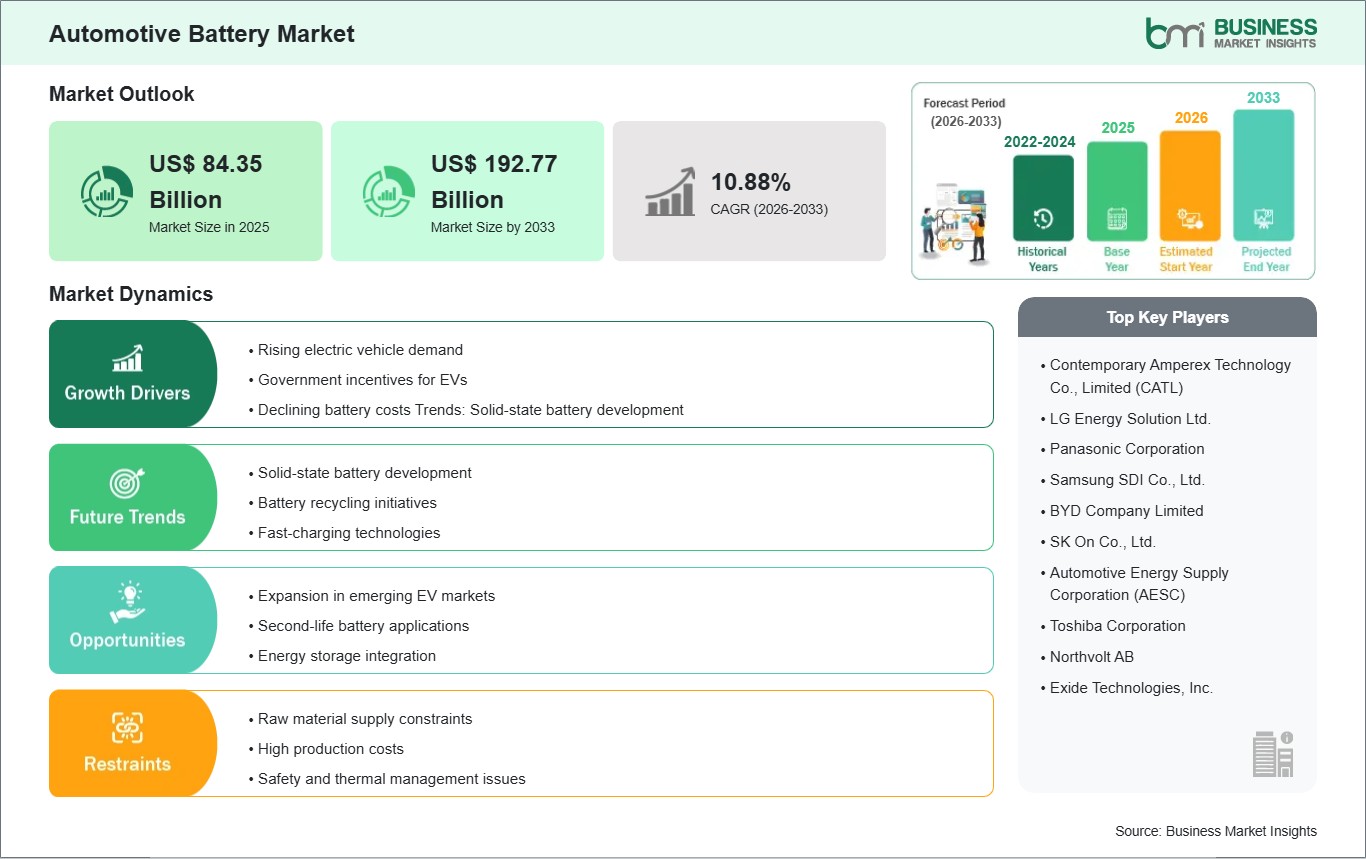

The Automotive Battery Market size is expected to reach US$ 192.77 Billion by 2033 from US$ 84.35 Billion in 2025. The market is estimated to record a CAGR of 10.88% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Automotive batteries refer to the integrated energy storage systems engineered to provide the high-surge electrical current required to start internal combustion engines (SLI) and the sustained power necessary for electric vehicle (EV) propulsion. By utilizing diverse electrochemical architectures, ranging from traditional lead-acid and enhanced absorbent glass mat (AGM) to high-capacity lithium-ion and emerging sodium-ion chemistries, these systems serve as the critical power hub for a vehicle's increasing electronic load. This technology is fundamental to the operation of modern start-stop systems, advanced driver-assistance systems (ADAS), and the global transition toward zero-emission mobility. Market expansion is being propelled by the rapid electrification of passenger and commercial fleets, the rising global vehicle parc leading to a robust aftermarket replacement cycle, and significant institutional subsidies.

