01

Market Summery

Executive Summary and Global Market Analysis

Automotive safety systems comprise integrated technologies and protective mechanisms designed to reduce collision risks, minimize occupant injuries, and enhance vehicle control during critical driving conditions. These systems are a combination of electronic sensors, mechanical actuating functions, and computerized intervention features in cars and commercial vehicles. Active safety systems will help in preventing accidents, while passive safety systems work towards minimizing the effects of impact during an accident.

In the context of the growing need for safety measures among automobiles in light of new safety legislation as well as consumers’ demands, carmakers are making an effort to integrate advanced safety measures into their cars. With increasing urban traffic and increased frequency of use on roads, the need for monitoring systems that also provide driver assistance is becoming increasingly important.

Passenger cars will also be responsible for significant integration volumes due to consumer preference for advanced levels of comfort and safety systems. Original Equipment Manufacturers' (OEMs') purchasing activities have remained active since safety systems are increasingly being integrated into vehicles in the production process rather than after-sales activities. The trend in technology development in the industry has been toward sensor fusion, predictive analysis, and assessing the environment of the vehicle in real time.

There has been an improvement in automated intervention systems that integrate braking systems, cameras, radar sensors, and electronic stability controls. Electrified platforms of vehicles have further pushed software-driven safety systems as a result of electronic control and connectivity systems. The focus is on providing scalable safety solutions that will fit across various vehicle segments and powertrains. Differentiation in products will rely on software precision, parts reliability, and integration into driver assistance systems.

