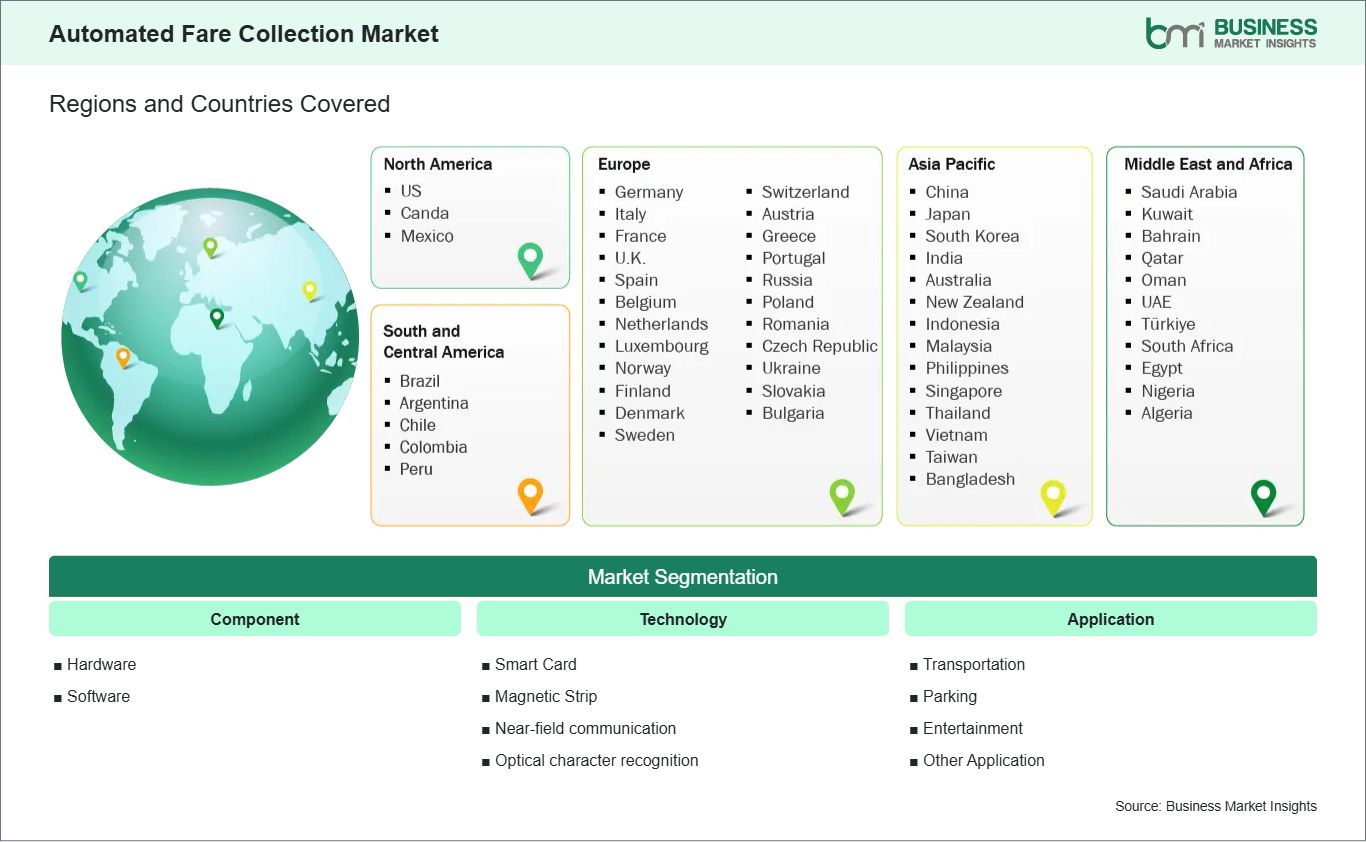

The Automated Fare Collection market is geographically segmented into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. Among these regions, Asia Pacific is projected to witness the strongest growth and maintain a leading market position throughout the forecast period, driven primarily by rapid urbanization, expanding public transit networks, government investments in smart mobility infrastructure, and increasing adoption of contactless and digital payment systems. The region benefits from large-scale transit modernization projects, high smartphone penetration, and favorable policy initiatives promoting cashless economies, smart city programs, and intelligent transportation systems, positioning it as a strategic hub for Automated Fare Collection deployment and innovation.

Within Asia Pacific, key markets include China, India, Japan, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Vietnam, Taiwan, and the Rest of Asia. Growth is propelled by extensive metro, bus, and rail networks, rising commuter volumes, and government initiatives aimed at improving public transport efficiency, reducing congestion, and enhancing passenger experience. Leading economies such as China, India, and Japan are at the forefront of adopting account-based ticketing, mobile payments, and contactless smart card solutions, leveraging real-time transaction monitoring, cloud-based back-office systems, and advanced analytics to optimize revenue management and operational efficiency.

Demand in Asia Pacific is further supported by investments in public transit infrastructure, multimodal mobility integration, and smart city programs, coupled with regulatory support, public-private partnerships, and workforce development in transportation technology and digital payment ecosystems. These factors collectively strengthen the regional Automated Fare Collection ecosystem, ensuring sustained market growth and adoption across both urban and semi-urban transport networks.