analysis - by Component [Solution and Services (Professional Services and Managed Services)], Type (FDD and TDD), and End User (Manufacturing, Energy & Utilities, Healthcare, Transportation, Mining, and Others)

No. of Pages:105

Report Code:

TIPRE00022796

Category:

Technology, Media and Telecommunications

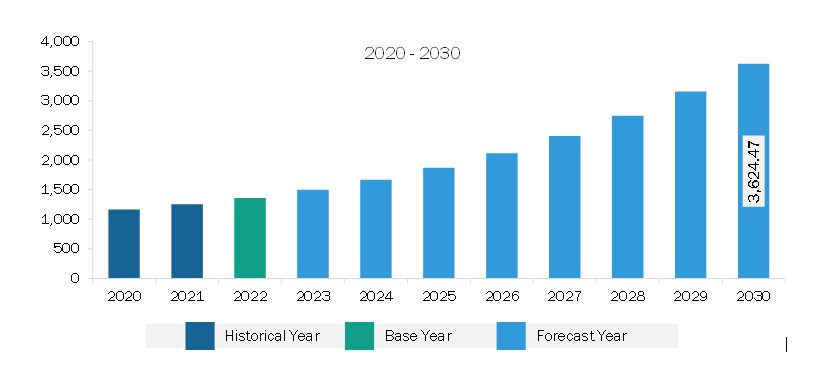

The Asia Pacific private LTE market was valued at US$ 1,357.90 million in 2022 and is expected to reach US$ 3,624.47 million by 2030; it is estimated to grow at a CAGR of 13.1% from 2022 to 2030.

Demand for Ultra-Reliable, Low Latency Communication Boosts Asia Pacific Private LTE Market.

The demand for greater bandwidth grows as people interact in high-definition video and receive increasingly immersive experiences with virtual reality and cloud gaming. Machines, too, rely on high-speed, low-latency networking, especially as industrial processes become more automated.

Private LTE is being built to enable services for latency-sensitive devices in applications such as autonomous driving, factory automation, remote surgery, mission-critical communications, and VR/AR entertainment. These applications require sub-millisecond latency and error rates of fewer than one packet per 105. Ultra-reliable low-latency communications (URLLC) application cases have stringent latency and reliability requirements.

Cellular networks encounter challenges due to channel fading, interference levels, and user equipment (UE) movement. Private LTE technology enables high reliability, low latency, and optimal multiplexing of URLLC and other traffic in the system. Throughout the projection period, remote LTE deployment must be planned to meet high latency and reliability standards for URLLC, i.e., be suitable for the private LTE market.

Asia Pacific Private LTE Market Overview

Asia Pacific is constantly witnessing a growing economy, leading to growth in various sectors, including manufacturing, infrastructure, and technology. Many of the region's economies are focusing on autonomous vehicles, smart cities, and IoT to empower their economy further. The investors avoid high-tech costs investment in the US. They are diverting toward APAC to invest in significant business opportunities, which include growth of LTE technology with the acceleration in the adoption of digital transformation across various countries in the region. The Asia Pacific private LTE market is segmented into South Korea, India, China, Japan, Australia, and the Rest of Asia Pacific.

The massive populations of China and India, the increasing middle-class population in these countries, and the growing telecom sector in both countries are projected to grow due to the deployment of LTE. The advancement in mobile technology and connected infrastructure across China, Japan, and South Korea will further boost the demand for private LTE. Moreover, the growing smartphone penetration in Asia Pacific is a significant factor driving the private LTE market across the region. The development of LTE networks and the accessibility of low-cost Android smartphones boost the demand for private LTE networks to engage more users. Furthermore, China is the largest producer of passenger cars globally; India, Japan, and South Korea are some of the primary vehicle manufacturing countries. The region is the third-largest pharmaceutical producer after North America and Europe. The supportive Government and favorable initiatives in many Asian countries, such as the price reform in Japan and China, the Food and Drug Administration's reform in China, supportive funding in Southeast Asia, and growing digitalization in the pharmaceutical industry are the major factors driving the private LTE market in the region.