03

Segment Analysis

Automotive Safety Systems Market Segmentation

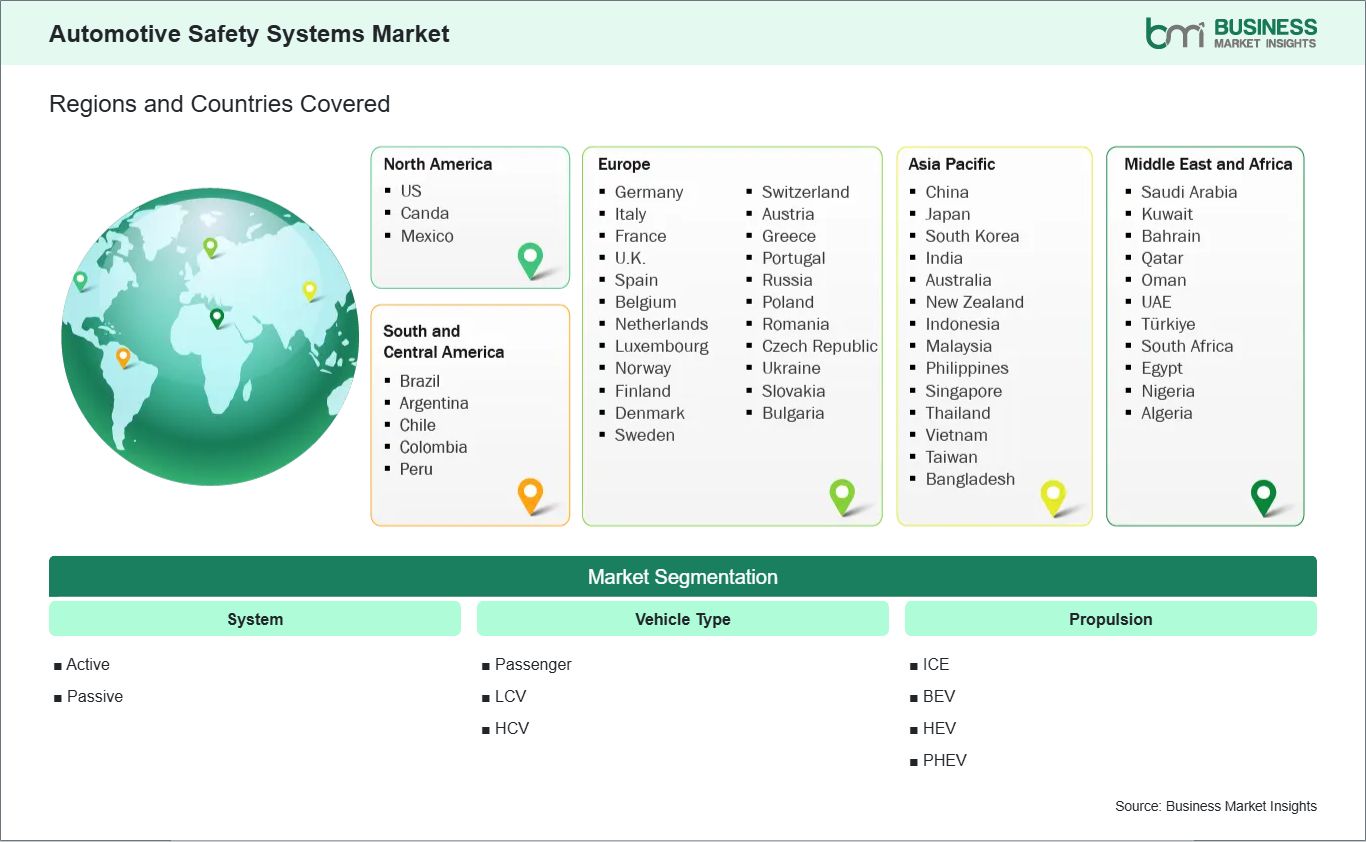

The automotive safety systems market is segmented based on, system, vehicle type, propulsion, and end user reflecting the growing emphasis on vehicle safety, regulatory compliance, and integration of advanced driver assistance systems across modern automotive platforms.

By System

- ABS - Enhances braking stability during abrupt deceleration on uneven road surfaces.

- ESC - Improves directional control during sharp turns and slippery driving conditions.

- BSD - Detects adjacent vehicle movement during lane transition maneuvers.

- LDWS - Alerts drivers regarding unintended lane departures on highways.

- TPMS - Monitors tire pressure variations to improve driving safety consistency.

- Airbags - Reduce occupant injury severity during frontal and side-impact collisions.

- Seatbelts - Maintain passenger restraint during sudden vehicle movement disruptions.

- Whiplash - Minimizes neck strain through optimized seating and headrest configurations.

By Vehicle Type

- Passenger - Integrates multi-layered safety technologies for occupant protection and convenience.

- LCV - Supports safer urban logistics and regional transportation operations.

- HCV - Addresses operational safety requirements across long-distance freight transportation.

By Propulsion

- ICE - Maintains broad safety integration across conventional vehicle architectures.

- BEV - Utilizes software-centric safety coordination with electronic control platforms.

- HEV - Combines electronic safety monitoring with hybrid drivetrain management systems.

- PHEV - Supports advanced driver assistance compatibility alongside electrified propulsion functions.

By End-user

- OEM - Embeds safety technologies directly within factory vehicle assembly processes.

- Aftermarket - Provides retrofit solutions for upgraded vehicle protection capabilities.

