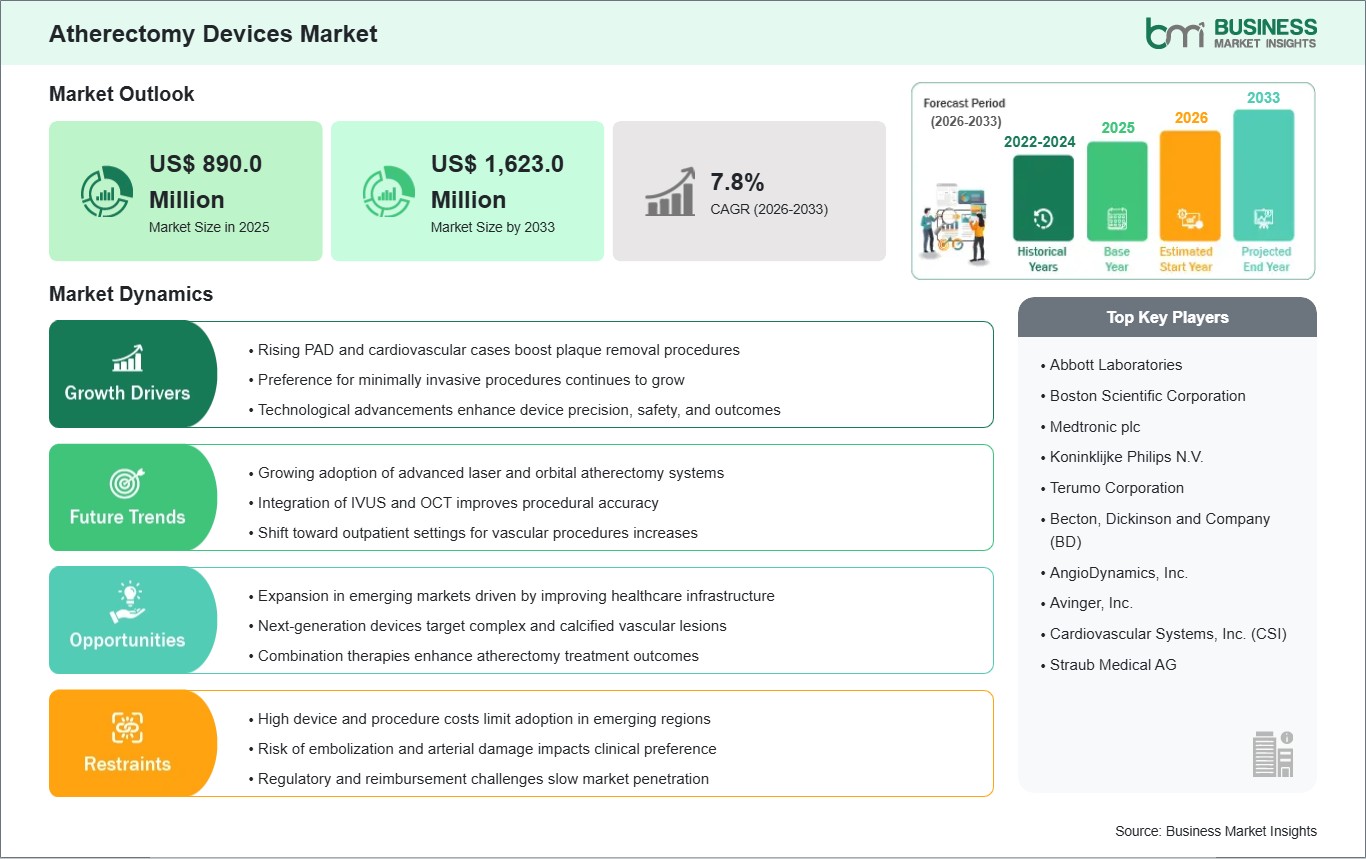

The Atherectomy Devices market size is expected to reach US$ 1,623.0 Million by 2033 from US$ 890.0 Million in 2025. The market is estimated to record a CAGR of 7.8% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Atherectomy devices refer to a specialized category of minimally invasive surgical instruments designed to remove atherosclerotic plaque from the interior walls of blood vessels. Unlike balloon angioplasty, which compresses plaque against the vessel wall, or stenting, which scaffolds the artery open, atherectomy utilizes mechanical or thermal energy to debulk and physically eliminate obstructive material. Market expansion is fundamentally propelled by the rising global prevalence of atherosclerosis, exacerbated by sedentary lifestyles, high rates of diabetes, and a global aging population susceptible to vascular calcification. Furthermore, the shift toward minimally invasive endovascular procedures is accelerating the demand for tools that offer lower procedural trauma and shorter hospital stays compared to traditional open vascular surgery. The expansion of Office-Based Labs (OBLs) and Ambulatory Surgical Centers (ASCs), which prioritize outpatient revascularization, continues to serve as a primary catalyst for sustained demand.

