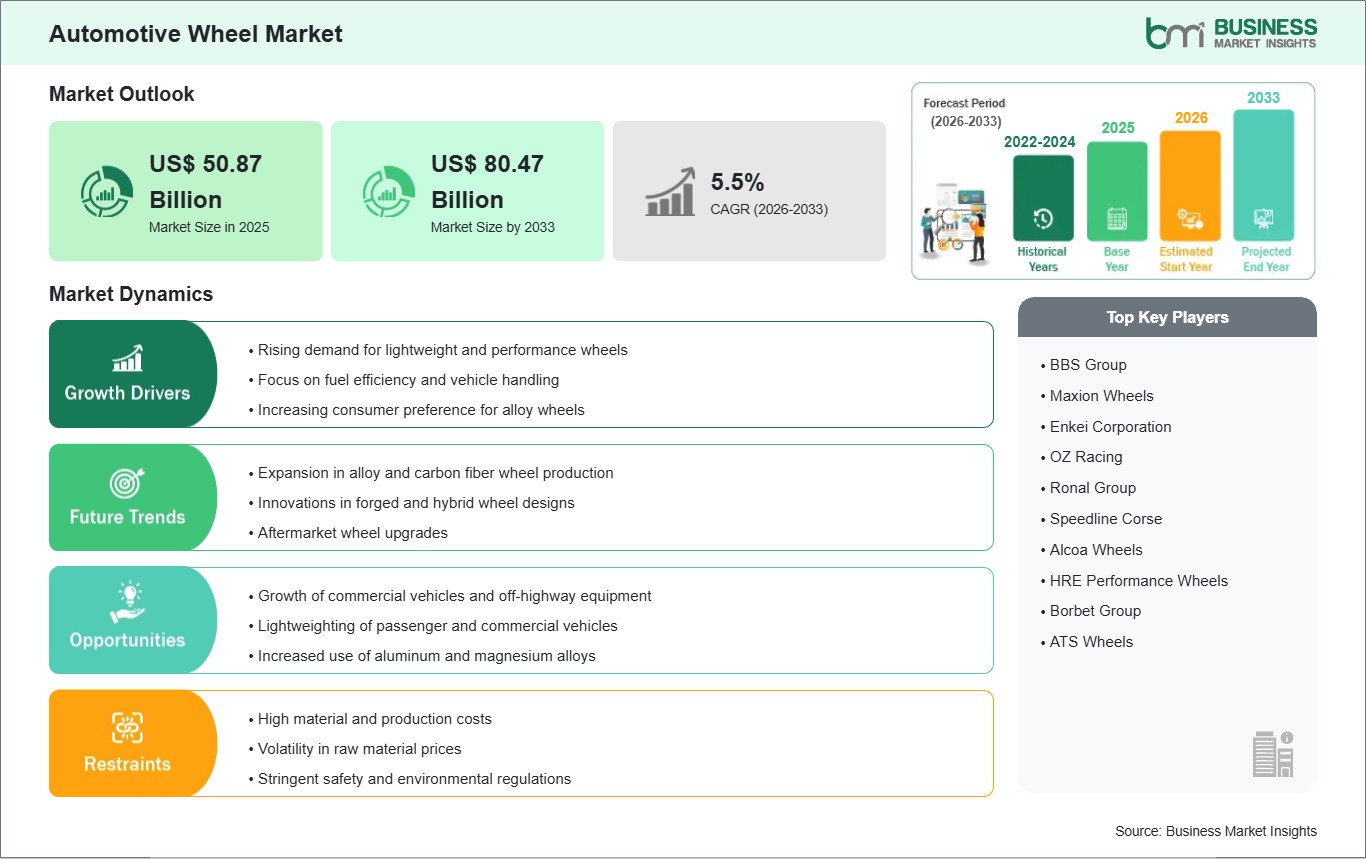

The Automotive Wheel Market size is expected to reach US$ 80.47 Billion by 2033 from US$ 50.87 Billion in 2025. The market is estimated to record a CAGR of 5.90% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global automotive wheel market is driven by the rising demand for lightweight, durable, and high-performance wheels that enhance vehicle safety, fuel efficiency, and aesthetics. Automotive wheels are critical for vehicle performance, influencing handling, braking, and overall ride quality. Innovations in materials and manufacturing processes, such as aluminum alloy and carbon fiber wheels, are reshaping the market by reducing weight while maintaining strength and durability.

The market growth is also supported by the increasing production of passenger and commercial vehicles worldwide. The growing preference for alloy wheels in premium segments and aftermarket upgrades is contributing to market expansion. In addition, regulations promoting fuel efficiency and reduced emissions are encouraging automakers to adopt lightweight wheel materials, such as aluminum and magnesium alloys, to decrease overall vehicle weight.

