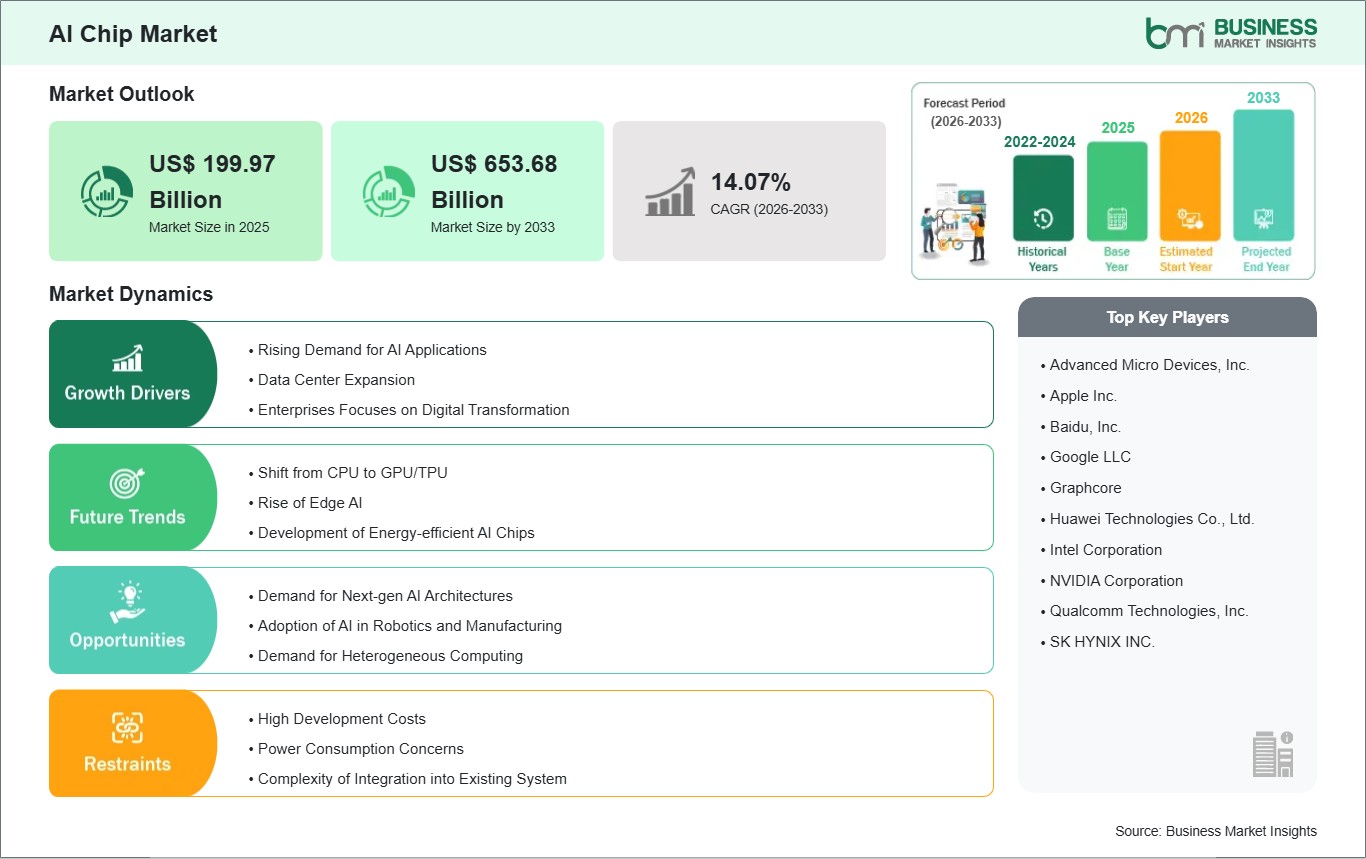

The AI Chip Market size is expected to reach US$ 653.68 Billion by 2033 from US$ 199.97 Billion in 2025. The market is estimated to record a CAGR of 15.96% from 2026 to 2033.

Executive Summary and Global Market Analysis:

An AI chip is a specialized type of microprocessor designed to accelerate artificial intelligence tasks by efficiently handling complex mathematical computations required for machine learning, deep learning, and neural network operations. Unlike traditional CPUs, AI chips such as GPUs, TPUs, and neural processing units are optimized for parallel processing, enabling faster and more energy-efficient performance for AI workloads. The benefits of AI chips include significant improvements in speed and accuracy for data-intensive tasks, reduced power consumption, and enhanced real-time decision-making capabilities, which are critical for applications ranging from autonomous vehicles to personalized healthcare. Usage of AI chips spans multiple industries including tech, automotive, healthcare, finance, and manufacturing, where they power intelligent systems like recommendation engines, predictive analytics, robotics, and natural language processing tools.

