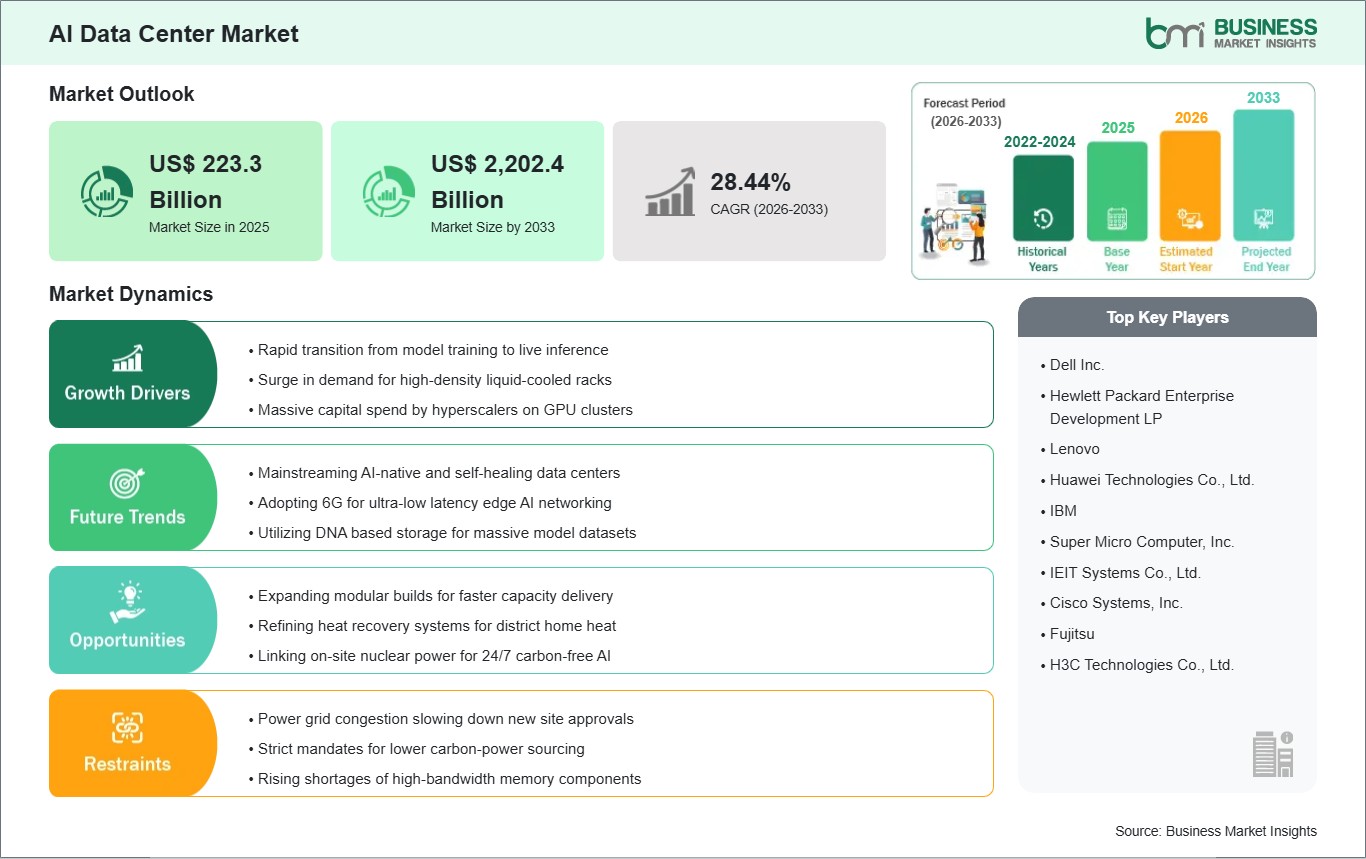

The AI Data Center Market size is expected to reach US$ 2,202.4 Billion by 2033 from US$ 223.3 Billion in 2025. The market is estimated to record a CAGR of 33.12% from 2026 to 2033.

Executive Summary and Global Market Analysis:

AI data centers are specialized computing facilities designed to meet the substantial computational and thermal requirements of artificial intelligence workloads, including large language model (LLM) training and high-speed inference. These centers serve as the core infrastructure of the global intelligence economy, encompassing hyperscale facilities, GPU-as-a-Service (GPUaaS) clouds, and liquid-cooled colocation centers. These technologies support the training of large neural networks, enable low-latency inference for real-time applications such as autonomous driving, and provide the high-density power delivery needed for generative AI. Market growth is driven by the rapid expansion of generative AI, significant infrastructure investments by technology hyperscalers, and the transition from experimental AI pilots to enterprise-scale production. Additionally, AI-driven Data Center Infrastructure Management (DCIM) uses machine learning to optimize power usage effectiveness (PUE) and predictive maintenance, improving operational efficiency.