Competitive dynamics focus on innovation in wheel design, material technology, and manufacturing methods. Companies are introducing forged and hybrid wheels with improved strength-to-weight ratios. Strategic partnerships with OEMs and aftermarket distributors help expand market reach and increase brand visibility. Sustainability initiatives, such as recycled alloy usage and eco-friendly coatings, are becoming increasingly important for market players.

Automotive Wheel Market - Strategic Insights:

Get more information on this report

Automotive Wheel Market Segmentation Analysis:

Key segments that contributed to the derivation of the automotive wheel market analysis are rim size, material, end-use, vehicle type, vehicle class, and off-highway applications.

By rim size, the market is segmented into 13–15 inch, 16–18 inch, 19–21 inch, and above 21 inch. The 16–18 inch segment dominated the market in 2025.

By material, the market is segmented into steel, alloy (aluminum & magnesium), carbon fiber, and other materials. The alloy (aluminum & magnesium) segment dominated the market in 2025.

By end-use, the market is segmented into original equipment (OE) and aftermarket. The original equipment (OE) segment dominated the market in 2025.

By vehicle type, the market is segmented into passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs). The passenger vehicles segment dominated the market in 2025.

By vehicle class, the market is segmented into economy, mid-priced, and luxury. The mid-priced segment dominated the market in 2025.

In terms of off-highway applications, the market is segmented into construction & mining equipment and agricultural tractors. The construction & mining equipment segment dominated the market in 2025.

Automotive Wheel Market Drivers and Opportunities:

Rising Demand for Lightweight and Performance Wheels

The automotive wheel market is expanding due to the growing demand and focus towards developing lightweight yet high-performance wheels. Lightweight wheels such as those made from aluminum and magnesium alloys allow manufacturers to decrease the unsprung weight of a vehicle, which improves handling, acceleration, braking, and overall vehicle dynamics. Reducing the overall weight of a vehicle allows for greater fuel efficiency and results in lower carbon emissions, thus meeting sustainability objectives on a global level.

Another factor contributing to the growth of the automotive wheel market is the growing consumer preference for alloy wheels on passenger cars and aftermarket accessory upgrades. Alloy wheels have superior looks and offer better performance than their steel counterparts. Alloy wheels are generally lighter than steel wheels, are not susceptible to rust, provide enhanced braking system performance due to superior thermal conductivity, and the addition of advanced manufacturing processes such as forging and flow forming will allow manufacturers to produce even stronger and lighter wheels matching or exceeding the performance characteristics of existing designs.

In addition to lighter and more efficient alloy wheels, manufacturers are developing new manufacturing techniques that facilitate the production of carbon fiber and hybrid composite wheels which provide incredible weight savings while maintaining high structural strength. As OEMs continue to place importance on fuel efficiency and performance characteristics of vehicles, lightweight and technologically advanced wheels will continue to increase in market share in all vehicle categories.

Growth of Commercial Vehicles and Off-Highway Equipment

The rise of commercial vehicle (CV) segments, including LCVs and HCVs, as well as off-highway applications including construction, mining, and farm equipment, has created a huge opportunity for the automotive wheel market. Wheels used by commercial and off-highway vehicles must be able to support high loads, be durable, and withstand tough operational conditions.

The latest innovations in material and design of alloy and steel wheels for heavy-duty vehicles will deliver increasingly better strength-to-weight performance, thus extending wheel life and reducing maintenance costs. In the construction and mining industries, wheels are built to be able to handle extreme load capabilities, rough terrains, and harsh environments.

The demand for high-performance, durable wheels for use in off-highway applications is also increasing because of the increase in urban infrastructure development, rapid urbanization, and increased use of mechanized agriculture in developing countries.

The aftermarket segment will also have more growth because vehicle owners are upgrading or replacing wheels to increase their vehicle's functionality or appearance. Partnerships between original equipment manufacturers (OEMs) and distributors will continue to expand the potential for manufacturers to reach new customers and generate additional revenues through these types of partnerships.

As global vehicle production continues to increase, we expect the automotive wheel market will experience continued growth as the use of off-highway equipment grows.

Automotive Wheel Market Size and Share Analysis:

The Automotive Wheel Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within rim size, material, end-use, vehicle type, vehicle class, and off-highway applications, offering insights into their contribution to overall market performance.

By rim size, the 16–18 inch subsegment dominated the market in 2025, driven by widespread use in mid-sized passenger vehicles.

