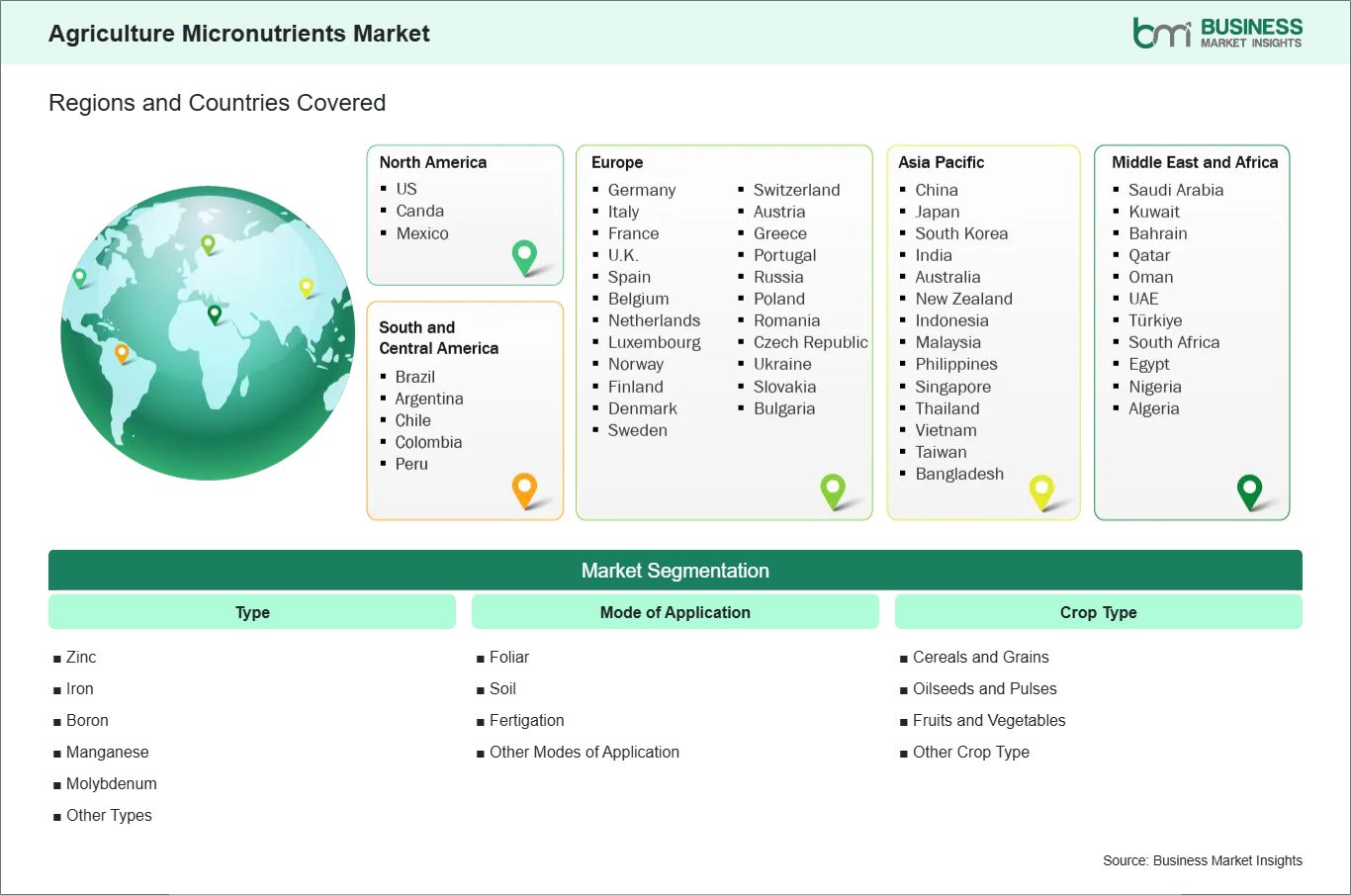

Type (Zinc, Iron, Boron, Manganese, Molybdenum, and Other Types)

Mode of Application (Foliar, Soil, Fertigation, and Other Modes of Application)

