01

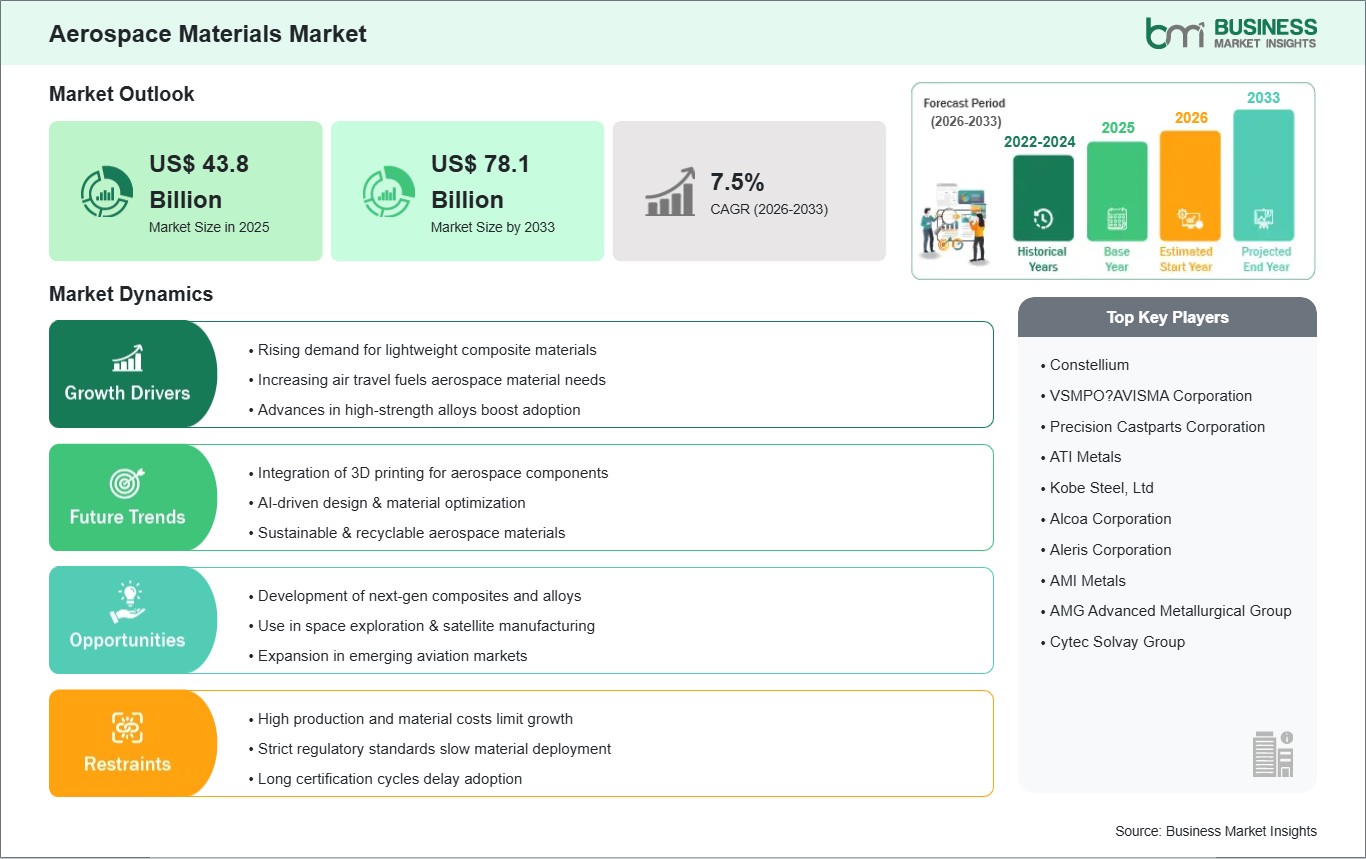

Market Summery

Executive Summary and Global Market Analysis

Aerospace Materials provide the structural and functional foundation for the aviation and space sectors, encompassing aluminum alloys, titanium, superalloys, and advanced composites. These materials offer critical advantages, such as superior fuel efficiency through lightweighting, enhanced corrosion resistance, and the ability to maintain structural integrity under hypersonic speeds and vacuum conditions. Growth is primarily driven by the surge in commercial aircraft backlogs, rising defense modernization budgets, and the rapid expansion of private space exploration. Additionally, the adoption of additive manufacturing (3D printing) is fundamentally transforming the production of complex, topology-optimized components.