Based on material, the alloy (aluminum & magnesium) subsegment dominated the market in 2025, driven by its lightweight and high-strength properties.

In terms of end-use, the original equipment (OE) subsegment dominated the market in 2025, driven by high integration of OEM wheels in vehicle production.

By vehicle type, the passenger vehicles subsegment dominated the market in 2025, driven by high global production.

Based on vehicle class, the mid-priced subsegment dominated the market in 2025, reflecting growing demand in mainstream consumer segments.

By off-highway applications, the construction & mining equipment subsegment dominated the market in 2025, driven by increasing industrial and infrastructure activities.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BBS Group

Maxion Wheels

Enkei Corporation

OZ Racing

Ronal Group

Speedline Corse

Alcoa Wheels

HRE Performance Wheels

Borbet Group

ATS Wheels

Get more information on this report

Automotive Wheel Market Report Coverage and Deliverables:

The "Automotive Wheel Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Automotive Wheel Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Automotive Wheel Market trends, as well as drivers, restraints, and opportunities

Automotive Wheel Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Automotive Wheel Market

Detailed company profiles, including SWOT analysis

Automotive Wheel Market Geographic Insights:

The geographical scope of the Automotive Wheel Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The adoption and demand for automotive wheels vary across regions, influenced by automotive production, vehicle ownership trends, and regulatory standards. In North America, the market is driven by advanced vehicle manufacturing, aftermarket penetration, and increasing demand for alloy wheels.

In Europe, stringent environmental and safety regulations encourage the adoption of lightweight and high-strength wheel solutions. Growth in luxury and mid-priced vehicle segments further supports market expansion.

Asia Pacific is the fastest-growing region, fueled by large-scale automotive production in China, India, and Japan, rising vehicle ownership, and increasing infrastructure development for off-highway applications.

The Middle East & Africa and South & Central America are experiencing moderate growth, driven by rising vehicle sales, commercial fleet expansion, and off-highway equipment adoption. Across all regions, technological innovation, sustainability goals, and regulatory requirements continue to shape market dynamics.

Get more information on this report

Automotive Wheel Market Research Report Guidance:

The report includes qualitative and quantitative data in the Automotive Wheel Market across rim size, material, end-use, vehicle type, vehicle class, off-highway applications, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Automotive Wheel Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Automotive Wheel Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Automotive Wheel Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 13 cover Automotive Wheel Market segments by rim size, material, end-use, vehicle type, vehicle class, off-highway applications, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 14 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 15 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 16 provides detailed profiles of the major companies operating in the Automotive Wheel Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 17, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Automotive Wheel Market News and Key Development:

The Automotive Wheel Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the automotive wheel market are:

In October 2025, BBS Group launched a new range of lightweight forged alloy wheels for premium passenger vehicles, enhancing fuel efficiency and performance.

In July 2025, Maxion Wheels introduced innovative steel and aluminum wheels for commercial and off-highway vehicles, focusing on durability and load-bearing capacity.

Key Sources Referred:

International Organization of Motor Vehicle Manufacturers (OICA)European Automobile Manufacturers Association (ACEA)International Energy Agency (IEA)United States Environmental Protection Agency (EPA)World Steel Association

The List of Companies - Automotive Wheel Market

BBS Group

Maxion Wheels

Enkei Corporation

OZ Racing

Ronal Group

Speedline Corse

Alcoa Wheels

HRE Performance Wheels

Borbet Group

ATS Wheels

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Automotive Wheel Market?

The Automotive Wheel Market is valued at US$ 50.87 Billion in 2025, it is projected to reach US$ 80.47 Billion by 2033.

What is the CAGR for Automotive Wheel Market by (2026 - 2033)?

As per our report Automotive Wheel Market, the market size is valued at US$ 50.87 Billion in 2025, projecting it to reach US$ 80.47 Billion by 2033. This translates to a CAGR of approximately 5.90% during the forecast period.

What segments are covered in this report?

The Automotive Wheel Market report typically cover these key segments-

Material (Steel, Alloy (Aluminum & Magnesium), Carbon Fiber, Other Materials)

End-Use (Original Equipment (OE), Aftermarket)

Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs))

What is the historic period, base year, and forecast period taken for Automotive Wheel Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Automotive Wheel Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Automotive Wheel Market?

The Automotive Wheel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BBS Group

Maxion Wheels

Enkei Corporation

OZ Racing

Ronal Group

Speedline Corse

Alcoa Wheels

HRE Performance Wheels

Borbet Group

ATS Wheels

Who should buy this report?

The Automotive Wheel Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Automotive Wheel Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Automotive Wheel Market

Get Free Sample For Automotive Wheel Market