The Aerospace Composites Market size is expected to reach US$ 91.57 Billion by 2033 from US$ 30.3 Billion in 2025. The market is estimated to record a CAGR of 14.83% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Aerospace composites are highly sought-after advanced materials in the world aerospace and defense sector, as they form the basis of the structural solutions that allow the company to achieve high performance of strength-to-weight, fuel efficiency, and design flexibility within a diverse airplane and spacecraft platform. They are mostly used in the production of fuselages, wings, empennage structures, engine parts, interiors, radomes, and space vehicle structures—parts that are widely used in commercial aviation, military aircraft, unmanned aerial vehicles, and helicopters, as well as space exploration missions. Aerospace composites, as a key tool to next-generation airframe construction, have a very high impact on the mechanical strength, fatigue, thermal stability, and corrosion resistance, although at the same time, they greatly contribute to the lightweight construction and long service life. In the commercial aviation sector, they allow reduced fuel consumption, reduced emissions, and increased payload capacity. Aerospace composites facilitate high structural integrity in aerospace applications, radar transparency, and performance in adverse environments of defense and space. In the interiors and secondary structures, they help in reducing weight, enhancing safety, and customizing the designs to guarantee uniform performance and reliability. High stiffness to weight ratios, high durability, and design flexibility to withstand aggressive operations, and the ability to undergo advanced manufacturing processes like automated fiber placement, resin transfer molding are the benefits of using aerospace composites. The growth in the market is highly encouraged by the increase in air passenger numbers in the world, the speeding up rate of aircraft production, the modernisation of military fleets, and the aerospace industry seeking fuel-efficient and lightweight materials. Also, the growth in space programs, urban air mobility, and the growing use of advanced composite technologies in the next generation aircraft platforms also continues to stimulate the market expansion at a global level. These aspects make aerospace composites inevitable materials in the development of high-performance, efficient, and advanced technological aerospace systems.

However, the market faces a number of challenges, such as high cost of materials and manufacturing, complicated fabrication processes, and extensive certification and qualification processes. The lack of volatility in raw material costs, the supply chain, and the low recyclability of conventional composite systems. Market growth can also be restrained by stringent regulatory requirements, large capital outlay to develop high-technology manufacturing facilities, and sensitivity to costs in a few aircraft programs. Ensuring high-quality, defect-free aerospace composite production requires stringent process control and a highly skilled workforce, which can add operational complexity for manufacturers. Despite these challenges, the market outlook remains strong, supported by advancements in resin systems, the development of recyclable and bio-based composites, and the growing adoption of sustainable aviation practices. In the years ahead, the global aerospace composites market will be shaped by rising R&D investments, supportive government initiatives, and the industry's shift toward lighter, more efficient, and environmentally responsible materials. These factors will continue to drive market expansion and reinforce the strategic importance of composites in the future aerospace ecosystem.