However, several factors may restrain market progression. The high capital intensity associated with the procurement of critical raw materials, specifically lithium, cobalt, and nickel, remains a primary hurdle, as these minerals are often subject to extreme price volatility and geopolitical supply risks. The industry also faces technical challenges regarding energy density vs. safety, where high-performance cells must be rigorously engineered to prevent thermal runaway and ensure stability under diverse climatic conditions. Additionally, stringent environmental regulations governing the recycling and disposal of lead-acid and lithium-based units increase production costs annually for many manufacturers. These hurdles, compounded by the complexity of integrating next-generation solid-state technology into mass-production workflows, increase the total operational risk and necessitate a cautious approach to large-scale commercialization.

Despite these hurdles, the market outlook remains highly favorable as the sector undergoes a chemistry diversification phase. Opportunities are emerging through the adoption of sodium-ion batteries, which offer a lower-cost, sustainable alternative for short-range urban mobility and 2-wheelers by reducing dependency on scarce minerals. The shift toward solid-state and semi-solid batteries is gaining significant traction; several automotive manufacturers have commenced on-vehicle validation for high-specific-energy cells that target ranges exceeding 1,000 kilometers. Furthermore, the growth of Battery-as-a-Service (BaaS) subscription models and AI-driven lifecycle diagnostics aligns with global goals for circular economy practices and improved consumer affordability. Collectively, these innovations position the automotive battery industry for sustained long-term development as a cornerstone of the resilient, connected, and electrified global transportation infrastructure.

Automotive Battery Market - Strategic Insights:

Get more information on this report

Automotive Battery Market Segmentation Analysis:

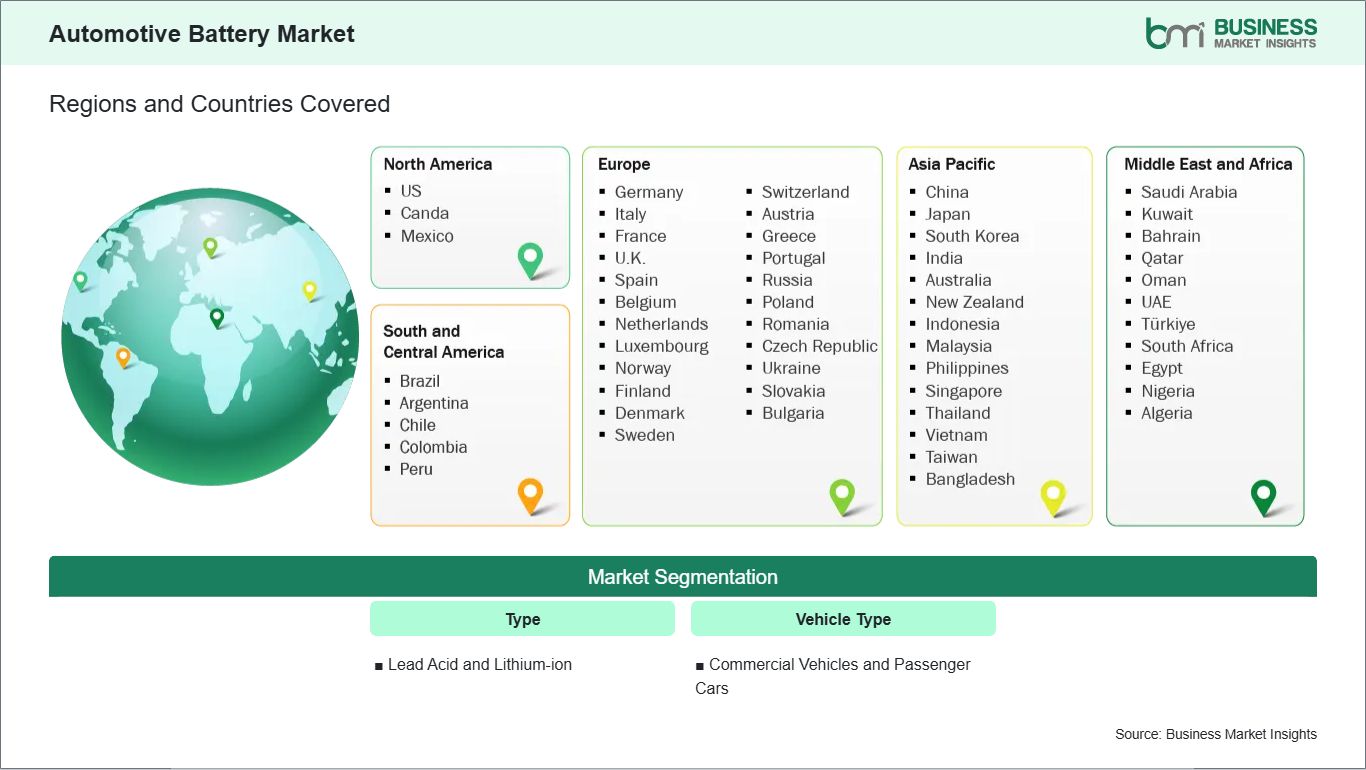

Key segments that contributed to the derivation of the Automotive Battery market analysis are type and vehicle type.

By Type, the market is segmented into Lead Acid and Lithium-ion.

By Vehicle Type, the market is divided into Commercial Vehicles and Passenger Cars.

Automotive Battery Market Drivers and Opportunities:

Rising Demand for Electrification, Sustainability, and Performance

The automotive battery market is being driven by the accelerating shift toward vehicle electrification, sustainability goals, and performance optimization. With governments worldwide enforcing stricter emission regulations and promoting clean mobility, automakers are investing heavily in electric vehicles (EVs) and hybrid models, fueling demand for advanced battery technologies. Rising consumer awareness of climate change and preference for eco‑friendly transportation are amplifying adoption, while incentives and subsidies for EV purchases further reinforce growth. The expansion of charging infrastructure and smart grid integration is also propelling investment in high‑capacity, fast‑charging batteries. Additionally, technological advancements in lithium‑ion, solid‑state, and alternative chemistries are improving energy density, safety, and lifecycle performance, making batteries more reliable and cost‑effective. The growing popularity of connected and autonomous vehicles is driving demand for batteries that support high power loads and continuous operation. Collectively, electrification, sustainability priorities, and performance requirements are fueling sustained growth in the global automotive battery market.

Rising Integration of Solid‑State, Recycling, and Emerging Applications

Opportunities in the automotive battery market are expanding through the integration of solid‑state technologies, recycling initiatives, and emerging applications. Solid‑state batteries are opening lucrative opportunities by offering higher energy density, faster charging, and improved safety compared to conventional lithium‑ion systems. Recycling and second‑life applications are gaining traction, as sustainability trends encourage circular economy practices and reduce dependence on raw material mining. The growing emphasis on renewable energy integration is fueling demand for automotive batteries that double as energy storage units, supporting vehicle‑to‑grid (V2G) applications. Emerging opportunities in commercial fleets, public transport, and shared mobility are also driving innovation, as these sectors require scalable, cost‑effective battery solutions to improve operational efficiency. Additionally, advancements in AI‑enabled battery management systems are creating new pathways for adoption, where predictive analytics optimize performance and extend battery life. Vendors who focus on solid‑state innovation, recycling ecosystems, and smart energy integration are well‑positioned to capture growth. The convergence of electrification, sustainability, and digital energy solutions underscores a transformative trajectory for the global automotive battery market.

Automotive Battery Market Size and Share Analysis:

The Automotive Battery market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within type and vehicle type, offering insights into their contribution to overall market performance.

Based on Type, the Lead Acid subsegment holds a strong presence, driven by its affordability, reliability, and widespread use in conventional vehicles. Lead acid batteries remain indispensable for starting, lighting, and ignition (SLI) functions, offering proven technology and cost‑effective solutions for mass‑market adoption. However, the Lithium‑ion subsegment is essential for modern electric and hybrid vehicles, providing higher energy density, longer cycle life, and faster charging capabilities. Lithium‑ion batteries anchor demand in sustainable mobility, supporting the transition toward electrification and reduced emissions. While lead acid dominates traditional applications, lithium‑ion drives innovation and growth in next‑generation automotive power systems.