However, several challenges can restrain market growth: high production costs and complexity associated with advanced carbon-fiber composites and specialized titanium alloys remain a barrier for mid-tier manufacturers. Unstable global supply chains, especially for rare earth elements and specialized metals, are causing long lead times. Furthermore, the industry also faces strict safety certification requirements and environmental concerns from traditional metallurgical methods, which often conflict with sustainability goals. Despite these hurdles, the market holds immense opportunities in the universal mandate for decarbonized aviation, bio-based composites, and smart materials for real-time structural health monitoring. The transition toward next-generation propulsion systems (hydrogen and electric) and AI-driven material discovery is expected to create significant opportunities for market growth.

03

Segment Analysis

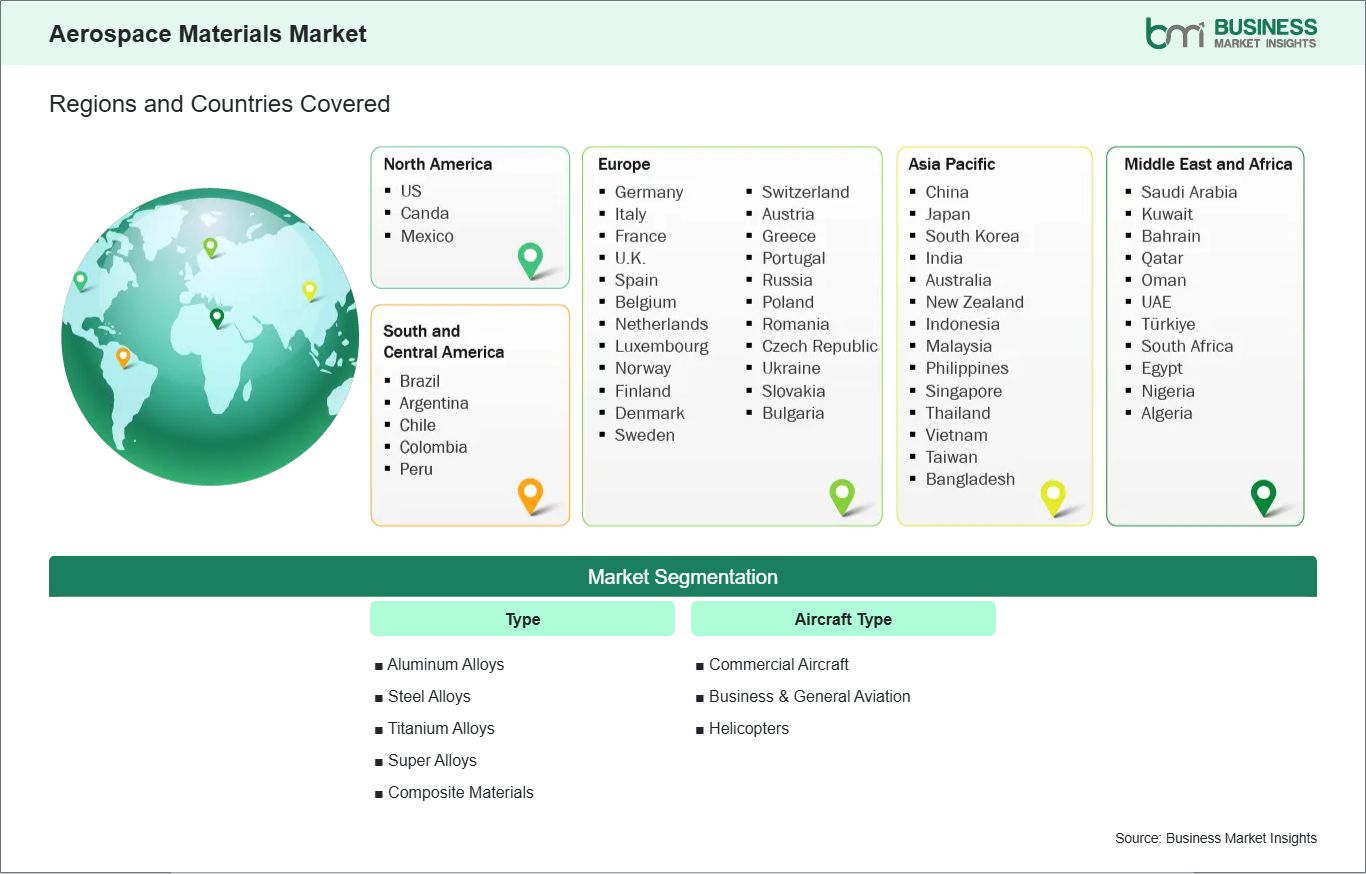

Aerospace Materials Market Segmentation

Key segments that contributed to the derivation of the Aerospace Materials market analysis are type and aircraft type.

- By Type, the market is segmented into Aluminum Alloys, Steel Alloys, Titanium Alloys, Super Alloys, and Composite Materials.

- By Aircraft Type, the market is segmented into Commercial Aircraft, Business & General Aviation, and Helicopters.

