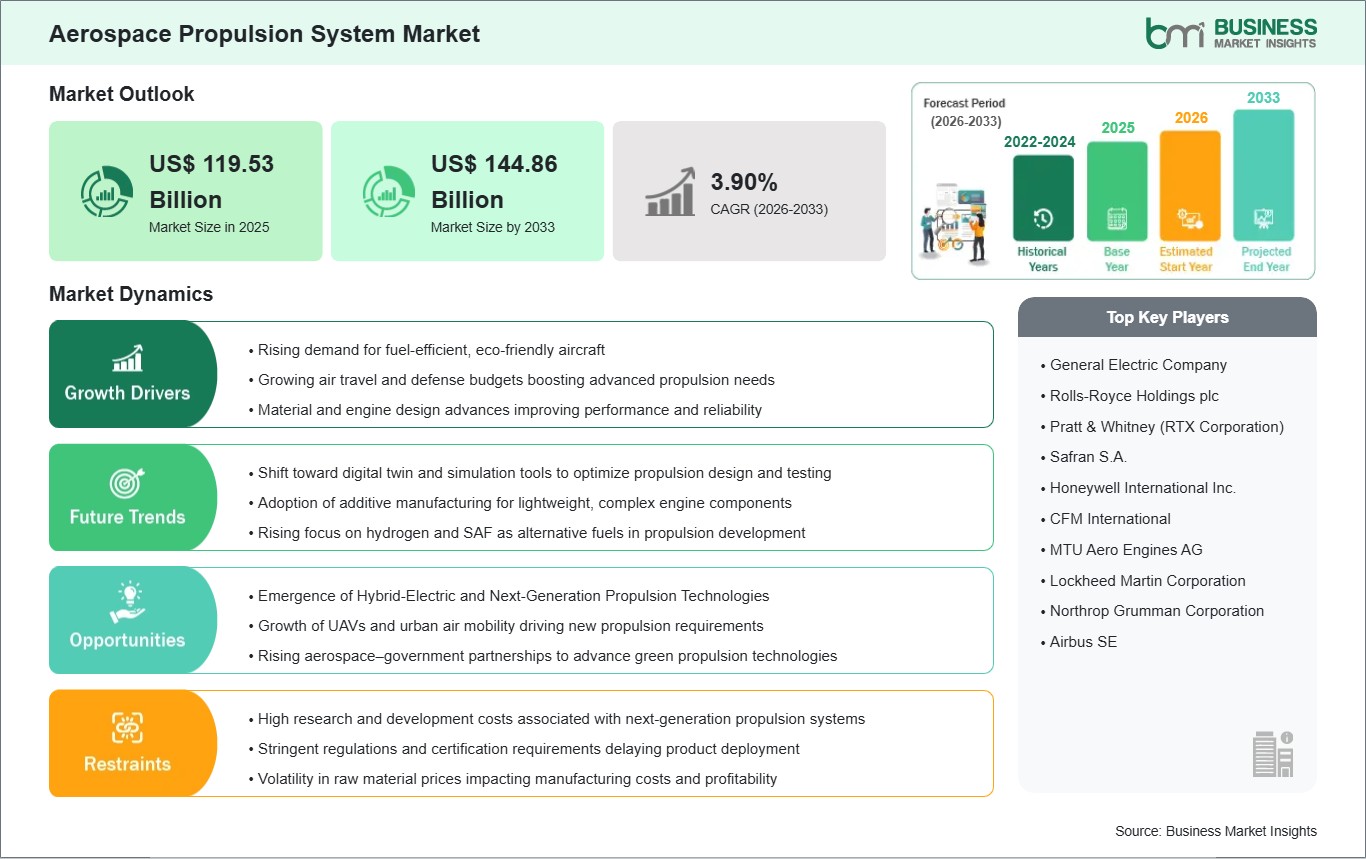

The Aerospace Propulsion System Market size is expected to reach US$ 144.86 Billion by 2033 from US$ 119.53 Billion in 2025. The market is estimated to record a CAGR of 2.43% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The Aerospace Propulsion System market is a foundational pillar of the global aerospace and defense industry, enabling the development of efficient, reliable, and high-performance aircraft and space platforms. Propulsion systems are central to determining aircraft range, speed, fuel efficiency, payload capacity, and environmental performance across commercial aviation, military aircraft, unmanned systems, and space launch vehicles. Continuous innovation in propulsion technologies supports the industry’s objectives of improving operational efficiency, reducing emissions, and meeting increasingly stringent safety and regulatory requirements. Advanced propulsion solutions, supported by digital engineering, simulation, and testing capabilities, allow manufacturers to optimize performance while reducing development cycles and lifecycle costs. Aerospace propulsion systems are at the core of managing the growing complexity of next-generation platforms, including wide-body and narrow-body commercial aircraft, advanced fighter jets, helicopters, and space systems. These solutions enable critical capabilities such as higher thrust-to-weight ratios, improved thermal efficiency, reduced noise levels, and enhanced reliability. As aerospace platforms evolve to support longer ranges, higher payloads, and more demanding mission profiles, robust and efficient propulsion technologies play a decisive role in maintaining competitiveness and operational readiness across civil and defense markets.

Several factors are driving the growth of the aerospace propulsion system market, including the recovery and expansion of global air travel, rising defense spending, and increasing demand for fuel-efficient and low-emission aircraft. Additionally, the emergence of sustainable aviation fuels (SAF), hybrid-electric propulsion concepts, and advanced materials is accelerating innovation and investment across the value chain. Ongoing modernization programs, fleet renewals, and growing interest in space exploration and satellite deployment further contribute to sustained market expansion. Despite strong long-term prospects, the market faces challenges such as high development and manufacturing costs, lengthy certification cycles, and complex supply chains. Stringent environmental regulations, technical risks associated with new propulsion architectures, and a shortage of highly skilled engineering talent also pose constraints. Nevertheless, continued R&D investment, strategic partnerships, and advancements in digital design and manufacturing are expected to support scalable growth and long-term competitiveness in the aerospace propulsion system market.

Aerospace Propulsion System Market - Strategic Insights:

Get more information on this report

Aerospace Propulsion System Market Segmentation Analysis:

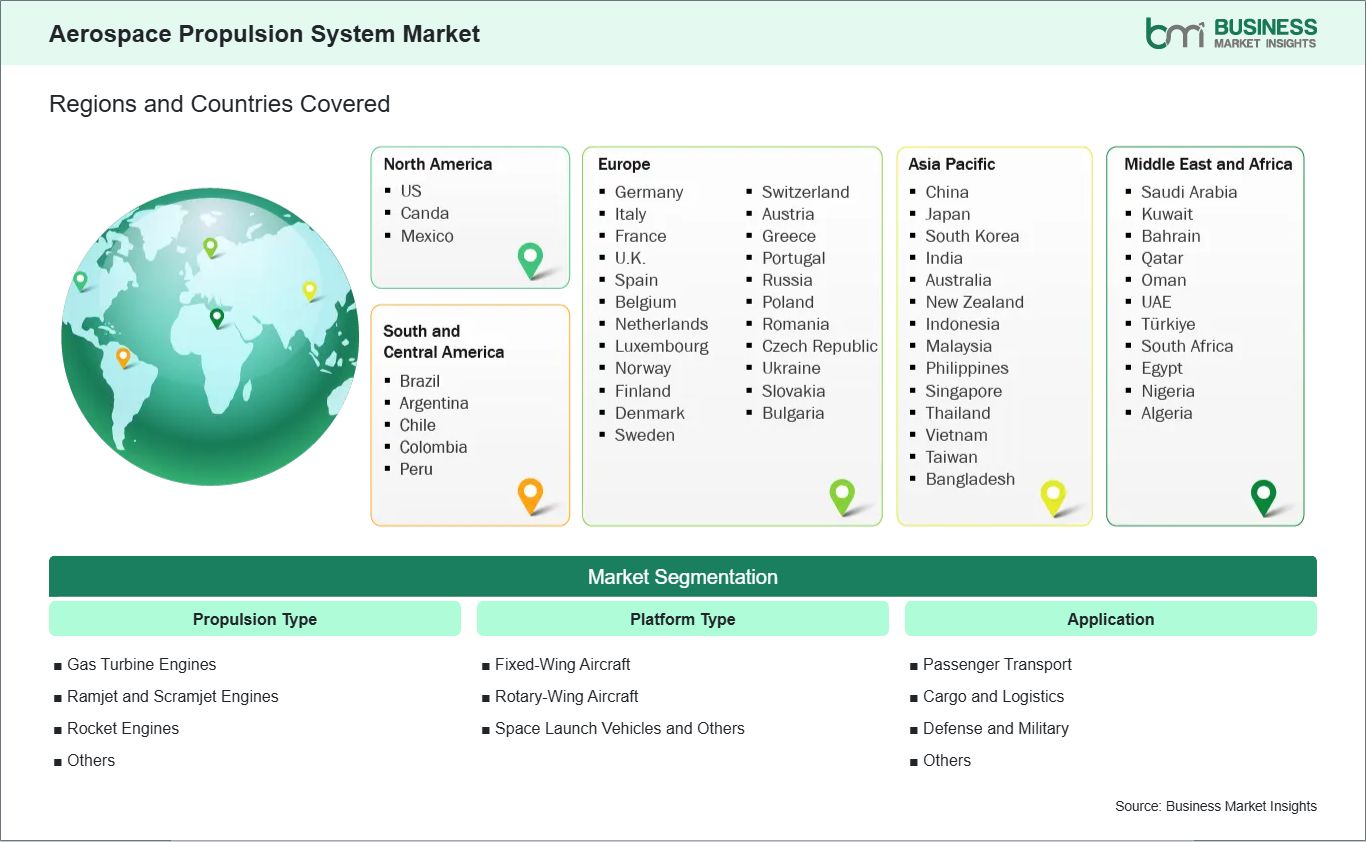

Key segments that contributed to the derivation of the Aerospace Propulsion System market analysis are equipment type, and end user.

By propulsion type, the Aerospace Propulsion System market is divided into Gas Turbine Engines, Ramjet and Scramjet Engines, Rocket Engines, and Others. The Gas Turbine Engines segment dominated the market in 2024.

By platform type, the market is divided into Fixed-Wing Aircraft, Rotary-Wing Aircraft, Space Launch Vehicles and Others. The Fixed-Wing Aircraft held the larger share in 2024.

By application, the market is divided into Passenger Transport, Cargo and Logistics, Defense and Military, Others. The Passenger Transport held the larger share in 2024.

Aerospace Propulsion System Market Drivers and Opportunities:

Growing Demand for Fuel-Efficient and Environmentally Sustainable Aircraft

The increasing global emphasis on fuel efficiency and environmental sustainability is a key driver of the aerospace propulsion system market. Airlines, defense agencies, and aircraft manufacturers are under mounting pressure to reduce operating costs, carbon emissions, and noise levels while maintaining high performance and safety standards. Fuel expenses represent a significant portion of airline operating costs, making propulsion efficiency a critical competitive factor. As a result, there is strong demand for next-generation propulsion systems that deliver higher thrust-to-weight ratios, improved thermal efficiency, and lower fuel consumption.

Regulatory bodies across North America, Europe, and Asia-Pacific are implementing increasingly stringent emissions and noise regulations, compelling manufacturers to invest in advanced propulsion technologies. Innovations such as high-bypass turbofan engines, geared turbofan architectures, advanced materials, and improved aerodynamics are gaining rapid traction. In parallel, military programs are also prioritizing efficient propulsion systems to extend operational range, improve mission endurance, and reduce logistical complexity. These combined commercial and defense requirements are driving sustained investment in propulsion system research, development, and fleet modernization, making fuel efficiency and sustainability a fundamental growth driver for the aerospace propulsion system market.