However, several factors may restrain market progression. The high capital and per-procedure costs associated with sophisticated atherectomy systems can be prohibitive for healthcare facilities in emerging or resource-limited regions. Stringent regulatory and clinical trial requirements for Class III medical devices extend the timeline for commercialization and increase development costs. Additionally, the industry faces challenges related to reimbursement volatility, where periodic adjustments to outpatient payment levels can influence the adoption of premium technologies in private vascular practices.

Despite these hurdles, the market holds significant opportunities in the integration of intravascular imaging, such as IVUS or OCT, which allows for real-time visualization of plaque removal. The rise of combination therapies, such as atherectomy followed by drug-coated balloon (DCB) angioplasty, and the expansion of robotic-assisted catheterization are expected to support long-term development within the sector. Manufacturers are also finding growth potential in the development of specialized laser systems that minimize the risk of distal embolization during complex interventions.

Atherectomy Devices Market - Strategic Insights:

Get more information on this report

Atherectomy Devices Market Segmentation Analysis:

Key segments that contributed to the derivation of the Atherectomy Devices market analysis are product, application, and end user.

By Product, the market is segmented into Rotational Atherectomy Systems, Directional Atherectomy Systems, Orbital Atherectomy Systems, Photo-Ablative Atherectomy Systems, and Support Devices.

By Application, the market is divided into Cardiovascular, Peripheral Vascular, and Neurovascular.

By End User, the market is categorized into Hospitals and Ambulatory Surgical Centers.

Atherectomy Devices Market Drivers and Opportunities:

Demographic Vulnerability and Minimally Invasive Vascular Care

The primary driver for the Atherectomy Devices Market is the systemic global rise in the prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD). The Increasing Incidence of Heavily Calcified Lesions acts as a foundational catalyst, as traditional angioplasty often fails to achieve adequate vessel expansion in these complex cases, necessitating mechanical plaque removal. This momentum is further propelled by the Growing Clinical Preference for Leave Nothing Behind Strategies; interventionalists are increasingly utilizing atherectomy to clear blockages without the permanent placement of metallic stents, thereby maintaining future surgical options and reducing foreign-body complications. In the technological sphere, the Integration of Real-Time Intravascular Imaging (IVUS/OCT) serves as a critical driver, allowing physicians to characterize plaque morphology and monitor debulking progress with sub-millimeter precision. Furthermore, the Expansion of Office-Based Labs (OBLs) and Ambulatory Surgical Centers (ASCs) is driving market growth by offering cost-effective, high-volume environments for outpatient vascular interventions. Together, these factors, disease complexity, stent-avoidance trends, and the shift toward outpatient care, ensure a robust and essential growth path for the global Atherectomy Devices Market.

AI-Guided Navigation and the Synergy of Combination Therapies

A significant high-value opportunity lies in the convergence of Atherectomy Platforms with Artificial Intelligence (AI) and Robotic-Assisted Surgery. Next-generation systems are being developed to utilize AI for automated lesion detection and real-time guidance, which reduces procedural variability and enhances safety by alerting clinicians to potential vessel dissections. There is also a major growth frontier in the development of Synergistic One-Device Solutions, where atherectomy is combined with other modalities, such as aspiration for embolic protection or intravascular lithotripsy for deep calcium modification, within a single catheter system. Furthermore, the expansion of Drug-Coated Balloon (DCB) Compatibility presents a lucrative opportunity, as evidence increasingly supports that thorough plaque excision significantly enhances the uptake of antiproliferative drugs into the vessel wall, leading to superior long-term patency. Beyond hardware, the rise of Precision-Designed Micro-Atherectomy for Neurovascular and Small-Vessel Applications offers a unique frontier, targeting previously unreachable blockages in the distal anatomy. Manufacturers who focus on Enhanced Crossing Profiles for Tortuous Anatomy and those pioneering Automated Smart Cutting Mechanisms are positioned to lead the global Atherectomy Devices Market.

Atherectomy Devices Market Size and Share Analysis:

The Atherectomy Devices market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

Based on the product, the Directional Atherectomy Systems subsegment holds the primary market presence, acting as the essential tool for targeted plaque removal in eccentric lesions. These systems are indispensable for the market, maintaining a significant position due to their ability to steer the cutting blade toward the plaque while protecting healthy arterial tissue. Rotational, Orbital, and Photo-Ablative (Laser) systems provide critical support for varied calcification levels. A notable trend is the surge in the Orbital Atherectomy and Laser Atherectomy subsegments, which are registering the highest pace of adoption. These technologies are becoming essential for Calcium Management and In-Stent Restenosis, as the move toward centrifugal sanding and ultraviolet photo-ablation allows for the safe treatment of severely hardened blockages and delicate neurovascular territories that were previously considered inaccessible or high-risk.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Abbott Laboratories

Boston Scientific Corporation

Medtronic plc

Koninklijke Philips N.V.