However, several challenges can restrain market growth: high initial procurement and integration costs, particularly for advanced liquid cooling retrofits and high-density power distribution, can limit the expansion of smaller colocation providers and enterprise facilities. Stringent regulatory hurdles and evolving environmental standards regarding water usage and carbon emissions from massive energy consumption lengthen the time-to-market for new "mega-campuses" and increase development overhead. Additionally, the industry faces constraints due to technical complexity and a critical shortage of specialized engineering talent, where the lack of expertise in managing 100kW+ rack densities and complex AI-silicon clusters can result in the sub-optimal use of these high-performance environments.

Despite these hurdles, the market holds immense opportunities in the universal mandate for sustainable and power-independent infrastructure and the accelerating deployment of behind-the-meter energy solutions like small modular reactors (SMRs). The expansion of 5G-enabled edge AI data centers, which allow for instantaneous inference processing for autonomous robotics, and the development of sovereign AI clouds to ensure national data security are expected to create significant opportunities for market growth.

AI Data Center Market - Strategic Insights:

Get more information on this report

AI Data Center Market Segmentation Analysis:

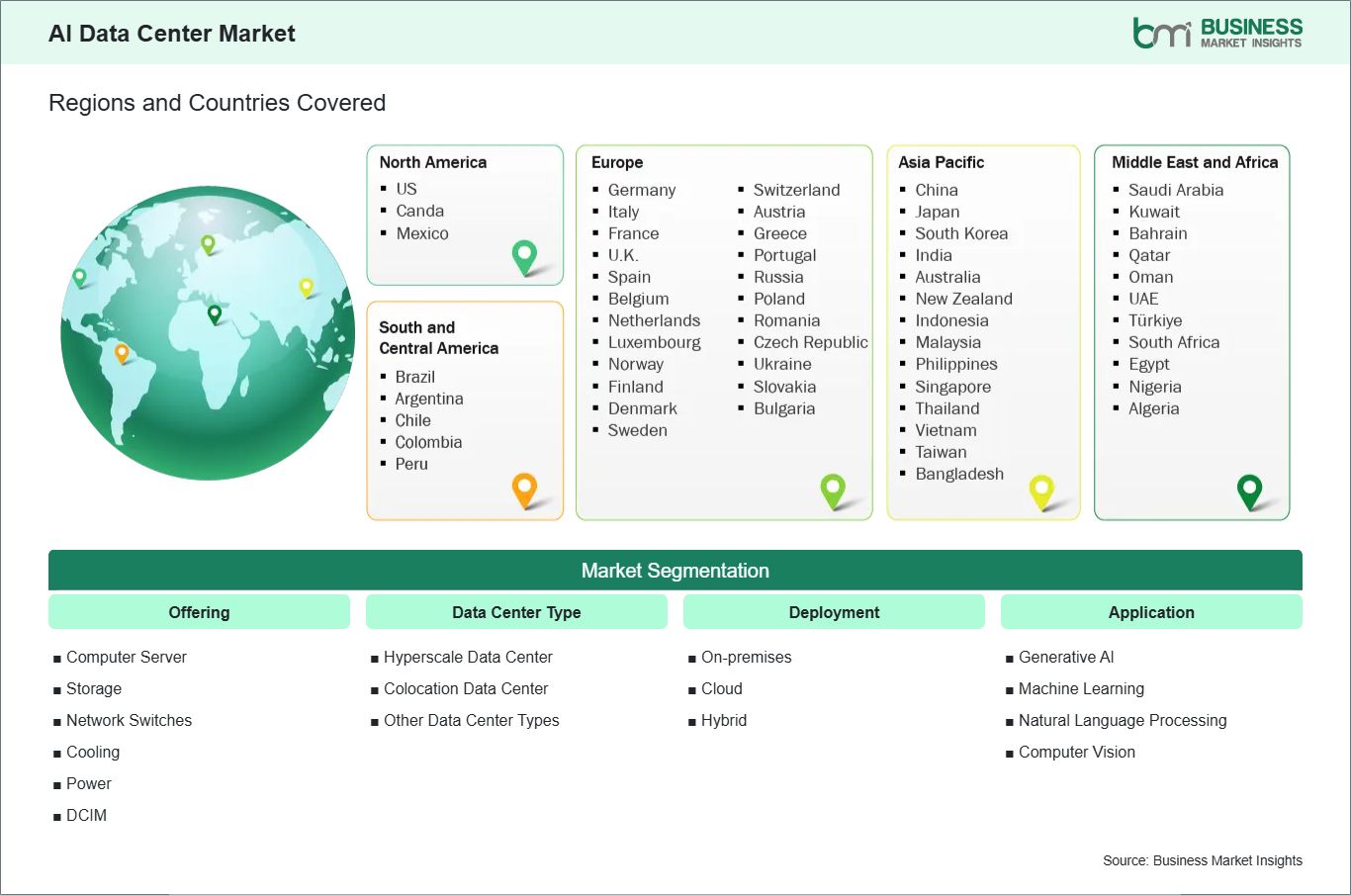

Key segments that contributed to the derivation of the AI Data Center market analysis are offering, data center type, deployment, application, and end user.

By Offering, the market is segmented into Computer Server, Storage, Network Switches, Cooling, Power, and DCIM.

By Data Center Type, the market is divided into Hyperscale Data Center, Colocation Data Center, and Others.

By Deployment, the market is categorized into On-premises, Cloud, and Hybrid.

By Application, the market is segmented into Generative AI, Machine Learning, Natural Language Processing, and Computer Vision.

By End User, the market is divided into Cloud Service Providers, Enterprises, and Government Organizations.

AI Data Center Market Drivers and Opportunities:

Scaling Generative AI Is Reshaping Data Center Power Systems

The primary driver for the AI Data Center Market is the massive transition of generative AI from experimental pilots to full-scale industrial production. As enterprises integrate large language models (LLMs) and agentic AI into their core workflows, the demand for high-density compute power has shifted from a specialized requirement to a foundational necessity. This "AI arms race" among hyperscalers and sovereign nations has forced a fundamental rethink of power infrastructure; by 2026, electricity availability will have become the defining constraint of the market.