Crop Type (Cereals and Grains (Corn, Wheat, Rice, and Other Cereals and Grains), Oilseeds and Pulses (Soybean, Cotton, Rapeseed/Canola, Peas and Legumes, and Other Oilseeds and Pulses), Fruits and Vegetables (Tomatoes, Chilies, Onions, Banana, Citrus Fruits, Berries, and Other Fruits and Vegetables), and Other Crop Type)

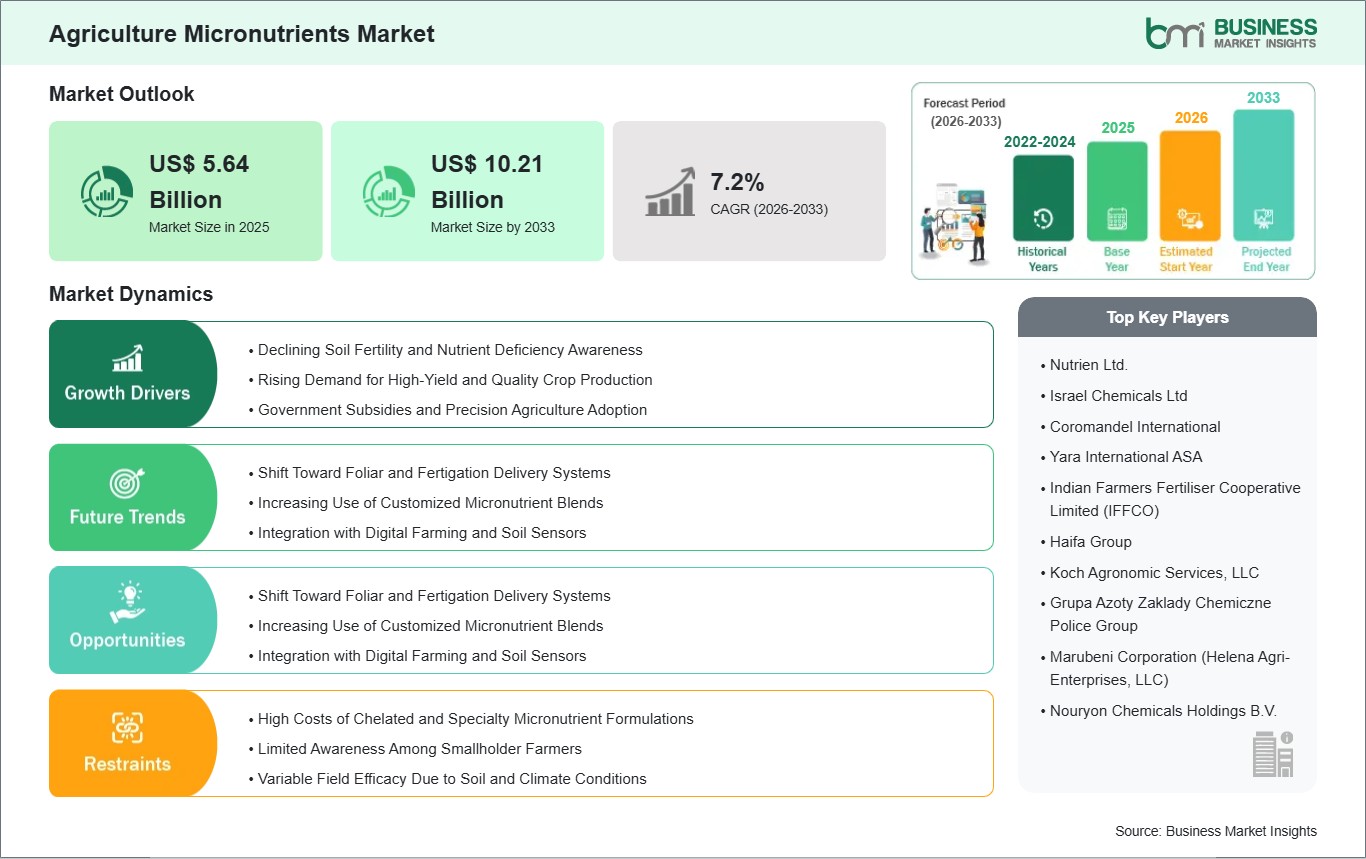

The Agriculture Micronutrients Market size is expected to reach US$ 10.21 Billion by 2033 from US$ 5.64 Billion in 2025. The market is estimated to record a CAGR of 7.70% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Agricultural micronutrients are essential trace elements, such as zinc, boron, iron, manganese, copper, and molybdenum. They play a critical role in modern crop nutrition and high-productivity farming systems. These nutrients support basic physiological processes like enzyme activation, photosynthesis, and hormone regulation. They can be applied through soil, foliar sprays, fertigation, or seed treatment to various crops. This helps to correct deficiencies, improve yield quality, and enhance stress tolerance. The market is growing steadily due to widespread soil nutrient depletion, rising demand for high-value and nutritious food, and the increasing use of precision agriculture technologies. Supportive government policies and greater farmer awareness of balanced fertilization are also speeding up global adoption.

However, the market faces significant challenges such as the technical difficulties of ensuring correct dosage and application, the sensitivity to soil conditions, and fluctuations in raw material costs. Additional issues are fragmented supply chains, varying regulatory standards, and the ongoing need for farmer education. Nevertheless, the market outlook remains positive due to advancements in chelated and nano-formulations, the integration of micronutrients with digital farming tools, and the focus on biofortification and sustainable practices. These trends highlight the essential role of micronutrients in creating resilient, efficient, and productive agricultural systems to secure future global food supply.

Key segments that contributed to the derivation of the agriculture micronutrients market analysis are type, mode of application, and crop type.

By type, the agriculture micronutrients market is categorized into zinc, iron, boron, manganese, molybdenum, and other types. The molybdenum segment dominated the market in 2025.

By mode of application, the market is segmented into foliar, soil, fertigation, and other modes of application. The foliar segment dominated the market in 2025.

By crop type, the agricultural activator adjuvants market is categorized into cereals and grains, oilseeds and pulses, fruits and vegetables, and Others. The cereals and grains segmented is further sub-segmented into corn, wheat, rice, and others. The oilseeds and pulses segment is further sub-segmented into soybean, cotton, rapeseed/canola, peas and legumes, and others. The fruits and vegetables segment is further sub-segmented into tomatoes, chilies, onions, bananas, citrus fruits, berries, and others. The cereals and grains segment held the largest share of the market in 2025.