04

Market Forces

Automotive Safety Systems Market Drivers and Opportunities

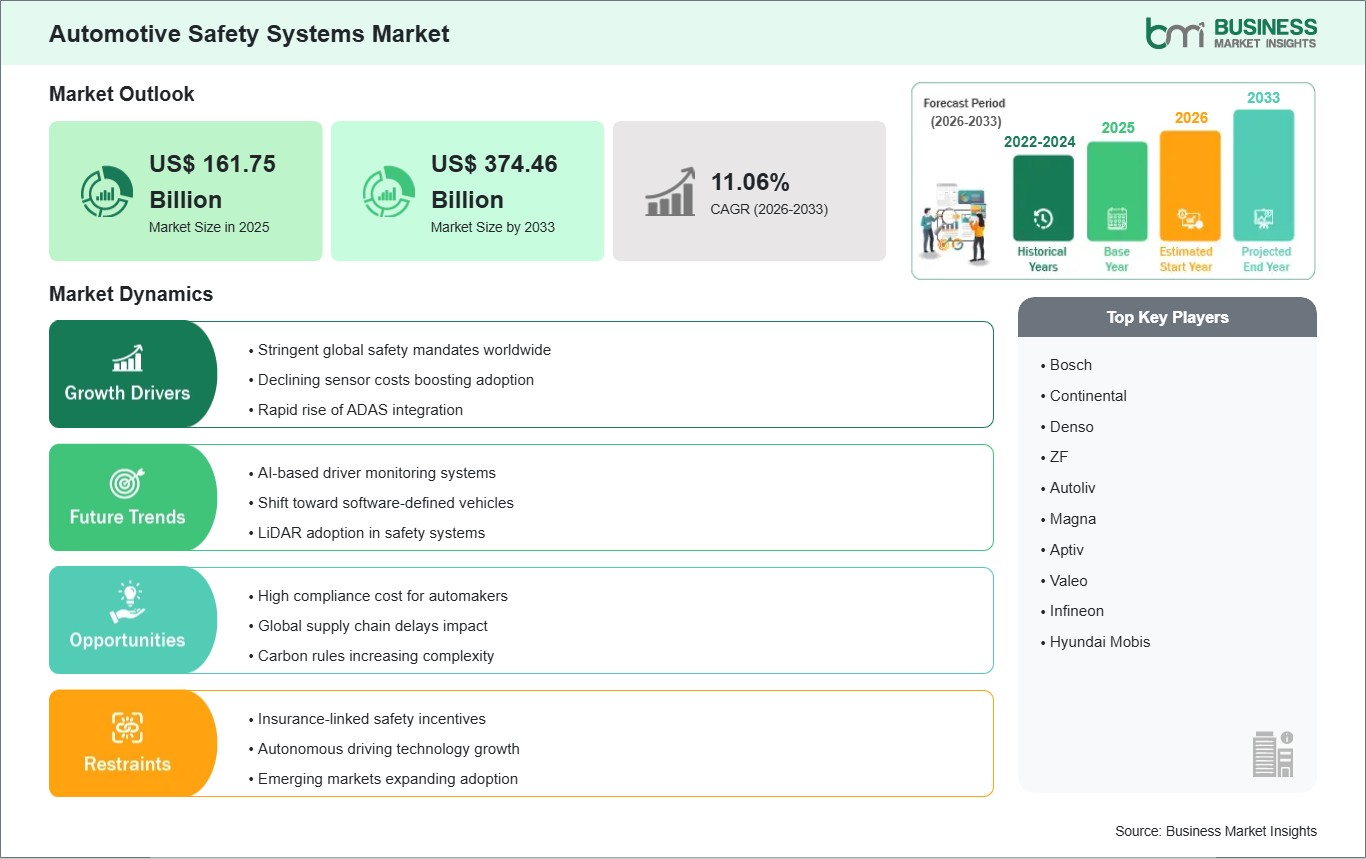

Stringent global safety mandates worldwide

The government’s transportation agencies are now using more rigorous safety designs for their vehicles to ensure that road accidents are minimized and higher safety standards are achieved. The regulators have begun mandating the use of sophisticated safety technology systems such as braking systems, stability controls, and other monitoring systems. Manufacturers are now fast-tracking these kinds of safety systems in their new model designs.

Regulations are changing the way that product development focuses within the automotive industry. Companies are redesigning their vehicle platforms to incorporate new standards related to active and passive safety features without affecting efficiency. The growing congruence of safety procedures among different regions is making it easier to create standards for technologies internationally. This is good news for companies that manufacture safety systems and electronics.

Insurance-linked safety incentives

Increasingly, premium packages are being designed in a manner that correlates with car safety and its ability to avoid accidents. Cars fitted with sophisticated monitoring and accident prevention systems tend to be favored with preferential treatment by insurers. This practice has made people opt for cars with better safety features when buying new cars. The safety-based insurance model is therefore encouraging intelligent driver assistance systems.

Expansions in the future for the ecosystem of connected vehicles may foster coordination among the insurers, telematics firms, and automobile producers. Techniques that analyze driver behavior and predict risks in real time might enable the use of an individualized insurance program based on performance factors in terms of safety. This trend would result in the faster implementation of technological systems in both passenger and commercial segments.

05

Size and Share Analysis

Automotive Safety Systems Market Size and Share Analysis

The Automotive Safety Systems Market is projected to grow from US$ 161.75 Billion in 2025 to US$ 374.46 Billion by 2033 , registering a CAGR of 11.06% from 2026 to 2033. The market expansion is supported by increasing integration of advanced driver assistance technologies, stringent road safety regulations, and rising deployment of sensor-driven electronic control systems enhancing vehicle stability and collision prevention performance.