Data centers are evolving from passive energy consumers into active grid stakeholders, investing in on-site power generation, such as natural gas turbines, small modular reactors (SMRs), and massive battery storage, to bypass grid congestion and ensure uptime. This relentless pursuit of compute capacity, backed by over a trillion dollars in planned ecosystem investment through the end of the decade, ensures a robust and high-velocity growth path as AI workloads move increasingly from model training to real-time inference.

Liquid Cooling Adoption and Edge AI Inference Growth

A significant high-value opportunity lies in the rapid adoption of advanced liquid cooling and thermal management systems. As next-generation GPUs and AI accelerators reach thermal design powers (TDP) that exceed the physical limits of traditional air cooling, technologies like direct-to-chip (DTC) and immersion cooling have moved from "niche" to "standard" for new builds. This transition not only enables higher rack densities but also offers a lucrative path for heat-reuse initiatives, where waste heat is redirected to local district heating or industrial processes.

Another major growth frontier is the expansion of Edge AI and Modular Data Centers. To reduce latency and data backhaul costs, AI inference is increasingly being offloaded from centralized hubs to localized nodes in factories, hospitals, and urban centers. This shift creates a massive market for prefabricated, "plug-and-play" modular units that can be deployed in months rather than years. Manufacturers who focus on AI-ready electrical architectures and "sovereign cloud" solutions, allowing nations to process sensitive data locally, are positioned to lead a market that is increasingly defined by speed, efficiency, and regional autonomy.

AI Data Center Market Size and Share Analysis:

The AI Data Center market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within offering, data center type, deployment, application, and end user, offering insights into their contribution to overall market performance.

For instance, the Computer Server subsegment holds a significant market share, driven by the insatiable demand for high-performance GPUs and specialized AI accelerators. These servers are indispensable for the Generative AI and Machine Learning subsegment of the application segment, where massive parallel processing is required to train models with trillions of parameters. A notable trend in 2026 is the rapid transition from air cooling to Liquid Cooling solutions, such as direct-to-chip and immersion cooling, which have become a technical necessity for racks exceeding 40 kW. These innovations are particularly vital in Hyperscale Data Centers, where they empower cloud providers to maintain hardware reliability while achieving Power Usage Effectiveness (PUE) ratings as low as 1.15.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Dell Inc.\r\n

Hewlett Packard Enterprise Development LP\r\n

Lenovo\r\n

Huawei Technologies Co., Ltd.\r\n

IBM\r\n

Super Micro Computer, Inc.\r\n

IEIT Systems Co., Ltd.\r\n

Cisco Systems, Inc.\r\n

Fujitsu\r\n

H3C Technologies Co., Ltd.