Emergence of Hybrid-Electric and Next-Generation Propulsion Technologies

The development of hybrid-electric and next-generation propulsion technologies presents a significant long-term opportunity for the aerospace propulsion system market. As the industry explores alternatives to conventional gas turbine engines, hybrid-electric, fully electric, and hydrogen-based propulsion concepts are gaining increasing attention from aircraft manufacturers, governments, and investors. These technologies offer the potential to significantly reduce emissions, operating costs, and noise, particularly for regional aircraft, urban air mobility (UAM) platforms, and short-haul operations.

Governments and regulatory authorities are actively supporting innovation through funding programs, research initiatives, and public–private partnerships aimed at accelerating the commercialization of sustainable propulsion solutions. Aerospace OEMs and engine manufacturers are investing heavily in electric motors, power electronics, energy storage systems, and advanced thermal management solutions to enable scalable deployment. Additionally, advancements in digital engineering, additive manufacturing, and materials science are lowering development barriers and enabling rapid prototyping of new propulsion architectures.

Aerospace Propulsion System Market Size and Share Analysis:

By propulsion type, the Aerospace Propulsion System market is divided into Gas Turbine Engines, Ramjet and Scramjet Engines, Rocket Engines, and Others. The Gas Turbine Engines segment dominated the market in 2024. Gas turbine engines including turbofan, turboprop, turbojet, and turboshaft variants offer an optimal balance of thrust, fuel efficiency, and reliability, making them the propulsion system of choice for the majority of aircraft and rotorcraft

By platform type, the market is divided into Fixed-Wing Aircraft, Rotary-Wing Aircraft, Space Launch Vehicles and Others. The Fixed-Wing Aircraft held the larger share in 2024. Fixed-wing aircraft, including commercial airliners, regional jets, and business aircraft, demand highly reliable and fuel-efficient propulsion systems to ensure performance across long-haul and short-haul routes.

By application, the market is divided into Passenger Transport, Cargo and Logistics, Defense and Military, Others. The Passenger Transport held the larger share in 2024. The dominance of passenger transport reflects the global expansion of commercial aviation, rising air travel demand, and fleet modernization initiatives, which require high-efficiency, low-emission propulsion systems.

Aerospace Propulsion System Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

General Electric Company

Rolls-Royce Holdings plc

Pratt & Whitney (RTX Corporation)

Safran S.A.

Honeywell International Inc.

CFM International

MTU Aero Engines AG

Lockheed Martin Corporation

Northrop Grumman Corporation

Airbus SE

Get more information on this report

Aerospace Propulsion System Market Report Coverage and Deliverables:

The "Aerospace Propulsion System Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Aerospace Propulsion System market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Aerospace Propulsion System market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Aerospace Propulsion System market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Aerospace Propulsion System market

Detailed company profiles, including SWOT analysis

Aerospace Propulsion System Market Geographic Insights:

The Aerospace Propulsion System market is geographically segmented into North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. Among these regions, Asia Pacific is expected to witness the strongest growth and remain a leading market throughout the forecast period, driven by rapid industrialization, expanding commercial and defense aviation sectors, and increasing investments in aerospace infrastructure. The region benefits from large-scale aircraft manufacturing capabilities, growing airline fleets, and government-backed aerospace programs, positioning it as a key hub for propulsion system development and adoption.

Within Asia Pacific, the market encompasses China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. Growth in this region is supported by robust aircraft production, rising demand for commercial and regional air transport, and strong defense modernization programs. Leading economies such as China, Japan, South Korea, and India are driving adoption of advanced propulsion technologies, including high-bypass turbofan engines, turboprops, and next-generation hybrid-electric and sustainable fuel systems. These countries are also leveraging digital engineering, additive manufacturing, and predictive maintenance technologies to enhance efficiency, reliability, and performance in propulsion systems.