By system, active safety technologies account for a significant share due to their real-time intervention capability and integration with advanced driver assistance functions. Systems such as ABS, ESC, and LDWS are increasingly embedded in modern vehicle architectures to enhance operational stability. Passive safety solutions maintain steady penetration as airbags, seatbelts, and whiplash protection remain mandatory across most vehicle categories. Continuous electronic integration across braking and stability modules further strengthens active system dominance.

By vehicle type, passenger vehicles dominate market utilization owing to large-scale production volumes and rising consumer preference for enhanced safety configurations. Light commercial vehicles maintain notable adoption supported by urban logistics expansion and last-mile delivery requirements. Heavy commercial vehicles continue integrating advanced safety systems to reduce operational risk in long-haul freight operations. Fleet operators increasingly prioritize driver assistance technologies to improve road safety compliance and reduce incident exposure.

By propulsion, internal combustion engine vehicles hold a substantial share due to their widespread global fleet presence and established manufacturing base. Battery electric vehicles are expanding rapidly with higher integration of sensor-driven safety architectures and centralized electronic control systems. Hybrid electric vehicles maintain steady adoption supported by dual powertrain safety coordination systems. Plug-in hybrid vehicles are witnessing growing integration of predictive safety technologies aligned with electrified mobility platforms.

By end-user, OEMs account for a major market share as safety systems are increasingly integrated during vehicle assembly rather than aftermarket installation. Standardization of safety regulations has strengthened OEM-level adoption across global manufacturing facilities. Aftermarket deployment continues expanding in regions with aging vehicle fleets and retrofit safety demand. Rising awareness of vehicle protection features further supports gradual expansion of aftermarket safety system installations.

07

Report Coverage

Automotive Safety Systems Market Report Coverage and Deliverables

The "Automotive Safety Systems Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- The market size and forecast at global, regional, and country levels for all market segments covered under the scope

- The market trends, as well as drivers, restraints, and opportunities

- The market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Automotive Safety Systems Market Geographic Insights

The Automotive Safety Systems Market shows diverse regional adoption patterns influenced by advancements in imaging technologies, increasing demand for immersive visual experiences, and rising adoption of automation and smart devices.

North America demonstrates strong penetration of advanced automotive safety technologies due to established regulatory enforcement and elevated consumer preference for technologically equipped vehicles. Vehicle manufacturers in the region continue integrating sophisticated driver assistance capabilities across passenger and commercial fleets. Insurance-linked vehicle assessment programs and highway safety initiatives further support widespread incorporation of active safety modules throughout regional automotive production activities.

The Asia Pacific region emerges as an important center of manufacturing and deployment of auto safety systems because of growing vehicle manufacturing capabilities and urban transit systems. There has been a greater use of electronic safety systems by regional automakers on their mainstream vehicles as per new safety standards. In addition, rising manufacture of electrified cars in key Asian economies contributes to advancements in safety software architectures and sensing systems.

Europe maintains strong emphasis on advanced occupant protection standards and intelligent mobility frameworks across automotive manufacturing operations. Vehicle producers across the region continue focusing on integrated safety ecosystems combining predictive analytics, braking assistance, and real-time monitoring functions. Emerging markets within the Middle East, Africa, and South and Central America are gradually expanding deployment of automotive safety technologies as transportation modernization programs and regulatory alignment initiatives continue progressing.

10

Industry Activity

Recent Developments

The automotive safety systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the automotive safety systems market are:

- In September 2025, the Automotive Research Association of India (ARAI) announced the completion of India’s first ADAS Test City in Pune, a 20-acre facility replicating Indian road networks to validate advanced driver assistance systems under real-world conditions.

- In November 2022, Continental AG announced the integration of Ambarella’s CV3 system-on-chip family into its ADAS solutions to enhance vehicle safety, sensor fusion, and automated driving performance.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade Indicators

World Trade Organization (WTO)

International Monetary Fund (IMF)

International Trade Administration (ITA)

Company Websites

Company Annual Reports

Company Investor Presentations