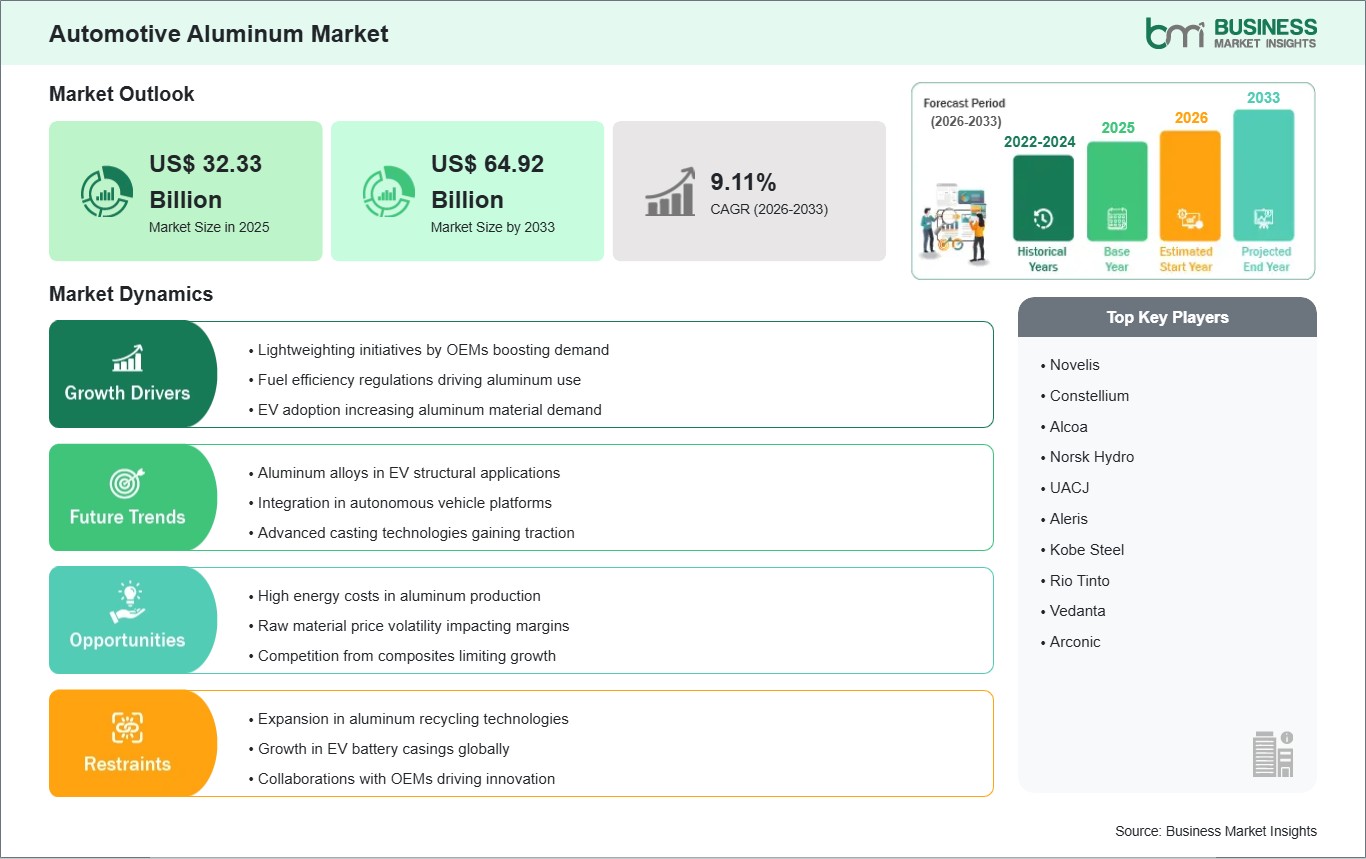

The Automotive Aluminum market size is expected to reach US$ 64.92 billion by 2033 from US$ 32.33 billion in 2025. The market is estimated to record a CAGR of 9.11% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Automotive aluminum is widely used in vehicle manufacturing to reduce weight, improve fuel efficiency, and enhance overall vehicle performance. It is available in various forms such as cast aluminum, rolled aluminum, and extruded aluminum, each designed for specific automotive applications. These materials are commonly used in engines, wheels, body panels, and chassis components. The market is growing as automotive manufacturers focus on lightweight vehicle designs, stricter fuel economy regulations, and increasing production of electric vehicles. The demand for aluminum continues to rise because it offers a combination of strength, corrosion resistance, and recyclability that supports modern vehicle development.

