01

Market Summery

Executive Summary and Global Market Analysis

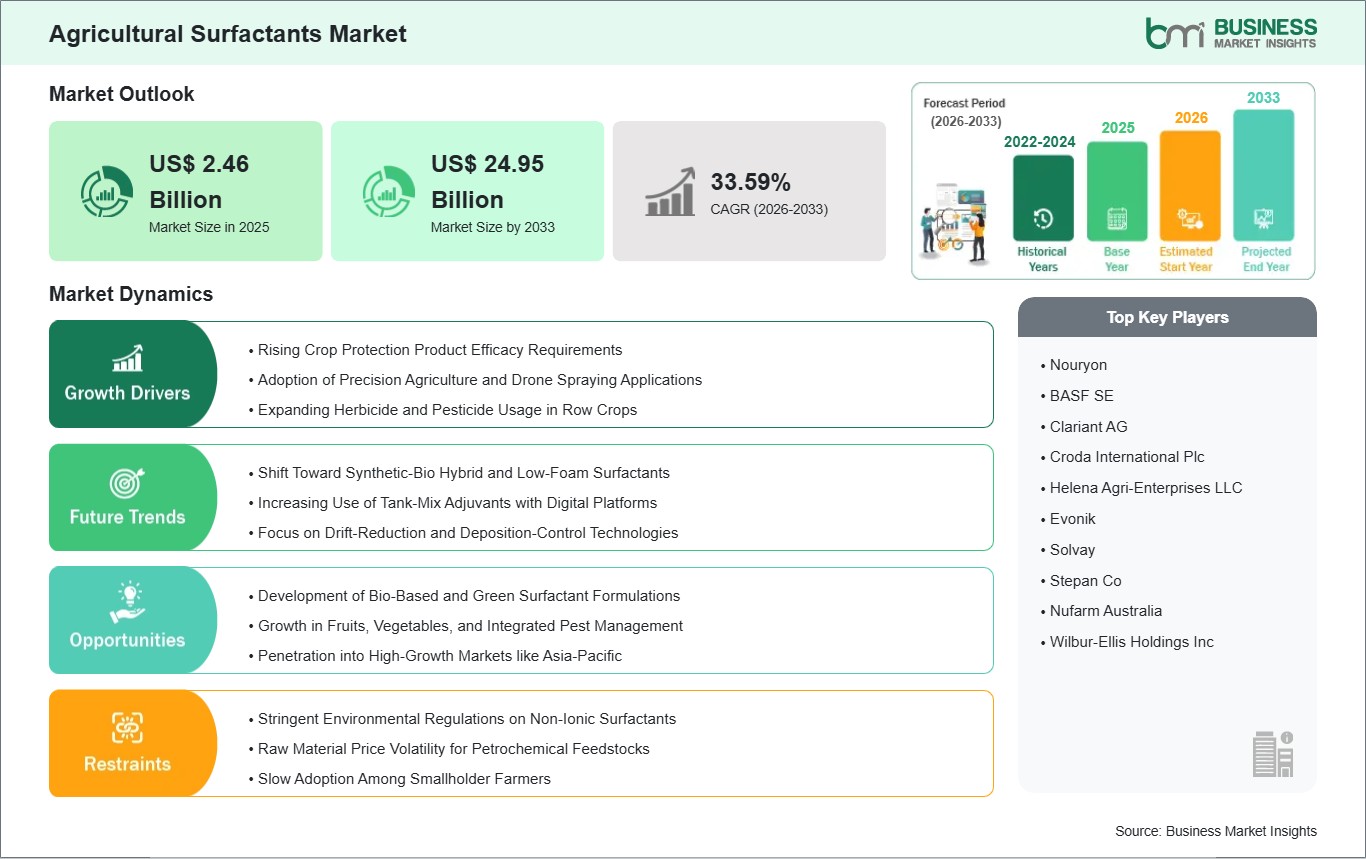

Agricultural surfactants are integral components of the global agrochemicals industry, functioning as formulation enhancers that significantly improve the performance, stability, and application efficiency of crop protection products. They are incorporated into herbicides, insecticides, fungicides, fertilizers, and plant growth regulators to optimize wetting, spreading, adhesion, penetration, and dispersion on plant surfaces. By enabling uniform distribution of active ingredients and improving their absorption into plant tissues, surfactants help reduce losses caused by runoff or spray drift. These attributes make them indispensable across a wide range of crop categories, including cereals, oilseeds, fruits, vegetables, and plantation crops. Within modern farming systems, surfactants contribute to maximizing yields, improving pest and weed control, and supporting precision agriculture practices.

Their advantages - such as enhanced formulation compatibility, improved efficacy at lower dosages, increased rainfastness, and adaptability across diverse climatic and soil conditions - continue to drive adoption. Market expansion is further supported by rising global food demand, the emphasis on advanced crop protection technologies, the growth of commercial agriculture, and the need to intensify production on limited arable land.

Significant innovation is also emerging in bio‑based and nonionic surfactants, advanced formulation technologies, and sustainability‑oriented, residue‑reducing inputs. These trends position agricultural surfactants as a critical enabler of high‑productivity, environmentally responsible farming. Despite strong growth prospects, the market faces challenges including volatile raw material prices, stringent regulatory constraints related to chemical residues, and environmental concerns associated with petroleum‑based surfactants. Additionally, strict agrochemical regulations, high development costs for eco‑friendly alternatives, and price sensitivity among farmers in developing markets pose barriers to adoption. Variations in crop type, water quality, and environmental conditions also require precise formulation control, adding complexity to manufacturing.

Nonetheless, substantial opportunities lie ahead. The development of biodegradable and bio‑based surfactants, the global shift toward sustainable agriculture, and the increasing adoption of integrated pest management and precision spraying systems are expected to fuel future demand. Ultimately, the trajectory of the agricultural surfactants market will be shaped by continuous R&D investment, supportive regulatory frameworks favoring safer inputs, and the accelerating transition toward high‑efficiency, environmentally sustainable farming solutions.