Demand factors in the AI chip market are influenced by key drivers such as rapid AI adoption, growth in data generation, and increased investment in cloud computing infrastructure. However, restraints include high development costs, design complexity, and supply chain challenges that can slow market penetration. Opportunities arise from expanding edge AI applications, rising demand for smart devices, and innovation in low-power chip architectures. Current trends focus on heterogeneous computing, custom ASIC development, and integration of AI accelerators in consumer electronics to meet evolving performance and efficiency needs.

AI Chip Market - Strategic Insights:

Get more information on this report

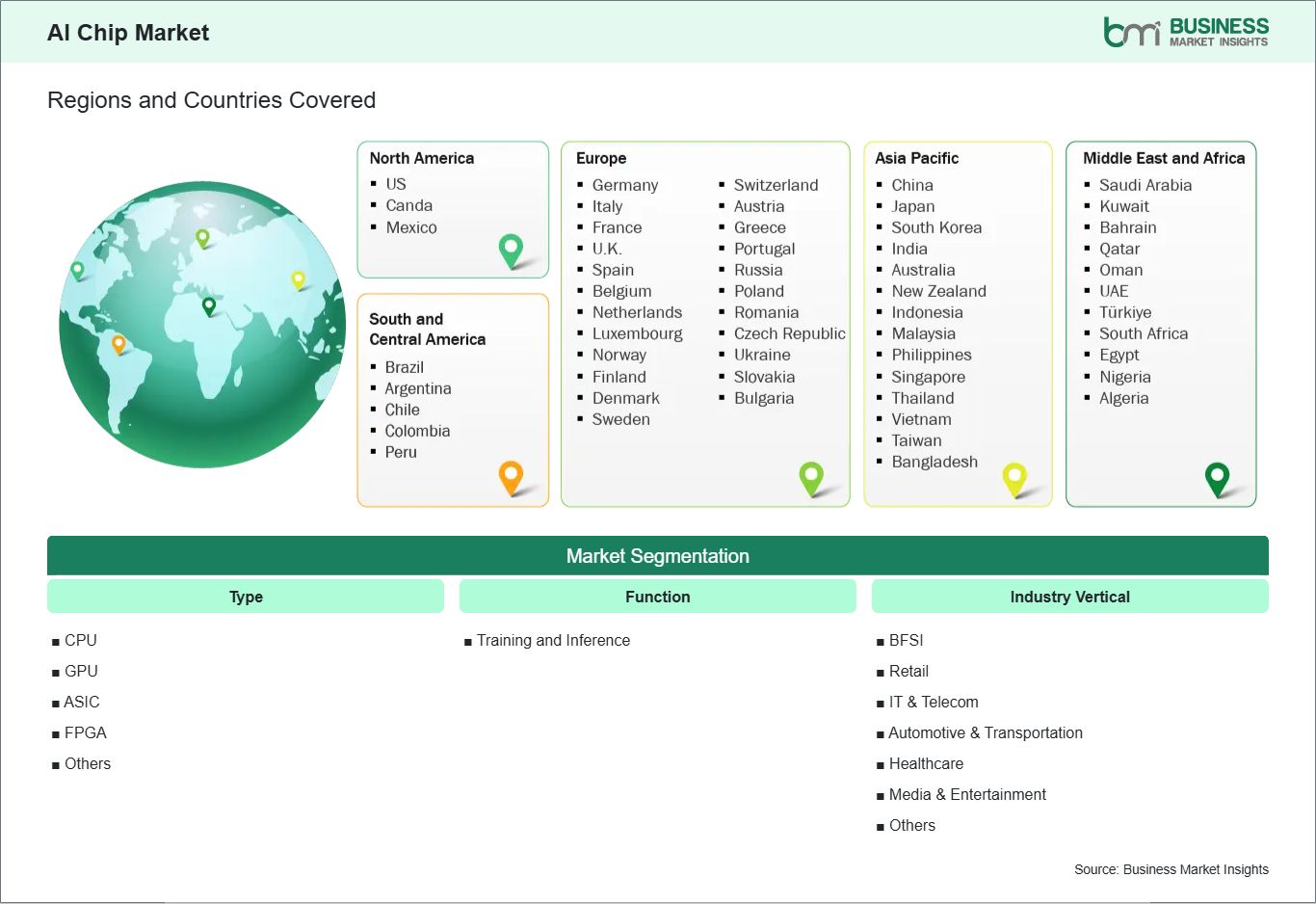

AI Chip Market Segmentation Analysis:

Key segments that contributed to the derivation of the AI chip market analysis are type, function, and industry vertical.

By type, the market is segmented into CPU, GPU, ASIC, FPGA, and others. The GPU segment held the largest share of the market in 2025.

By function, the market is divided into training and inference. The inference segment held the largest share of the market in 2025.