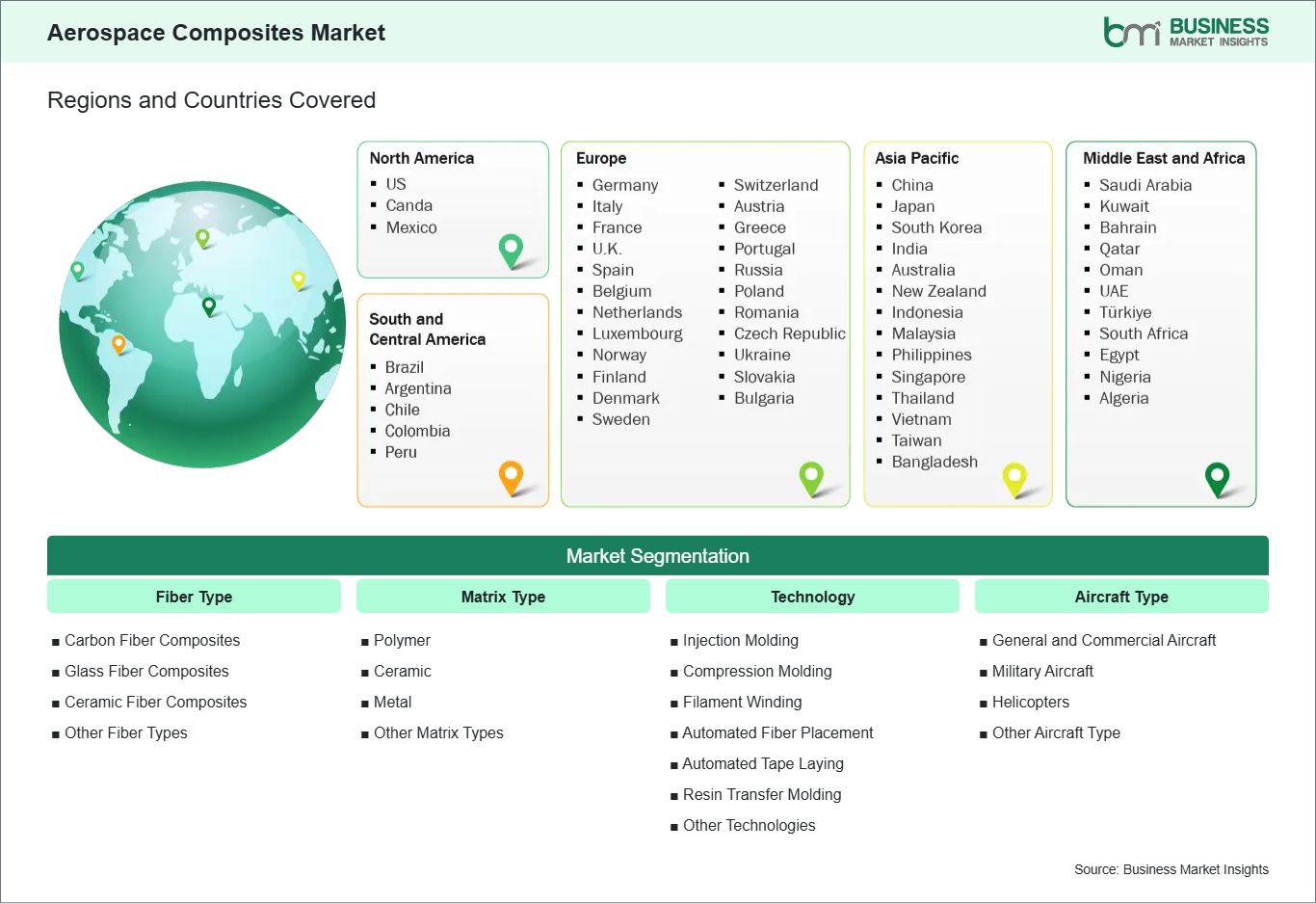

Key segments that contributed to the derivation of the aerospace composites market analysis are fiber type, matrix type, technology, aircraft type, and application.

By fiber type, the aerospace composites market is categorized into carbon fiber composites, glass fiber composites, ceramic fiber composites, and others. The carbon fiber composites segment dominated the market in 2025.

By matrix type, the market is segmented into polymer, ceramic, metal, and others. The polymer segment dominated the market in 2025.

By technology, the aerospace composites market is categorized into injection molding, compression molding, filament winding, automated fiber placement, automated tape laying, resin transfer molding, and others. The injection molding segment held the largest share of the market in 2025.

By aircraft type, the market is segmented into general and commercial aircraft, military aircraft, helicopters, and others. The commercial aircraft segment dominated the market in 2025.

By application, the aerospace composites market is categorized into cabin, seat, sandwich panels, engine, wings, rotor blades, tail boom, fuselage, and others. The wings segment held the largest share of the market in 2025.

Aerospace Composites Market Drivers and Opportunities:

Rising Aircraft Production and Demand for Lightweight Materials

Lightweight and high-strength materials are becoming crucial inputs in the aerospace sector so as to enhance fuel efficiency, emissions, and overall performance of the aircraft. Composite aerospace materials are widely used because of their high strength-to-weight ratio, fatigue, corrosion, and thermal stability, which makes aerospace composite materials ideal for the primary and secondary aircraft components. Increased air passenger traffic across the world has seen a rise in the production of commercial aircraft, and modernization efforts in the defense sector are also creating a demand to develop advanced military platforms, both of which are greatly increasing the utilization of composite materials. Aircraft manufacturers are also proactively substituting conventional metal with composites in the fuselage, the wings, interiors, and engine parts, in a bid to save on weight and operational costs. Also, tougher environmental policies and sustainability goals are driving airlines and OEMs towards investing in the design of fuel-efficient aircraft, which is further pushing the rapid adoption of composites. Sustained demand is also coming in the form of the expansion of the unmanned aerial vehicles, business jets, and next-generation air mobility solutions. With aerospace makers focusing on performance, durability, and lifecycle efficiency, aerospace composites are gaining immense traction across aviation and defense markets.

Advancement of Sustainable, Recyclable, and Next Generation Composite Technologies

Traditional aerospace composites face challenges related to recyclability, high production costs, and complex end-of-life processing. As a result, the industry is increasingly shifting toward sustainable alternatives such as recyclable thermoplastics, bio‑based resins, and hybrid advanced materials. These next-generation composites deliver comparable or superior performance while supporting material recovery and reducing environmental impact. The global push for sustainable aviation, circular‑economy principles, and carbon‑reduction goals is driving investment in low-waste manufacturing and eco-efficient material systems. Advances in automated production, resin infusion processes, and additive manufacturing are further improving efficiency, lowering scrap rates, and reducing overall costs.

Aerospace OEMs and suppliers are also partnering with research institutions and material innovators to accelerate the certification and commercialization of sustainable composite solutions. With regulatory bodies and customers placing greater emphasis on environmental responsibility, manufacturers adopting advanced, eco-friendly composite technologies are well-positioned to capture emerging opportunities, strengthen competitiveness, and support the long-term transformation of the aerospace composites market.

Aerospace Composites Market Size and Share Analysis:

The Aerospace Composites market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within fiber type, matrix type, technology, aircraft type, and application, offering insights into their contribution to overall market performance.