Terumo Corporation

Becton, Dickinson and Company (BD)

AngioDynamics, Inc.

Avinger, Inc.

Cardiovascular Systems, Inc. (CSI)

Straub Medical AG

Get more information on this report

Atherectomy Devices Market Report Coverage and Deliverables:

The "Atherectomy Devices Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Atherectomy Devices Market Geographic Insights:

The geographical scope of the Atherectomy Devices market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America maintains a dominant market share, supported by a significant disease burden, advanced healthcare infrastructure, and the early adoption of interventional technologies such as AI-guided imaging. Europe represents a mature and technologically advanced market where growth is sustained by an aging population and a strong institutional focus on minimally invasive endovascular procedures. Asia Pacific is identified as the most rapidly advancing region, propelled by accelerating healthcare modernization, expanding clinical facilities, and substantial public investments to address the rising prevalence of cardiovascular mortality in emerging economies.

The Asia-Pacific Atherectomy Devices Market is segmented into China, Japan, South Korea, India, Australia, and the Rest of Asia Pacific. China serves as a central engine for regional expansion, driven by large-scale government programs to modernize vascular care and a growing demand for plaque-modification devices. India is witnessing a notable transition as private healthcare providers expand their interventional portfolios to address the high occurrence of peripheral and coronary artery diseases among the middle-class demographic. Japan continues to prioritize high-specification instrumentation, focusing on the integration of robotic catheter systems and advanced rotational atherectomy for its substantial geriatric population.

Get more information on this report

Atherectomy Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the Atherectomy Devices market across product, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by product, application, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Atherectomy Devices Market News and Key Development:

The Atherectomy Devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Atherectomy Devices market are:

In October 2025, BD launched the XTRACT™ Registry for the Rotarex™ Catheter System, enrolling the first patient in the U.S. The multi-center, post-market registry is designed to collect real-world evidence on the performance of BD`s atherectomy and thrombectomy device for peripheral artery disease (PAD). This initiative strengthens clinical validation, supports broader adoption, and highlights BD`s commitment to advancing evidence-based PAD care, positively impacting the atherectomy devices market.

In November 2024, Philips launched the U.S. THOR IDE clinical trial for its innovative combined laser atherectomy and intravascular lithotripsy catheter. The first patient was successfully treated at the Cardiovascular Institute of the South, marking a milestone in peripheral artery disease (PAD) management. This first-of-its-kind device integrates two critical PAD treatments into a single procedure, simplifying workflows, reducing procedural complexity, and potentially improving patient outcomes. The launch underscores Philips’ in-house innovation capabilities and strengthens the pipeline of advanced atherectomy solutions, positively impacting market growth.

Key Sources Referred:

World Bank & Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Atherectomy Devices Market

Abbott Laboratories

Boston Scientific Corporation

Medtronic plc

Koninklijke Philips N.V.

Terumo Corporation

Becton, Dickinson and Company (BD)

AngioDynamics, Inc.

Avinger, Inc.

Cardiovascular Systems, Inc. (CSI)

Straub Medical AG

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Atherectomy Devices Market?

The Atherectomy Devices Market is valued at US$ 890.0 Million in 2025, it is projected to reach US$ 1,623.0 Million by 2033.

What is the CAGR for Atherectomy Devices Market by (2026 - 2033)?

As per our report Atherectomy Devices Market, the market size is valued at US$ 890.0 Million in 2025, projecting it to reach US$ 1,623.0 Million by 2033. This translates to a CAGR of approximately 7.8% during the forecast period.

What segments are covered in this report?

The Atherectomy Devices Market report typically cover these key segments-

Product (Rotational Atherectomy Systems, Directional Atherectomy Systems, Orbital Atherectomy Systems, Photo-Ablative Atherectomy Systems, and Support Devices)

Application (Cardiovascular, Peripheral Vascular, and Neurovascular)

End User (Hospitals and Ambulatory Surgical Centers)

What is the historic period, base year, and forecast period taken for Atherectomy Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Atherectomy Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Atherectomy Devices Market?

The Atherectomy Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Abbott Laboratories

Boston Scientific Corporation

Medtronic plc

Koninklijke Philips N.V.

Terumo Corporation

Becton, Dickinson and Company (BD)

AngioDynamics, Inc.

Avinger, Inc.

Cardiovascular Systems, Inc. (CSI)

Straub Medical AG

Who should buy this report?

The Atherectomy Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Atherectomy Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Atherectomy Devices Market

Get Free Sample For Atherectomy Devices Market