Get more information on this report

AI Data Center Market Report Coverage and Deliverables:

The "AI Data Center Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

AI Data Center market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

AI Data Center market trends, as well as market dynamics such as drivers, restraints, and key opportunities

AI Data Center market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the AI Data Center market

Detailed company profiles, including SWOT analysis

AI Data Center Market Geographic Insights:

The geographical scope of the AI Data Center market report is divided into five regions: North America, Asia Pacific, Europe, Middle East &Africa, and South &Central America.

The Asia-Pacific AI Data Center Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily driven by the region's aggressive push into Generative AI and the rollout of 5G networks, which necessitate low-latency processing at the edge. China and Japan are leading the transition toward high-performance computing (HPC) facilities, while India and Southeast Asian hubs such as Malaysia are witnessing a surge in "mega-campus" developments. These projects are increasingly focused on overcoming grid constraints through localized power solutions and advanced liquid cooling technologies.

Get more information on this report

AI Data Center Market Research Report Guidance:

The report includes qualitative and quantitative data in the AI Data Center market across offering, data center type, deployment, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the AI Data Center market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the AI Data Center market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the AI Data Center market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover AI Data Center market segments by offering, data center type, deployment, application, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the AI Data Center market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

AI Data Center Market News and Key Development:

The AI Data Center market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the AI Data Center market are:

In January 2026, LightHouse Data Centers and Wharton Digital announced the launch of a fully integrated platform to develop, own, and operate hyperscale data centers across North America. The partnership combines LightHouse's deep hyperscale development, leasing, and operational expertise with Wharton's institutional capital and four decades of real estate experience. Together, the platform is positioned to deliver in excess of 2 gigawatts (GW) of capacity to solve accelerating demand from hyperscale, AI, and cloud customers amid industry-wide supply constraints.

In June 2025, Amazon announced plans to invest a new total of AU$20 billion from 2025 to 2029 to expand, operate, and maintain its data center infrastructure in Australia. The country's largest publicly-announced global technology investment will support the strong growth in customer demand for cloud computing and artificial intelligence (AI), accelerating AI adoption and capability, and the continued modernization of Australian organizations of all sizes.

Key Sources Referred:

Institute of Electrical and Electronics Engineers (IEEE)International Energy Agency (IEA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - AI Data Center Market

Dell Inc.

Hewlett Packard Enterprise Development LP

Lenovo

Huawei Technologies Co., Ltd.

IBM

Super Micro Computer, Inc.

IEIT Systems Co., Ltd.

Cisco Systems, Inc.

Fujitsu

H3C Technologies Co., Ltd.

Frequently Asked Questions

How big is the AI Data Center Market?

The AI Data Center Market is valued at US$ 223.3 Billion in 2025, it is projected to reach US$ 2,202.4 Billion by 2033.

What is the CAGR for AI Data Center Market by (2026 - 2033)?

As per our report AI Data Center Market, the market size is valued at US$ 223.3 Billion in 2025, projecting it to reach US$ 2,202.4 Billion by 2033. This translates to a CAGR of approximately 33.12% during the forecast period.

What segments are covered in this report?

The AI Data Center Market report typically cover these key segments-

Offering (Computer Server, Storage, Network Switches, Cooling, Power, and DCIM)

Data Center Type (Hyperscale Data Center, Colocation Data Center, and Other Data Center Types)

Deployment (On-premises, Cloud, and Hybrid)

Application (Generative AI, Machine Learning, Natural Language Processing, and Computer Vision)

What is the historic period, base year, and forecast period taken for AI Data Center Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the AI Data Center Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in AI Data Center Market?

The AI Data Center Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Dell Inc.\r\n

Hewlett Packard Enterprise Development LP\r\n

Lenovo\r\n

Huawei Technologies Co., Ltd.\r\n

IBM\r\n

Super Micro Computer, Inc.\r\n

IEIT Systems Co., Ltd.\r\n

Cisco Systems, Inc.\r\n

Fujitsu\r\n

H3C Technologies Co., Ltd.

Who should buy this report?

The AI Data Center Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the AI Data Center Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For AI Data Center Market

Get Free Sample For AI Data Center Market