There are some challenges that could slow market growth. Aluminum production is energy intensive, and fluctuations in raw material and energy costs can affect manufacturing expenses. The higher cost of aluminum compared to traditional steel can limit adoption in some cost-sensitive vehicle segments. Automotive manufacturers also face technical challenges when integrating aluminum into complex vehicle structures, requiring specialized joining and fabrication techniques. Supply chain disruptions and volatility in global commodity markets may further affect material availability and pricing. These factors can create challenges for manufacturers seeking to expand aluminum usage across vehicle platforms.

Even with these challenges, the market is expected to grow as the automotive industry moves toward lighter, more efficient, and environmentally sustainable vehicles. New opportunities are emerging through advancements in aluminum processing technologies, recycling methods, and alloy development. Electric vehicle manufacturers are increasingly using aluminum to improve battery efficiency and extend driving range. Research into high-strength aluminum materials is also supporting the development of safer and more durable vehicle structures. As sustainability and vehicle efficiency remain key priorities, automotive aluminum is expected to play an increasingly important role in future vehicle manufacturing.

Automotive Aluminum Market - Strategic Insights:

Get more information on this report

Automotive Aluminum Market Segmentation Analysis:

The Automotive Aluminum market is segmented based on product type, application, and vehicle type, reflecting the growing use of lightweight materials across modern vehicle manufacturing.

By Product Type

Cast Aluminum: Widely used for complex automotive components requiring strength and durability

Rolled Aluminum: Preferred for body structures and panels due to its lightweight characteristics and formability

Extruded Aluminum: Used in structural applications that require high strength and design flexibility

By Application

Engine: Supports lightweight engine designs and improved thermal performance

Wheels: Enhances fuel efficiency and vehicle handling through weight reduction

Body Panels: Reduces overall vehicle mass while maintaining structural integrity

Chassis: Provides strength and durability for vehicle frameworks and structural systems

By Vehicle Type

Passenger Cars: Represents the largest demand segment due to high production volumes and efficiency requirements

Commercial Vehicles: Uses aluminum to improve payload capacity and fuel economy

EVs: Increasing adoption driven by the need for lightweight materials that enhance battery performance and driving range

Automotive Aluminum Market Drivers and Opportunities:

Rising Demand for Lightweight Vehicles and Emission Reduction

The demand for automotive aluminum is increasing as vehicle manufacturers focus on reducing vehicle weight to improve fuel efficiency and meet tightening environmental regulations. Lightweight materials help lower fuel consumption and reduce emissions while maintaining vehicle safety and performance standards. Governments across major automotive markets continue to implement regulations aimed at improving fuel economy and reducing carbon emissions, encouraging manufacturers to incorporate aluminum into vehicle designs.

The growing production of electric vehicles is also contributing to higher aluminum demand. Lightweight vehicle structures help improve battery efficiency and extend driving range, making aluminum an attractive material for electric mobility solutions. Automotive manufacturers are increasingly replacing heavier materials with aluminum in body panels, chassis systems, and powertrain components. As sustainability and energy efficiency become more important across the automotive industry, the use of automotive aluminum is expected to continue expanding across multiple vehicle categories and applications.

Advancements in Recycling and High-Strength Aluminum Technologies

The Automotive Aluminum market is creating new opportunities through innovations in recycling processes and advanced aluminum alloys. The automotive industry is placing greater emphasis on sustainable manufacturing practices, leading to increased use of recycled aluminum in vehicle production. Recycling aluminum requires significantly less energy compared to primary production, supporting environmental goals and reducing manufacturing costs.

At the same time, research into high-strength and advanced aluminum alloys is improving material performance and expanding potential applications. These innovations allow manufacturers to achieve greater weight reduction while maintaining durability and crash performance. Electric vehicle development is creating additional opportunities for specialized aluminum products that improve energy efficiency and structural integrity. Advances in manufacturing technologies, including precision casting and extrusion techniques, are further enhancing product capabilities. As the industry focuses on sustainability, lightweighting, and performance improvements, advanced aluminum solutions are expected to generate significant growth opportunities for the market.

Automotive Aluminum Market Size and Share Analysis:

The Automotive Aluminum market size is expected to reach US$ 64.92 billion by 2033 from US$ 32.33 billion in 2025. The market is estimated to record a CAGR of 9.11% from 2026 to 2033.

By product type, cast aluminum accounts for a significant share due to its widespread use in engine components, transmission housings, and structural parts. Rolled aluminum continues to witness strong demand in body panel applications, while extruded aluminum is gaining importance in chassis systems and structural components that require strength and design flexibility.

