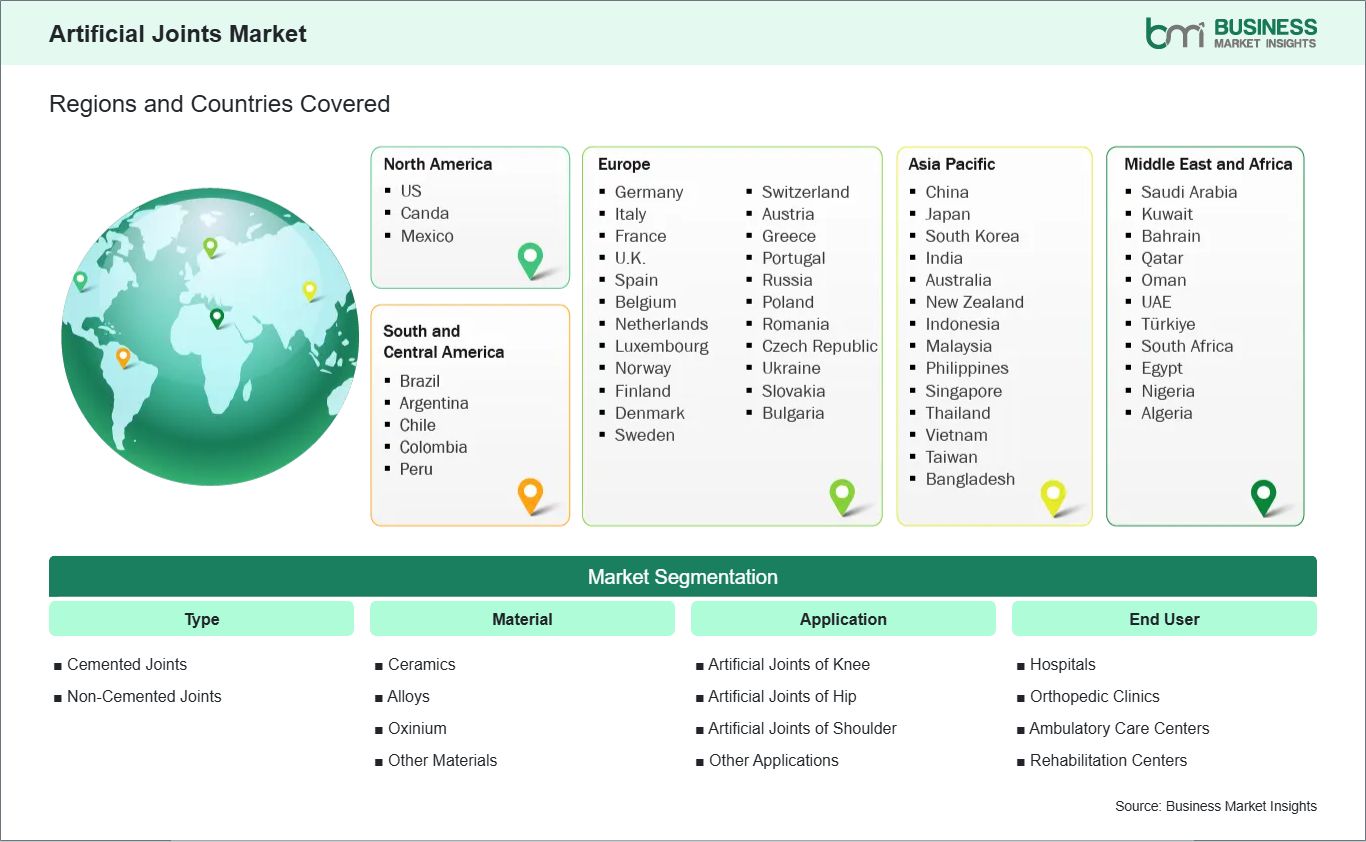

The geographical scope of the artificial joints market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The artificial joints market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific artificial joints market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia-Pacific artificial joints market is experiencing robust growth, due to the rising population of older people in the area, together with the increasing occurrence of joint ailments like osteoarthritis and degenerative conditions; for instance, the countries in Asia are experiencing a remarkable increase in the number of old people, which, in turn, creates a bigger demand for joint replacement operations. Besides, better medical infrastructure and easier access to surgery, which were first made possible through government investment in hospitals, training of orthopedic specialists, and improved reimbursement support, have now allowed more patients to go for advanced orthopedic treatments that they could not afford before.

The enhancement of economic conditions and the rise of a middle class in the key markets of China, India, and Southeast Asia are leading to an increase in disposable incomes and health insurance coverage, thus permitting more people to have elective joint surgeries. The tech progress, such as robotic surgery, 3D printing, and minimally invasive procedures, is also bringing the clinical use closer; all these innovations are making the whole process more precise, recovery quicker, and results better, hence patient acceptance is rising. Moreover, the international patients who are looking for affordable yet quality joint replacement services are the ones that are boosting the market in countries such as Thailand, India, and Singapore, which are known for their medical tourism.