Asia Pacific Private LTE Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Private LTE Market Segmentation

The Asia Pacific private LTE market is segmented based on component, type end user, and country. Based on component, the Asia Pacific private LTE market is segmented into solution andservices. The services is further bifurcated into professional and managed services.

The solution segment held a larger market share in 2022.

Based on type, the Asia Pacific private LTE market is bifurcated into FDD and TDD. The FDD held a larger market share in 2022.

Based on end user, the Asia Pacific private LTE market is segmented into manufacturing,energy & utilities,healthcare,transportation,mining, and others. The manufacturing held the largest market share in 2022.

Based on country, the Asia Pacific private LTE market is segmented into China, Japan, South Korea, India, Australia, and the Rest of Asia Pacific. China dominated the Asia Pacific private LTE market share in 2022.

Cisco Systems Inc, Telefonaktiebolaget LM Ericsson, Huawei Investment & Holding Co Ltd, Samsung Group, Verizon Communications Inc, Star Solutions, Sierra Wireless Inc, and Kyndryl Holdings Inc are some of the leading companies operating in the Asia Pacific private LTE market.

Asia Pacific Private LTE Market Strategic Insights

Get more information on this report

Asia Pacific Private LTE Market Segmentation Analysis

Asia Pacific Private LTE Market Report Highlights

Asia Pacific Private LTE Report Scope

Report Attribute

Details

Market size in 2022

US$ 1,357.90 Million

Market Size by 2030

US$ 3,624.47 Million

CAGR (2022 - 2030)

13.1%

Historical Data

2020-2021

Forecast period

2023-2030

Segments Covered

By Component

Solution and Services

By Type

FDD and TDD

By End User

Manufacturing

Energy & Utilities

Healthcare

Transportation

Mining

Regions and Countries Covered

Asia-Pacific

China, India, Japan, Australia, Rest of Asia-Pacific

Market leaders and key company profiles

Cisco Systems Inc.

Telefonaktiebolaget LM Ericsson.

Huawei Investment & Holding Co Ltd.

Samsung Group.

Verizon Communications Inc.

Star Solutions.

Sierra Wireless, Inc.

Kyndryl Holdings Inc.

Get more information on this report

Asia Pacific Private LTE Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Asia Pacific Private LTE Market

Cisco Systems Inc.Telefonaktiebolaget LM Ericsson.Huawei Investment & Holding Co Ltd.Samsung Group.Verizon Communications Inc.Star Solutions.Sierra Wireless, Inc.Kyndryl Holdings Inc.

Frequently Asked Questions

How big is the Asia Pacific Private LTE Market?

The Asia Pacific Private LTE Market is valued at US$ 1,357.90 Million in 2022, it is projected to reach US$ 3,624.47 Million by 2030.

What is the CAGR for Asia Pacific Private LTE Market by (2022 - 2030)?

As per our report Asia Pacific Private LTE Market, the market size is valued at US$ 1,357.90 Million in 2022, projecting it to reach US$ 3,624.47 Million by 2030. This translates to a CAGR of approximately 13.1% during the forecast period.

What segments are covered in this report?

The Asia Pacific Private LTE Market report typically cover these key segments-

Component (Solution and Services)

Type (FDD and TDD)

End User (Manufacturing, Energy & Utilities, Healthcare, Transportation, Mining)

What is the historic period, base year, and forecast period taken for Asia Pacific Private LTE Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Private LTE Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2030

Who are the major players in Asia Pacific Private LTE Market?

The Asia Pacific Private LTE Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Cisco Systems Inc.

Telefonaktiebolaget LM Ericsson.

Huawei Investment & Holding Co Ltd.

Samsung Group.

Verizon Communications Inc.

Star Solutions.

Sierra Wireless, Inc.

Kyndryl Holdings Inc.

Who should buy this report?

The Asia Pacific Private LTE Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Asia Pacific Private LTE Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Asia Pacific Private LTE Market

Get Free Sample For Asia Pacific Private LTE Market