Agriculture Micronutrients Market Drivers and Opportunities:

Widespread Soil Nutrient Depletion and Degradation

Intensive farming practices and the widespread use of high-yielding crop varieties have caused a significant and ongoing removal of micronutrients from soil without sufficient replenishment. This depletion worsens due to soil erosion, unbalanced fertilization that focuses only on NPK, and the low levels of natural organic matter in many agricultural soils. Consequently, micronutrient deficiencies have become a major limiting factor for crop productivity and quality across many global farmlands. This growing agronomic challenge is driving the demand for targeted micronutrient solutions, as farmers increasingly realize that macronutrients alone cannot maintain yields. Regulatory and educational programs that promote soil health testing and balanced fertilization are encouraging the use of micronutrients in standard farming practice. This makes them a key input for maintaining soil fertility and ensuring reliable harvests.

Integration with Digital Agriculture and Precision Delivery Platforms

The rise of precision farming tools, such as soil sensors, drone-based spectral imaging, and AI-driven analytics, allows for precise mapping of micronutrient deficiencies in fields. This creates a strong opportunity for formulating and applying customized micronutrient blends at variable rates. These technologies support nutrient management that focuses on using the right source, right rate, right time, and right place, which greatly improves efficiency and farm economics. For micronutrient suppliers, this shift opens new paths for creating valuable, data-linked product and service bundles, along with smart formulations that work with modern equipment. This integration enhances crop performance and resource efficiency, positioning micronutrients as a key element of connected, sustainable, and data-driven farm management systems.

Agriculture Micronutrients Market Size and Share Analysis:

The Agriculture Micronutrients market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type, mode of application, and crop type, offering insights into their contribution to overall market performance.

Based on type, the molybdenum subsegment dominates the agriculture micronutrients market. Molybdenum is essential for nitrogen fixation in legumes and for using nitrogen efficiently within plants. Its demand comes from the growing legume cultivation, the need to improve fertilizer efficiency, and the common molybdenum deficiency in acidic soils. This nutrient helps support sustainable nitrogen management practices, making it important for precision crop nutrition.