By application, body panels dominate the market owing to increasing efforts to reduce vehicle mass and improve efficiency. Engine applications continue to generate substantial demand because of aluminum's thermal properties and lightweight characteristics, while chassis and wheel applications are expanding as manufacturers focus on enhancing vehicle performance and durability.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Novelis

Constellium

Alcoa

Norsk Hydro

UACJ

Aleris

Kobe Steel

Rio Tinto

Vedanta

Arconic

Get more information on this report

Automotive Aluminum Market Report Coverage and Deliverables:

The "Automotive Aluminum Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Automotive Aluminum Market Geographic Insights:

The Automotive Aluminum Market shows diverse regional adoption patterns influenced by vehicle production levels, lightweight material demand, environmental regulations, and advancements in automotive manufacturing technologies.

North America, being a developed region, has a well-established automotive industry and a high rate of adoption of lightweight materials in vehicle production. The region comprises the United States and Canada, where manufacturers are investing in fuel-efficient and electric vehicle technologies. The region focuses on reducing vehicle emissions and improving energy efficiency through the use of advanced aluminum components. Strong manufacturing infrastructure, technological capabilities, and recycling systems support the widespread use of automotive aluminum across passenger cars, commercial vehicles, and electric vehicles.

Asia Pacific is growing significantly, driven by increasing vehicle production and expanding automotive manufacturing capabilities. The region comprises countries such as China, India, and Japan, where rising demand for fuel-efficient vehicles and rapid growth in electric mobility are creating strong opportunities for aluminum applications. The region focuses on improving manufacturing efficiency and supporting sustainable transportation initiatives. Expanding automotive supply chains, increasing industrial investments, and growing adoption of advanced materials continue to support market growth across the region.

Both regions are contributing significantly to the growth of the Automotive Aluminum Market, focusing on lightweight vehicle development, expanding electric vehicle production, and increasing adoption of sustainable manufacturing practices.

Get more information on this report

Automotive Aluminum Market Research Report Guidance:

The report includes qualitative and quantitative data pertaining to the Automotive Aluminum market, categorized by Product Type, Application, Vehicle Type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by Product Type, Application, Vehicle Type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Automotive Aluminum Market News and Key Development:

The Automotive Aluminum Market is analyzed using a mix of primary and secondary research sources, including corporate publications, industry associations, and verified databases. This approach ensures accurate tracking of innovation trends and strategic developments influencing the market.

In January 2026, Norsk Hydro and Mercedes-Benz successfully scaled their strategic supply partnership, integrating low-carbon aluminum into the structural chassis and body panel stampings of new electric vehicle programs. The specialized alloy matrix blends renewable-energy primary aluminum with at least 25% post-consumer recycled scrap, dropping production-phase emissions down to a fraction of the historical global average. The commercial rollout demonstrates the rapid transition from experimental foundry testing to full-scale vehicle assembly line integration to comply with upcoming global environmental regulations.

In April 2025, Nemak and Hydro strengthened their collaboration to advance low-carbon aluminum solutions for automotive manufacturing. The partnership focuses on increasing the use of post-consumer scrap and developing more sustainable foundry alloys for vehicle production. The initiative supports growing industry demand for lightweight and environmentally responsible aluminum materials used in automotive applications.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Automotive Aluminum Market

Novelis

Constellium

Alcoa

Norsk Hydro

UACJ

Aleris

Kobe Steel

Rio Tinto

Vedanta

Arconic

Frequently Asked Questions

How big is the Automotive Aluminum Market?

The Automotive Aluminum Market is valued at US$ 32.33 Billion in 2025, it is projected to reach US$ 64.92 Billion by 2033.

What is the CAGR for Automotive Aluminum Market by (2026 - 2033)?

As per our report Automotive Aluminum Market, the market size is valued at US$ 32.33 Billion in 2025, projecting it to reach US$ 64.92 Billion by 2033. This translates to a CAGR of approximately 9.11% during the forecast period.

What segments are covered in this report?

The Automotive Aluminum Market report typically cover these key segments-

Product Type (Cast Aluminum, Rolled Aluminum, Extruded Aluminum)

Application (Engine, Wheels, Body Panels, Chassis)

Vehicle Type (Passenger Cars, Commercial Vehicles, EVs)

What is the historic period, base year, and forecast period taken for Automotive Aluminum Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Automotive Aluminum Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Automotive Aluminum Market?

The Automotive Aluminum Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Novelis

Constellium

Alcoa

Norsk Hydro

UACJ

Aleris

Kobe Steel

Rio Tinto

Vedanta

Arconic

Who should buy this report?

The Automotive Aluminum Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Automotive Aluminum Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Automotive Aluminum Market

Get Free Sample For Automotive Aluminum Market