04

Market Forces

Aerospace Materials Market Drivers and Opportunities

Fuel Efficiency and E-commerce Expansion

With stricter environmental rules and higher fuel prices, aviation is moving quickly toward lighter, high-performance materials. Advanced composites such as carbon-fiber-reinforced polymers (CFRPs) and new aluminum-lithium alloys are important as they offer high strength for their weight. These materials enable lighter aircraft, directly translating to improved fuel economy and lower operational costs. This demand is further bolstered by the rapid expansion of global e-commerce. The digitalization of commerce and the consumer preference for rapid delivery have made air cargo a critical supply chain component. This surge supports the market as the need for fast, efficient shipping solutions rises to meet complex global demands, prompting manufacturers to ramp up production of new-generation, cargo-efficient aircraft.

The ongoing globalization of trade further propels this market. With more trade agreements and increasingly connected supply chains, businesses now depend on air logistics to ship valuable, time-sensitive products such as electronics and pharmaceuticals internationally. Trade liberalization and free trade zones have created new opportunities, making it easier for developed and emerging economies to trade with each other. Furthermore, multinational companies are diversifying manufacturing strategies to remain resilient against geopolitical shifts, necessitating air cargo solutions that support time-critical supply chains spanning multiple continents. As companies adopt just-in-time inventory practices, the demand for rapid air freight and the advanced materials required for these aircraft is expected to grow steadily.

Additive Manufacturing and Space Exploration

A major high-value opportunity lies in the scaling of additive manufacturing (3D printing) and the development of sustainable composite materials. 3D printing enables the production of complex, topology-optimized parts, leading to drastic waste reduction and shorter lead times for structural components. Simultaneously, the industry’s push toward net-zero goals is creating a market for "green" materials, including bio-derived resins and recyclable thermoplastic composites. These innovations allow manufacturers to meet environmental standards while reducing weight. By integrating AI-driven material modeling to predict performance, companies can lead an era where materials are active, intelligent components of flight.

Another significant opportunity is emerging in commercial space exploration and Urban Air Mobility (UAM). As private enterprises increase satellite launches and lunar missions, there is an escalating demand for materials capable of enduring radiation and thermal cycling, such as high-strength titanium alloys. Additionally, the rise of electric Vertical Take-off and Landing (eVTOL) aircraft creates a frontier for ultra-lightweight structures and battery casing materials. Companies pivoting toward these segments are positioned to capture the next wave of high-margin aerospace innovation.

05

Size and Share Analysis

Aerospace Materials Market Size and Share Analysis

The Aerospace Materials market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type and aircraft type, offering insights into their contribution to overall market performance.

For instance, the Aluminum Alloys subsegment remains a fundamental component of the market, particularly for the construction of Commercial Aircraft. While newer models are incorporating more non-metallic parts, advanced aluminum-lithium alloys continue to be favored for their high strength-to-weight ratio and cost-effectiveness in high-volume airframe manufacturing. These alloys are extensively used in wing skins and fuselage panels where they offer a balanced performance of durability and damage tolerance.

07

Report Coverage

Aerospace Materials Market Report Coverage and Deliverables

The Aerospace Materials Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

- Aerospace Materials market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Aerospace Materials market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Aerospace Materials market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Aerospace Materials market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Aerospace Materials Market Geographic Insights

The geographical scope of the Aerospace Materials market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Aerospace Materials Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily driven by a surge in commercial air travel and the successful development of domestic aircraft programs.

Growth is further bolstered by the rising adoption of advanced composites and lithium-aluminum alloys to achieve sustainability goals and improve fuel efficiency. The establishment of high-tech manufacturing hubs and the proliferation of low-cost carriers across Southeast Asia secures Asia-Pacific’s position as the primary hub for future aerospace material consumption.

10

Industry Activity

Recent Developments

The Aerospace Materials market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Aerospace Materials market are:

- In February 2025, Alleima launched a high-temperature alloy for applications in industries like aerospace and automotive. Alleima® TD, an innovative solution for the heat treatment industry, where there is a need for reliable high temperature materials. The product ensures consistent performance for mineral insulated cable (MIC), measurements, and heating cables, even at extreme temperatures up to 1250°C. Industries with a focus on the production of automotives, aluminium, gas turbines, and aerospace engines are known for their harsh environments that put high demand on surrounding materials in production.

- In January 2025, IMERYS launched Fondag® Aerospace, state-of-the-art concrete engineered to withstand the punishing conditions of rocket launches. The product delivers superior heat and abrasion resistance, with testing showing a 64% improvement in abrasion resistance, enabling reduced downtime and higher operational efficiency for aerospace operators. This product launch reflects a commitment to providing cutting-edge solutions that support our customers’ goals. Fondag® Aerospace’s advanced properties are already delivering value to some of the industry’s most prominent organizations, reinforcing our position as a trusted partner in the aerospace sector.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations