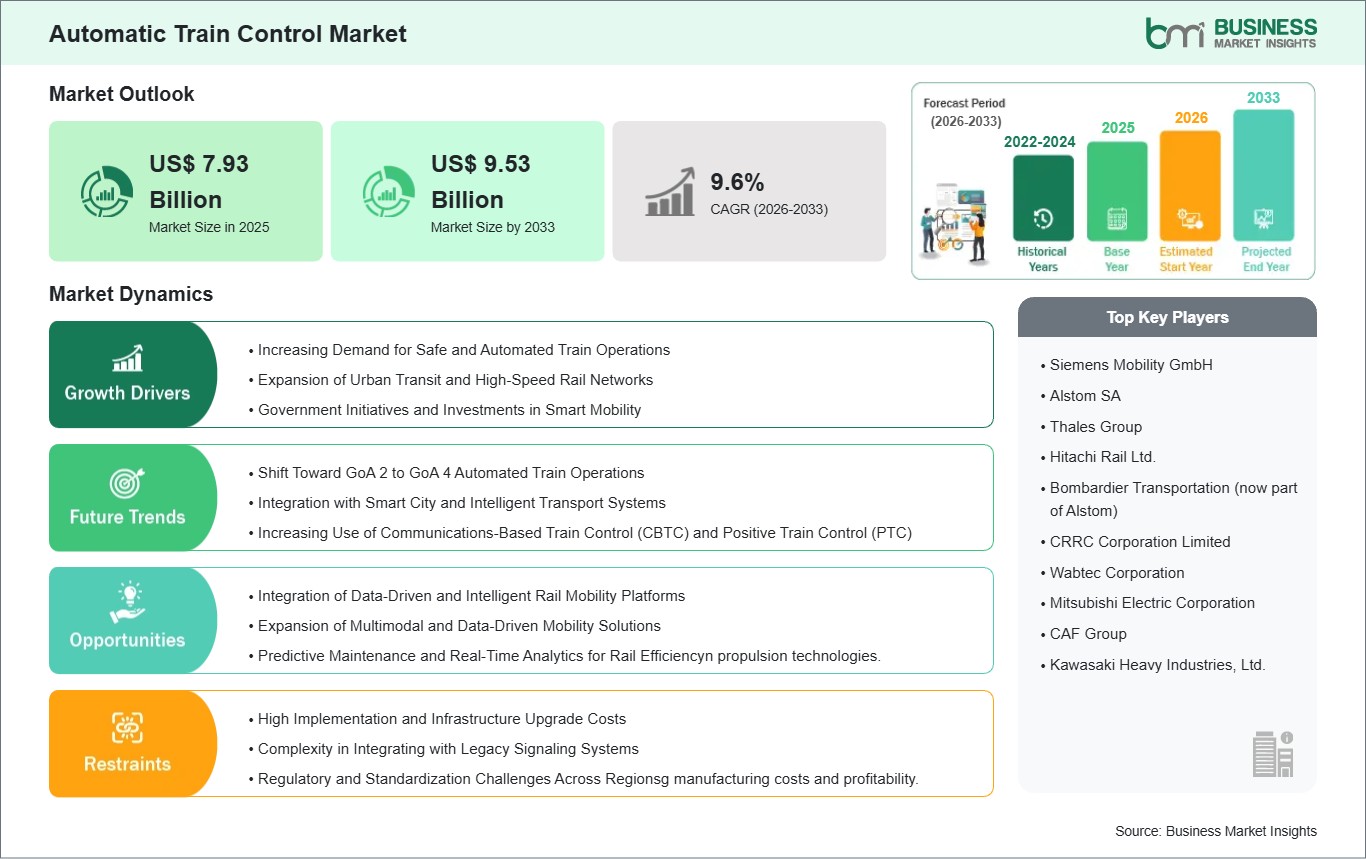

Increasing Demand for Safe and Automated Train Operations

The growing emphasis on safe, efficient, and automated rail operations is a key driver of the Automatic Train Control market. Rail operators and urban transit authorities are under increasing pressure to modernize legacy signaling and train control systems to improve safety, operational efficiency, and on-time performance. ATC systems—including GoA 2 to GoA 4 automation levels, positive train control (PTC), and communications-based train control (CBTC)—enable automatic speed regulation, collision prevention, real-time train monitoring, and predictive maintenance.

Rising passenger volumes, urbanization, and high-density rail networks are driving demand for automated and semi-automated control solutions that minimize human error, reduce operational costs, and increase network throughput. Government regulations and safety mandates in regions such as North America, Europe, and Asia Pacific are accelerating the deployment of ATC technologies. Additionally, advancements in AI, IoT, and cloud-enabled control platforms allow rail operators to monitor performance in real time, enhance decision-making, and optimize fleet utilization, making automated train control an essential component of modern rail systems.

Integration of Data-Driven and Intelligent Rail Mobility Platforms

A major growth opportunity for the Automatic Train Control market lies in the development of integrated, data-driven rail mobility platforms that enhance operational efficiency and passenger experience. Modern ATC systems generate extensive real-time data on train location, speed, signaling status, and network performance, which can be leveraged for predictive maintenance, capacity optimization, and service reliability improvements.

Integration with multimodal transport networks, including metro, bus, commuter rail, and high-speed rail, enables seamless scheduling, improved network coordination, and advanced traffic management. Data-driven ATC platforms also support dynamic train scheduling, automated incident response, and energy-efficient routing, reducing operational costs and environmental impact. Emerging urban rail networks in Asia Pacific and Europe, alongside smart city and sustainable mobility initiatives, provide significant opportunities for ATC vendors to offer interoperable, cloud-connected, and AI-enhanced solutions that optimize rail operations while meeting rising safety and efficiency standards.