By industry vertical the market is segmented into BFSI, consumer electronics, retail, IT & telecom, automotive & transportation, healthcare, media & entertainment, and others. The consumer electronics segment held the largest share of the market in 2025.

AI Chip Market Drivers and Opportunities:

Rising Demand for AI Applications

The factor of rising demand for AI applications is a primary driver of growth in the AI chip market, as it directly influences the need for more powerful and efficient processing hardware. Artificial intelligence is increasingly integrated across diverse sectors, including healthcare, automotive, finance, retail, and telecommunications, creating a surge in computational requirements. In healthcare, AI-powered diagnostic tools, predictive analytics, and personalized medicine rely heavily on rapid data processing and complex algorithms, which in turn fuels the demand for high-performance AI chips. Similarly, the automotive industry’s shift toward autonomous vehicles and advanced driver-assistance systems (ADAS) depends on real-time data processing capabilities, further emphasizing the need for specialized AI hardware. Moreover, the proliferation of AI in consumer electronics, such as smart speakers, home automation devices, and smartphones, is also driving demand, as these devices require efficient, low-power AI chips to perform tasks like natural language processing and computer vision. Enterprises and cloud service providers are increasingly deploying AI workloads in data centers, necessitating chips that can handle large-scale machine learning and deep learning tasks efficiently, while minimizing latency and energy consumption.

Additionally, the evolution of AI models, particularly generative AI and large language models, demands chips with higher memory bandwidth and parallel processing capabilities, reinforcing market growth. The rising adoption of AI in industrial automation, predictive maintenance, and robotics further amplifies this trend, as these applications require edge AI chips capable of performing high-speed computations in real-world environments. Overall, as organizations across sectors continue to embrace AI to enhance efficiency, optimize decision-making, and develop innovative products and services, the demand for AI chips escalates, creating a positive feedback loop that propels market expansion, drives technological innovation, and intensifies competition among chip manufacturers to deliver faster, more efficient, and specialized AI solutions.

Demand for Next-gen AI Architectures

Emergence of next-generation AI architectures, which are fundamentally transforming the way artificial intelligence workloads are processed. Traditional AI models, while powerful, often face limitations in efficiency, scalability, and energy consumption, especially as applications become more complex and data-intensive. Next-gen AI architectures, such as transformer-based models, neuromorphic computing, and advanced parallel processing designs, address these challenges by enabling faster computations, higher throughput, and more efficient memory utilization. These architectures allow AI chips to handle increasingly sophisticated tasks, from natural language processing and computer vision to autonomous systems and real-time analytics, without excessive energy consumption or latency. Furthermore, these architectures are designed to optimize for both training and inference, catering to the growing demand for on-device AI in smartphones, edge devices, and IoT ecosystems. The adaptability of next-gen AI architectures also opens opportunities for AI chip manufacturers to create specialized accelerators tailored to specific workloads, enhancing performance and creating differentiation in a competitive market.

Additionally, as AI models continue to grow in size and complexity, there is a rising need for chips that can support high-bandwidth memory, advanced interconnects, and multi-chip scaling, all of which are facilitated by these new architectures. This technological evolution not only drives demand from cloud service providers and enterprise AI platforms but also fuels innovation in industries such as healthcare, automotive, finance, and manufacturing, where AI is increasingly embedded into critical operations. Consequently, next-gen AI architectures serve as a key enabler of market expansion, positioning AI chips as indispensable components for future AI innovation and unlocking significant growth opportunities for companies investing in cutting-edge semiconductor technologies.

AI Chip Market Size and Share Analysis:

By type, the market is segmented into CPU, GPU, ASIC, FPGA, and others. The GPU segment held the largest share of the market in 2025. The demand for GPUs in the AI chip market is rising due to increasing adoption of artificial intelligence across industries, growth in deep learning and data-intensive applications, expansion of cloud computing, and rising investment in AI research. Additionally, advancements in autonomous systems, gaming, and high-performance computing further drive GPU requirements.

By function, the market is divided into training and inference. The inference segment held the largest share of the market in 2025, owing to the rising demand for real-time applications, including autonomous vehicles, voice assistants, and recommendation systems. Factors such as energy-efficient architectures, low-latency processing, growing AI adoption across industries, and advances in neural network optimization significantly propel the need for specialized inference-focused chips.

By industry vertical, the market is segmented into BFSI, consumer electronics, retail, IT & telecom, automotive & transportation, healthcare, media & entertainment, and others. The consumer electronics segment held the largest share of the market in 2025. Increasing demand for faster processing, enhanced device intelligence, and energy efficiency motivates manufacturers. Advancements in machine learning, lower production costs, and growing consumer interest in smart devices further accelerate integration. Strong ecosystem support and software compatibility also boost adoption.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Advanced Micro Devices, Inc.

Apple Inc.

Baidu, Inc.