Agriculture Micronutrients Market Report Coverage and Deliverables:

The " Agriculture Micronutrients Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Agriculture Micronutrients market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Agriculture Micronutrients market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Agriculture Micronutrients market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the agriculture micronutrients market

Detailed company profiles, including SWOT analysis

The geographical scope of the Agriculture Micronutrients market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. The Asia Pacific Agriculture Micronutrients Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia Pacific. Asia Pacific shows strong growth in the global agricultural micronutrients market. This growth is due to its large arable land, intensive farming practices, and the urgent need to improve soil fertility. The rising population, increased food demand, and the decline of arable land are speeding up the use of micronutrients to fix deficiencies and enhance crop yield and quality.

Major government efforts to promote balanced fertilization, growing awareness among farmers, and the rise of high-value crop farming are boosting production and consumption in the region. Together, these factors make Asia Pacific a significant consumer and a rapidly developing producer of agricultural micronutrients, highlighting its important role in the global market.

Get more information on this report

Agriculture Micronutrients Market Research Report Guidance:

The report includes qualitative and quantitative data in the Agriculture Micronutrients market across type, mode of application, crop type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Agriculture Micronutrients market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Agriculture Micronutrients market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Agriculture Micronutrients market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Agriculture Micronutrients market segments by type, mode of application, crop type, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Agriculture Micronutrients market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Agriculture Micronutrients Market News and Key Development:

The Agriculture Micronutrients market is evaluated by gathering qualitative and quantitative data post-primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the agriculture micronutrients market are:

In December 2024, US-based Sound Agriculture secured a $25 million extension of its Series D raise, enabling the expansion of its plant epigenetics platform and bio-inspired nutrient efficiency solutions, aimed at promoting healthier soils, higher crop yields, and climate-friendly farming practices.

In July 2024, Syngenta Biologicals and Intrinsyx Bio partnered to introduce innovative endophyte formulations aimed at enhancing sustainability and crop yields through seed treatment and foliar applications. This collaboration will provide farmers with access to Intrinsyx Bio's endophyte formulations, which fix atmospheric nitrogen and improve nutrient uptake, thereby reducing reliance on synthetic fertilizers. Syngenta's investment in biological solutions emphasizes its commitment to sustainable farming and environmental management.

Key Sources Referred:

World Bank – Global Trade IndicatorsEuropean Chemicals AgencyInternational Council of Chemical AssociationsInternational Monetary Fund (IMF)World Trade Organization (WTO)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Agriculture Micronutrients Market

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Agriculture Micronutrients Market?

The Agriculture Micronutrients Market is valued at US$ 5.64 Billion in 2025, it is projected to reach US$ 10.21 Billion by 2033.

What is the CAGR for Agriculture Micronutrients Market by (2026 - 2033)?

As per our report Agriculture Micronutrients Market, the market size is valued at US$ 5.64 Billion in 2025, projecting it to reach US$ 10.21 Billion by 2033. This translates to a CAGR of approximately 7.70% during the forecast period.

What segments are covered in this report?

The Agriculture Micronutrients Market report typically cover these key segments-

Type (Zinc, Iron, Boron, Manganese, Molybdenum, and Other Types)

Mode of Application (Foliar, Soil, Fertigation, and Other Modes of Application)

Crop Type (Cereals and Grains (Corn, Wheat, Rice, and Other Cereals and Grains), Oilseeds and Pulses (Soybean, Cotton, Rapeseed/Canola, Peas and Legumes, and Other Oilseeds and Pulses), Fruits and Vegetables (Tomatoes, Chilies, Onions, Banana, Citrus Fruits, Berries, and Other Fruits and Vegetables), and Other Crop Type)

What is the historic period, base year, and forecast period taken for Agriculture Micronutrients Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Agriculture Micronutrients Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Agriculture Micronutrients Market?

The Agriculture Micronutrients Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Nutrien Ltd.

Israel Chemicals Ltd

Coromandel International

Yara International ASA

Indian Farmers Fertiliser Cooperative Limited (IFFCO)

The Agriculture Micronutrients Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Agriculture Micronutrients Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Agriculture Micronutrients Market

Get Free Sample For Agriculture Micronutrients Market