03

Segment Analysis

Agricultural Surfactants Market Segmentation

Key segments that contributed to the derivation of the agricultural surfactants market analysis are type, substrate, application, and crop type.

- By type, the agricultural surfactants market is segmented into non-ionic, anionic, cationic, and amphoteric. The non-ionic segment dominated the market in 2025.

- By substrate, the market is divided into synthetic and bio-based. The synthetic segment dominated the market in 2025.

- By application, the agricultural surfactants market is categorized into herbicides, insecticides, fungicides, and other applications. The herbicides segment held the largest share of the market in 2025.

- By crop type, the agricultural surfactants market is categorized into cereals and grains, oilseeds and pulses, fruits and vegetables, and other crop types. The fruits and vegetables segment dominated the market in 2025. The cereals and grains segment is further sub-segmented into corn, wheat, rice, and other cereals and grains. The oilseeds and pulses segment is further sub-segmented into soybean, sunflower, and other oilseeds and pulses. The fruits and vegetables segment is further sub-segmented into root and tuber vegetables, leafy vegetables, pome fruits, berries, citrus fruits, and other fruits and vegetables.

04

Market Forces

Agricultural Surfactants Market Drivers and Opportunities

Rising Adoption of Advanced Crop Protection and Yield Enhancement Solutions

Agricultural surfactants are increasingly being deployed to enhance the performance of herbicides, insecticides, fungicides, and fertilizers by improving spray coverage, adhesion, and penetration across crop surfaces. As modern farming systems intensify their focus on maximizing output from limited arable land, growers are adopting high‑efficiency crop protection strategies that rely on surfactants to ensure uniform and effective delivery of active ingredients. The rising adoption of precision agriculture—characterized by targeted chemical application, reduced wastage, and data‑driven spraying practices is further elevating demand for high‑performance surfactant formulations. At the same time, the expansion of high‑value crops such as fruits, vegetables, and oilseeds is heightening the need for advanced weed and pest management solutions, directly contributing to market growth. Farmers are also gravitating toward surfactants due to their ability to offer cost‑effective, reliable performance across diverse climatic conditions and crop environments. These attributes make surfactants a preferred input for achieving consistent results, optimizing resource use, and improving the overall effectiveness of agrochemical applications.