Google LLC

Graphcore

Huawei Technologies Co., Ltd.

Intel Corporation

NVIDIA Corporation

Qualcomm Technologies, Inc.

SK HYNIX INC.

Get more information on this report

AI Chip Market Report Coverage and Deliverables:

The "AI Chip Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

AI chip market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

AI chip market trends, as well as market dynamics such as drivers, restraints, and key opportunities

AI chip market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the AI chip market

Detailed company profiles, including SWOT analysis

AI Chip Market Geographic Insights:

The geographical scope of the AI chip market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The AI chip market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific AI chip market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The demand factor driving the growth of the AI chip market in the Asia Pacific region is driven by a combination of technological, economic, and policy factors that collectively create a conducive environment for innovation and implementation. First and foremost, the rapid growth of data-intensive industries, such as e-commerce, fintech, healthcare, and smart manufacturing, is fueling the demand for high-performance AI chips capable of processing massive datasets efficiently. The proliferation of edge computing and IoT devices further necessitates the deployment of specialized AI hardware to ensure low-latency and energy-efficient operations. Additionally, government initiatives across the region play a pivotal role in accelerating AI chip adoption. Countries like China, Japan, South Korea, and Singapore have implemented strategic AI development plans, offering subsidies, tax incentives, and research grants to domestic semiconductor manufacturers, thereby stimulating investment in AI chip design and production. Economic factors also contribute significantly, as the Asia Pacific region hosts both large-scale consumer markets and cost-competitive manufacturing hubs, attracting global semiconductor companies to establish production and research facilities locally.

Furthermore, advancements in AI algorithms and machine learning models have increased the utility of AI chips, making them indispensable for tasks such as natural language processing, computer vision, and autonomous systems. Collaborative ecosystems involving academia, industry, and government research institutions further support innovation, knowledge transfer, and talent development in AI hardware. In combination, these technological demands, supportive policies, economic advantages, and collaborative innovation networks are key factors driving the accelerated adoption of AI chips across the Asia Pacific region, positioning it as a leading hub for AI-driven transformation.

Get more information on this report

AI Chip Market Research Report Guidance:

The report includes qualitative and quantitative data in the AI chip market across type, function, and industry vertical, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the AI chip market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the AI chip market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the AI chip market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover AI chip market segments by offering, type, connectivity, power rating, power source, and end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the AI chip market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

AI Chip Market News and Key Development:

The AI chip market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the AI chip market are:

In December 2025, Amazon EC2 Trn3 UltraServers powered by AWS's first 3nm AI chip help organizations of all sizes run their most ambitious AI training and inference workloads. Trainium3 UltraServers deliver high performance for AI workloads with up to 4.4x more compute performance, 4x greater energy efficiency, and almost 4x more memory bandwidth than Trainium2 UltraServers—enabling faster AI development with lower operational costs.

In October 2025, Qualcomm Technologies, Inc. announced the launch of its next-generation AI inference-optimized solutions for data centers: the Qualcomm AI200 and AI250 chip-based accelerator cards, and racks. Building off the Company’s NPU technology leadership, these solutions offer rack-scale performance and superior memory capacity for fast AI inference at high performance per dollar per watt—marking a major leap forward in enabling scalable, efficient, and flexible generative AI across industries.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - AI Chip Market

Advanced Micro Devices, Inc.

Apple Inc.

Baidu, Inc.

Google LLC

Graphcore

Huawei Technologies Co., Ltd.

Intel Corporation

NVIDIA Corporation

Qualcomm Technologies, Inc.

SK HYNIX INC.

Frequently Asked Questions

How big is the AI Chip Market?

The AI Chip Market is valued at US$ 199.97 Billion in 2025, it is projected to reach US$ 653.68 Billion by 2033.

What is the CAGR for AI Chip Market by (2026 - 2033)?

As per our report AI Chip Market, the market size is valued at US$ 199.97 Billion in 2025, projecting it to reach US$ 653.68 Billion by 2033. This translates to a CAGR of approximately 15.96% during the forecast period.

What segments are covered in this report?

The AI Chip Market report typically cover these key segments-

Type (CPU, GPU, ASIC, FPGA, Others)

Function (Training and Inference)

Industry Vertical (BFSI, Retail, IT & Telecom, Automotive & Transportation, Healthcare, Media & Entertainment, Others)

What is the historic period, base year, and forecast period taken for AI Chip Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the AI Chip Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in AI Chip Market?

The AI Chip Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Advanced Micro Devices, Inc.

Apple Inc.

Baidu, Inc.

Google LLC

Graphcore

Huawei Technologies Co., Ltd.

Intel Corporation

NVIDIA Corporation

Qualcomm Technologies, Inc.

SK HYNIX INC.

Who should buy this report?

The AI Chip Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the AI Chip Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For AI Chip Market

Get Free Sample For AI Chip Market