Demand for aerospace propulsion systems in Asia Pacific is further fueled by commercial aviation, defense, space launch programs, and emerging urban air mobility applications. Significant investments in engine manufacturing facilities, R&D centers, testing laboratories, and compliance certification infrastructure are accelerating market expansion. Additionally, public–private partnerships, government-led aerospace initiatives, and workforce development programs aimed at technical and engineering expertise are strengthening the regional ecosystem.

Despite challenges such as high capital expenditure, complex regulatory frameworks, and integration of new propulsion technologies with legacy aircraft platforms, Asia Pacific remains strategically positioned as a global hub for aerospace propulsion systems, supported by efficient supply chains, cost-competitive manufacturing, and strong domestic demand.

Get more information on this report

Aerospace Propulsion System Market Research Report Guidance:

The report includes qualitative and quantitative data in the Aerospace Propulsion System market across module, insulation, and application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Aerospace Propulsion System market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Aerospace Propulsion System market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Aerospace Propulsion System market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Aerospace Propulsion System market segments by propulsion type, paltform type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Aerospace Propulsion System market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer

Aerospace Propulsion System Market News and Key Development:

The Aerospace Propulsion System market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Aerospace Propulsion System market are:

In January 2026, GE Aerospace and Lockheed Martin announced the successful completion of a series of engine tests for a liquid-fueled Rotating Detonation Ramjet (RDR). The ground-based demonstrations, conducted at GE Aerospace’s research facility, validated a propulsion system designed to enable missiles to fly at hypersonic speeds exceeding Mach 5 with significantly increased range.

In January 2026, L3Harris Technologies, announced the intended sale of a majority stake in its Space Propulsion and Power Systems business to AE Industrial Partners, shifting control over one of its marquee engines: the RL10.

Key Sources Referred:

International Air Transport Association (IATA)Federal Aviation Administration (FAA) and other national civil aviation authoritiesEuropean Union Aviation Safety Agency (EASA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Aerospace Propulsion System Market

General Electric Company

Rolls-Royce Holdings plc

Pratt & Whitney (RTX Corporation)

Safran S.A.

Honeywell International Inc.

CFM International

MTU Aero Engines AG

Lockheed Martin Corporation

Northrop Grumman Corporation

Airbus SE

Frequently Asked Questions

How big is the Aerospace Propulsion System Market?

The Aerospace Propulsion System Market is valued at US$ 119.53 Billion in 2025, it is projected to reach US$ 144.86 Billion by 2033.

What is the CAGR for Aerospace Propulsion System Market by (2026 - 2033)?

As per our report Aerospace Propulsion System Market, the market size is valued at US$ 119.53 Billion in 2025, projecting it to reach US$ 144.86 Billion by 2033. This translates to a CAGR of approximately 2.43% during the forecast period.

What segments are covered in this report?

The Aerospace Propulsion System Market report typically cover these key segments-

Propulsion Type (Gas Turbine Engines, Ramjet and Scramjet Engines, Rocket Engines, and Others)

Platform Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Space Launch Vehicles and Others)

Application (Passenger Transport, Cargo and Logistics, Defense and Military, Others

What is the historic period, base year, and forecast period taken for Aerospace Propulsion System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Aerospace Propulsion System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Aerospace Propulsion System Market?

The Aerospace Propulsion System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

General Electric Company

Rolls-Royce Holdings plc

Pratt & Whitney (RTX Corporation)

Safran S.A.

Honeywell International Inc.

CFM International

MTU Aero Engines AG

Lockheed Martin Corporation

Northrop Grumman Corporation

Airbus SE

Who should buy this report?

The Aerospace Propulsion System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Aerospace Propulsion System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Aerospace Propulsion System Market

Get Free Sample For Aerospace Propulsion System Market