Development of Bio-Based and Environmentally Safer Surfactant Technologies

Conventional agricultural surfactants—predominantly derived from petrochemical sources—are facing increasing regulatory and environmental scrutiny due to concerns over toxicity, environmental persistence, and adverse ecosystem impacts. As global sustainability standards tighten and regulatory agencies impose stricter controls on agrochemical formulations, demand is shifting decisively toward bio‑based, biodegradable, and low‑toxicity surfactant alternatives.

Next‑generation surfactants formulated from renewable feedstocks such as plant oils, natural fatty acids, and sugars offer improved environmental profiles while maintaining high performance in agricultural spray applications. This transition supports broader sustainability objectives, including integrated pest management practices, residue reduction, and the overall movement toward greener agricultural inputs. Advancements in formulation science, green chemistry, and scalable production technologies are making eco‑friendly surfactants increasingly cost‑competitive and consistent in performance. As a result, these solutions are gaining traction among agrochemical manufacturers and growers seeking to balance regulatory compliance with operational efficiency. Companies that prioritize sustainable product development, invest in R&D, and align with emerging regulatory standards are well‑positioned to capture new market opportunities, establish a differentiated competitive advantage, and meet the growing global demand for environmentally responsible agricultural inputs.

05

Size and Share Analysis

Agricultural Surfactants Market Size and Share Analysis

The Agricultural Surfactants market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type, substrate, application, and crop type, offering insights into their contribution to overall market performance.

Based on substrate, the synthetic subsegment dominates the agricultural surfactants market. Synthetic substrates have gained immense traction in agriculture due to purity, consistency, and dependability. They improve the wetting, spreading, and adhesion of herbicides, insecticides, and fertilizers. These are more stable and compatible with large-scale formulations, making them the preferred choice for all crops.

07

Report Coverage

Agricultural Surfactants Market Report Coverage and Deliverables

The " Agricultural Surfactants Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Agricultural Surfactants market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Agricultural Surfactants market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Agricultural Surfactants market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the agricultural surfactants market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Agricultural Surfactants Market Geographic Insights

The geographical scope of the Agricultural Surfactants market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

The Asia Pacific Agricultural Surfactants Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia Pacific. Asia Pacific is a major marketplace for farming surfactant products due to a booming agricultural and agrochemical industry. The market growth is also supported by increasing demand for efficient crop protection, precision farming, and crop solutions.

Increasing urbanization, growing farm mechanization, and growing attention to sustainable and environmentally safe agricultural practices further confirm the position of the Asia Pacific as a significant producer and consumer of surfactants. These factors collectively highlight the strategic nature of the region in the global value chain in agricultural surfactants.

10

Industry Activity

Recent Developments

The Agricultural Surfactants market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the agricultural surfactants market are:

- In October 2025, Godrej Agrovet Limited launched Ashitaka, a new herbicide for maize crops, developed in collaboration with ISK Japan. This innovative product effectively controls grasses and broad-leaved weeds, which pose significant challenges for maize farmers in India, especially during the initial growth stages. Applied at the 2 to 4 leaf weed stage, Ashitaka offers effective weed control.

- In March 2025, Syngenta acquired natural compounds and genetic strains from Novartis, enhancing its agricultural research capabilities. This acquisition provides Syngenta with access to novel leads and integrated strengths in bio-engineering, data science, fermentation, and analytics.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade Indicators European Chemicals Agency International Council of Chemical Associations International Monetary Fund (IMF) World Trade Organization (WTO) International Trade Administration (ITA) Company Websites Company Annual Reports Company Investor Presentations