Automotive Battery Market Report Coverage and Deliverables:

The "Automotive Battery Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Automotive Battery market size and forecast at global, regional, and country levels for all market segments covered under the scope

Automotive Battery market trends, as well as drivers, restraints, and opportunities

Automotive Battery market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Automotive Battery market

Detailed company profiles, including SWOT analysis

Automotive Battery Market Geographic Insights:

The geographical scope of the Automotive Battery market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America maintains a preeminent position within the global industry, a status reinforced by the region's advanced automotive manufacturing base and a decisive transition toward high-capacity energy storage. The regional landscape is characterized by high-density investments in the United States and Canada, where the expansion of domestic gigafactories has become a strategic priority to secure the local supply chain. This market leadership is supported by a robust corporate ecosystem that increasingly favors high-performance lithium-ion and emerging solid-state chemistries to satisfy the requirements of both passenger electric vehicles and heavy-duty commercial fleets. Local consumer trends reflect a unique dual-track demand for both convenience and long-range reliability. While battery electric vehicle adoption remains a core driver, there is a significant resurgence in the popularity of hybrid electric vehicles, which serve as a practical bridge for consumers concerned about charging infrastructure gaps. Additionally, the aftermarket segment continues to show resilience, driven by a high density of internal combustion engine vehicles that require traditional, maintenance-free starting batteries. This behavioral transition is further influenced by an increasing preference for smart battery management systems that provide real-time health diagnostics directly to the user's mobile device.

Regulatory influences play a critical role, particularly through federal initiatives that provide substantial tax credits and subsidies for batteries manufactured with a high percentage of domestic components. Stringent environmental mandates regarding lead-acid production and recycling have also prompted significant capital investments in cleaner smelting and recovery facilities. As the region continues to prioritize energy independence, the evolution of standardized recycling protocols and the implementation of state-level zero-emission mandates are expected to remain primary drivers for ensuring the long-term sustainability and competitiveness of North American automotive battery networks.

Get more information on this report

Automotive Battery Market Research Report Guidance:

The report includes qualitative and quantitative data in the Automotive Battery market across type, vehicle type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Automotive Battery market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Automotive Battery market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Automotive Battery market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Automotive Battery market segments by type, vehicle type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Automotive Battery market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Automotive Battery Market News and Key Development:

The Automotive Battery market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Automotive Battery market are:

In March 2026, MATTER Motor Works partnered with Iontra Inc to integrate Iontra’s real-time battery intelligence and adaptive charging into MATTER’s AI-Defined Vehicle (AIDV) platform. This collaboration enables AI-governed battery management, improving safety, lifespan, and charging efficiency for electric two-wheelers, marking a major step forward in intelligent EV energy systems.

In February 2026, Karma Automotive Inc partnered with Factorial Inc to launch the first U.S. commercial solid-state battery program for passenger vehicles. Factorial’s FEST® technology will power Karma’s next-generation electric platform, starting with the Karma Kaveya super-coupe, enhancing energy density, range, and efficiency while leveraging existing lithium-ion manufacturing lines for scalable U.S. production.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Automotive Battery Market?

The Automotive Battery Market is valued at US$ 84.35 Billion in 2025, it is projected to reach US$ 192.77 Billion by 2033.

What is the CAGR for Automotive Battery Market by (2026 - 2033)?

As per our report Automotive Battery Market, the market size is valued at US$ 84.35 Billion in 2025, projecting it to reach US$ 192.77 Billion by 2033. This translates to a CAGR of approximately 10.88% during the forecast period.

What segments are covered in this report?

The Automotive Battery Market report typically cover these key segments-

Type (Lead Acid and Lithium-ion)

Vehicle Type (Commercial Vehicles and Passenger Cars)

What is the historic period, base year, and forecast period taken for Automotive Battery Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Automotive Battery Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Automotive Battery Market?

The Automotive Battery Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Automotive Battery Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Automotive Battery Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Automotive Battery Market

Get Free Sample For Automotive Battery Market