballast water treatment system for retrofitting vessels, improving operational efficiency while meeting IMO standards.

In May 2025, Wärtsilä received USCG type approval for its hybrid ballast water treatment system, enabling compliance with both physical and chemical treatment requirements.

Key Sources Referred:

International Maritime Organization (IMO)US Coast Guard (USCG)United Nations Conference on Trade and Development (UNCTAD)Marine Environment Protection Committee (MEPC)

The List of Companies - Ballast Water Treatment Market

Ecochlor

Wärtsilä

Alfa Laval

De Nora

Hyde Marine

Ostlund

OceanSaver

Severn Trent De Nora

Desmi Ocean Guard

Optimarin

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Ballast Water Treatment Market?

The Ballast Water Treatment Market is valued at US$ 7.25 Billion in 2025, it is projected to reach US$ 14.23 Billion by 2033.

What is the CAGR for Ballast Water Treatment Market by (2026 - 2033)?

As per our report Ballast Water Treatment Market, the market size is valued at US$ 7.25 Billion in 2025, projecting it to reach US$ 14.23 Billion by 2033. This translates to a CAGR of approximately 8.79% during the forecast period.

What segments are covered in this report?

The Ballast Water Treatment Market report typically cover these key segments-

Technology (Physical Disinfection, Chemical Disinfection, Mechanical Methods)

Capacity (Less than 1,500 m³, 1,500-5,000 m³, More than 5,000 m³)

What is the historic period, base year, and forecast period taken for Ballast Water Treatment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Ballast Water Treatment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Ballast Water Treatment Market?

The Ballast Water Treatment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Ecochlor

Wärtsilä

Alfa Laval

De Nora

Hyde Marine

Ostlund

OceanSaver

Severn Trent De Nora

Desmi Ocean Guard

Optimarin

Who should buy this report?

The Ballast Water Treatment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Ballast Water Treatment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Ballast Water Treatment Market

Get Free Sample For Ballast Water Treatment Market