Based on fiber type, the carbon fiber composites subsegment dominates the aerospace composites market. Carbon fiber composites provide high strengths in weight-to-weight ratios, stiffness, fatigue, and thermal stability, which make it a key material in the primary structure of aircraft such as fuselages, wings, and empennage parts. Their successful experience in the harsh aerospace conditions and their capability to satisfy the rigorous safety and certification requirements have made them the choice of manufacturers in both commercial and military aircraft and space usage.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Solvay SA

Toray Advanced Composites

Collins Aerospace

Mitsubishi Chemical Group

Avient Corp

Ensinger GmbH

Materion Corporation

Spirit AeroSystems Inc

VX Aerospace Corporation

Adani Group

Get more information on this report

Aerospace Composites Market Report Coverage and Deliverables:

The " Aerospace Composites Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Aerospace Composites market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Aerospace Composites market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Aerospace Composites market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the aerospace composites market

Detailed company profiles, including SWOT analysis

Aerospace Composites Market Geographic Insights:

The geographical scope of the Aerospace Composites market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

The Asia Pacific Aerospace Composites Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia Pacific. Asia Pacific continues to record strong growth across key aerospace segments, including commercial aviation, defense, space exploration, and unmanned systems, securing its position as one of the fastest-expanding markets for aerospace composites. Rising aircraft production, increasing passenger traffic, and the demand for lightweight, fuel-efficient materials are further accelerating composite adoption to enhance performance and reduce emissions.

Ongoing industrialization, expanding aerospace manufacturing capabilities, and a greater focus on indigenous aircraft programs and advanced materials are strengthening the region's role in the global aerospace value chain. Collectively, these factors position Asia Pacific as both a major producer and a significant consumer of aerospace composites, reinforcing its strategic importance in the worldwide market.

Get more information on this report

Aerospace Composites Market Research Report Guidance:

The report includes qualitative and quantitative data in the Aerospace Composites market across fiber type, matrix type, technology, aircraft type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Aerospace Composites market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Aerospace Composites market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Aerospace Composites market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Aerospace Composites market segments by fiber type, matrix type, technology, aircraft type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Aerospace Composites market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Aerospace Composites Market News and Key Development:

The Aerospace Composites market is evaluated by gathering qualitative and quantitative data post-primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the aerospace composites market are:

In October 2025, BEML partnered with Kineco Ltd to advance composite manufacturing for defense and aerospace. This collaboration was formalized through a Memorandum of Understanding (MoU) exchanged in the presence of BEML CMD Shantanu Roy and Kineco Founder Shekhar Sardessai, along with senior officials from both organizations.

In June 2025, Toray Advanced Composites, Daher, and TARMAC Aerosave launched a joint End-of-Life Aerospace Recycling Program for commercial aircraft. In collaboration with Airbus, this initiative aims to enhance recycling technology practices by recovering and reusing secondary structural components made from continuous fiber-reinforced thermoplastic composites.

Key Sources Referred:

World Bank Global Trade IndicatorsEuropean Chemicals AgencyInternational Council of Chemical AssociationsInternational Monetary Fund (IMF)World Trade Organization (WTO)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Aerospace Composites Market

Solvay SA

Toray Advanced Composites

Collins Aerospace

Mitsubishi Chemical Group

Avient Corp

Ensinger GmbH

Materion Corporation

Spirit AeroSystems Inc

VX Aerospace Corporation

Adani Group

Frequently Asked Questions

How big is the Aerospace Composites Market?

The Aerospace Composites Market is valued at US$ 30.3 Billion in 2025, it is projected to reach US$ 91.57 Billion by 2033.

What is the CAGR for Aerospace Composites Market by (2026 - 2033)?

As per our report Aerospace Composites Market, the market size is valued at US$ 30.3 Billion in 2025, projecting it to reach US$ 91.57 Billion by 2033. This translates to a CAGR of approximately 14.83% during the forecast period.

What segments are covered in this report?

The Aerospace Composites Market report typically cover these key segments-

Fiber Type (Carbon Fiber Composites, Glass Fiber Composites, Ceramic Fiber Composites, and Other Fiber Types)

Matrix Type (Polymer, Ceramic, Metal, and Other Matrix Types)

Technology (Injection Molding, Compression Molding, Filament Winding, Automated Fiber Placement, Automated Tape Laying, Resin Transfer Molding, and Other Technologies)

Aircraft Type (General and Commercial Aircraft, Military Aircraft, Helicopters, and Other Aircraft Type)

What is the historic period, base year, and forecast period taken for Aerospace Composites Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Aerospace Composites Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Aerospace Composites Market?

The Aerospace Composites Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Solvay SA

Toray Advanced Composites

Collins Aerospace

Mitsubishi Chemical Group

Avient Corp

Ensinger GmbH

Materion Corporation

Spirit AeroSystems Inc

VX Aerospace Corporation

Adani Group

Who should buy this report?

The Aerospace Composites Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Aerospace Composites Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Aerospace Composites Market

Get Free Sample For Aerospace Composites Market