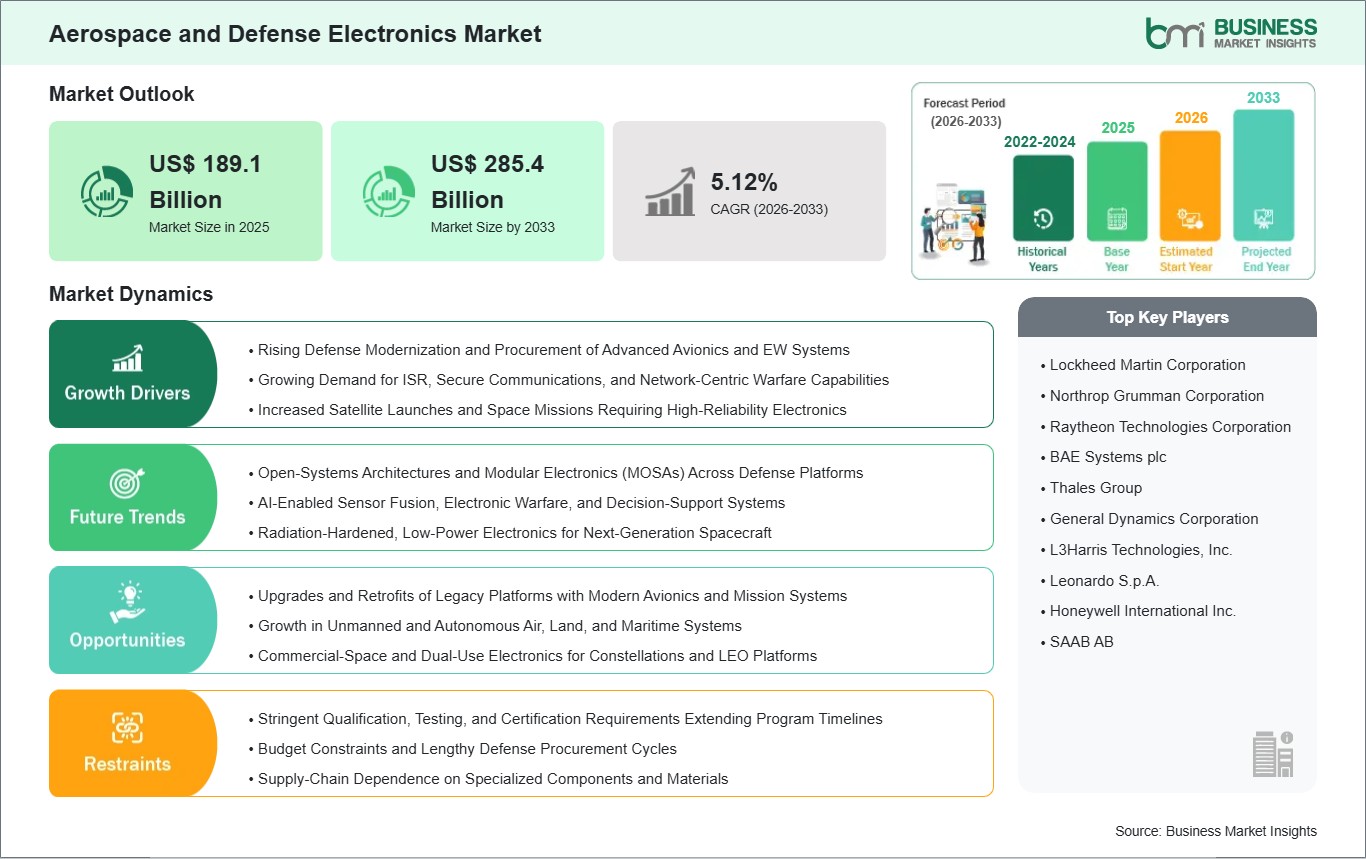

The Aerospace and Defense Electronics Market size is expected to reach US$ 285.4 Billion by 2033 from US$ 189.1 Billion in 2025. The market is estimated to record a CAGR of 5.28% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The aerospace and defense electronics market is the one that provides the systems that are vital for the functionalities of the aircraft such as avionics, communications, navigation, surveillance, electronic warfare, and onboard computing. The technology can be used for air, land, naval, and space platforms. These electronics provide the military with various capabilities such as situational awareness, precision targeting, secure data links, resilient command and control, and battle network integration, which in turn, makes them the core of military modernization and deterrence strategies globally. The market growth is a result of the rise in defense budgets in different parts of the world, the next generation fighters, rotorcraft, UAVs, and naval vessels that are procured in large quantities, and the increased use of intelligence, surveillance, and reconnaissance (ISR) assets in the areas that are likely to be contested.

Besides that, the space market, which is becoming more and more commercialized, the reduction in launch costs, and the increase in the number of satellite constellations in low Earth orbit are some of the factors that are giving a significant push to the demand for components that are resistant to radiation and have a high reliability as well as for the payload electronics. At the same time, there are issues such as strict qualification and certification standards, export controls, lengthy development and procurement cycles, and susceptibility to supply chain disruptions for specialized materials, semiconductors, and RF components that are making things difficult. However, there are also many opportunities in the future in the form of various projects on open systems architectures, AI enabled sensor fusion, electronic warfare upgrades, cyber resilient avionics, and life extension of legacy platforms for the suppliers of advanced aerospace and defense electronic systems.

Aerospace and Defense Electronics Market - Strategic Insights:

Get more information on this report

Aerospace and Defense Electronics Market Segmentation Analysis:

Key segments that contributed to the derivation of the Aerospace and Defense Electronics market analysis are component, application, platform, and sales channel.

By component, the aerospace and defense electronics market is segmented into sensors, communication systems, electronic warfare, navigation systems, power electronics, and others. The sensors segment accounted for the largest share of the market in 2024.

By application, the market is segmented into military, commercial, space, and homeland security. The military segment held the largest share of the market in 2024.

By platform, the market is segmented into airborne, land, naval, and space. The airborne segment held the largest share of the market in 2024.

By sales channel, the market is segmented into OEM and aftermarket. The OEM segment accounted for the largest share of the market in 2024.

Aerospace and Defense Electronics Market Drivers and Opportunities:

Defense Modernization and Multi‑Domain Operations

The aerospace and defense electronics market is mainly influenced by the defense sector modernization and the growing importance of multi, domain operations. To confront complex threats and harsh environments, the military is outfitting their vehicles with the latest avionics, mission computers, sensors, communications, and electronic warfare (EW) systems.

Next, generation fighters, bombers, helicopters, UAVs, and naval platforms are just some of the ways integrated radar, EO/IR payloads, secure datalinks, navigation, and electronic support measures are making the technology per platform significantly more advanced. ISR capabilities persistent surveillance, signals intelligence, and space, based observation are becoming more comprehensive, thus increasing the need for high, performance processing, RF components, and payload electronics.

In addition, several countries have made the decision to either replace or upgrade their fleet of the old aircraft and ships thus creating retrofit programs that mainly involve the overhaul of avionics and mission systems. Meanwhile, regional matters such as heightened geopolitical tensions and defense budgets in areas like Asia, Pacific and Eastern Europe are acting as a confirmation of this trend, thus leading to the creation of a solid pipeline of procurement and R&D programs for aerospace and defense electronics suppliers.

Open Architectures and Expanding Space Sector

A major opportunity is in open, systems architectures and widening demand in the space sector. To reduce vendor lock, in, enable faster upgrades, and lower lifecycle costs, defense ministries are increasingly mandating modular open systems (MOSA). The change is advantageous to those suppliers who make standards, based cards, backplanes, and software frameworks compatible with such initiatives as SOSA and FACE, thus facilitating the integration of new capabilities into the existing platforms. simultaneously, commercial and military space markets are booming rapidly, with small satellite constellations in low Earth orbit for communications, navigation augmentation, and Earth observation. Such satellites need radiation, tolerant processors, power, management ICs, RF front, ends, and payload electronics that can withstand the harsh environment and at the same time provide high throughput. The rising use of on, orbit processing, space situational awareness, and in, space manufacturing will thus considerably increase the demand for advanced electronics. The suppliers who integrate ruggedized hardware, AI, enabled sensor fusion, cybersecurity, and lifecycle support services are able to secure multi, year upgrade contracts across air, land, naval, and space platforms, thus positioning themselves as strategic partners in the transition to agile, software, reconfigurable defense systems.

Aerospace and Defense Electronics Market Size and Share Analysis:

Based on component, the aerospace and defense electronics market is divided into the following: sensors, communication systems, electronic warfare, navigation systems, power electronics, and others. The sensors segment dominated the market share in 2024. Sensors may include radar, EO/IR, acoustic, and electronic, support sensors, which are essential for surveillance, targeting, threat detection, and situational awareness in air, land, naval, and space platforms, and are continuously being enhanced as resolution and range requirements keep increasing.

The application, wise market is segmented into military, commercial, space, and homeland security. The military segment accounted for the largest share of the market in 2024. As a result of modernization programs and rising geopolitical tensions, defense forces are investing heavily in avionics, mission computers, communications, and electronic, warfare systems for fighters, UAVs, armored vehicles, and naval vessels.

The platform, wise market is segmented into airborne, land, naval, and space. The airborne segment was the largest shareholder of the market in 2024. In order to meet the demands of combat and transport aircraft, helicopters, and UAVs, which require extensive avionics suites, ISR payloads, and EW equipment, there has been a high electronic content per platform as well as frequent upgrade cycles.

The market is segmented by sales channel into OEM and aftermarket. In 2024, the OEM segment held the major part of the market as the majority of advanced electronics are integrated during the initial platform development and production, while the prime contractors source the mission critical systems from the specialized electronics suppliers.

Aerospace and Defense Electronics Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Lockheed Martin Corporation

Northrop Grumman Corporation

Raytheon Technologies Corporation

BAE Systems plc

Thales Group

General Dynamics Corporation

L3Harris Technologies, Inc.

Leonardo S.p.A.

Honeywell International Inc.

SAAB AB

Get more information on this report

Aerospace and Defense Electronics Market Report Coverage and Deliverables:

The Aerospace and Defense Electronics Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

Aerospace and defense electronics market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Aerospace and defense electronics market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Aerospace and defense electronics market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Aerospace and defense electronics market

Detailed company profiles, including SWOT analysis

Aerospace and Defense Electronics Market Geographic Insights:

The geographical scope of the aerospace and defense electronic market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Asia-Pacific Aerospace and defense electronics market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia.

Asia Pacific is emerging as a key growth engine as countries such as China, India, Japan, South Korea, and Australia increase defense spending and focus on indigenous capability. Programs to acquire or develop next‑generation fighters, UAVs, submarines, and air‑defense systems drive requirements for radar, EO/IR payloads, data links, and electronic‑support measures. Europe remains important through collaborative platforms like Eurofighter and A400M and strong aerospace industries across France, Germany, the UK, and Italy. The Middle East invests heavily in air‑defense, ISR, and C4ISR systems, often sourcing from US and European suppliers but increasingly considering local offsets. Latin America has smaller budgets but ongoing needs for surveillance, border security, and transport aircraft upgrades, supporting selective avionics and mission‑system modernization. Across all regions, new commercial‑space initiatives and sovereign satellite programs are adding demand for radiation‑tolerant electronics and payload systems.

Get more information on this report

Aerospace and Defense Electronics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Aerospace and defense electronics market across component, application, platform, and sales channel, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Aerospace and defense electronics market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Aerospace and defense electronics market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Aerospace and defense electronics market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover Aerospace and defense electronics market segments by component, application, platform, and sales channel, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Aerospace and defense electronics market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Aerospace and Defense Electronics Market News and Key Development:

The aerospace and defense electronics market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the aerospace and defense electronics market are:

In September 2025, Safran Electronics & Defense, a leading European high-technology company in aerospace and defense, and Polska Grupa Zbrojeniowa S.A. (PGZ), Poland’s primary defense industry leader, have signed two Memorandums of Understanding (MoU) to further expand their collaboration in support of European security and industrial cooperation during the International Defense Industry Exhibition (MSPO) held in Kielce.

In September 2025, Hanwha Aerospace has signed a contract with BAE Systems to integrate next-generation, anti-jamming Global Positioning System (GPS) technology into Hanwha Aerospace’s Deep Strike Capability precision-guided weapon system. This contract brings the two aerospace and defense technology companies together to collaborate in the critical field of advanced guidance technology. The collaboration will leverage BAE Systems’ world-renowned expertise in military GPS and anti-jamming solutions to counter sophisticated electronic warfare threats.

Key Sources Referred:

Aerospace Industries AssociationAFCEA InternationalAIAAInternational Energy Agency World Bank – Global Trade Indicators World Trade Organization (WTO) International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Aerospace and Defense Electronics Market

Lockheed Martin Corporation

Northrop Grumman Corporation

Raytheon Technologies Corporation

BAE Systems plc

Thales Group

General Dynamics Corporation

L3Harris Technologies, Inc.

Leonardo S.p.A.

Honeywell International Inc.

SAAB AB

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Aerospace and Defense Electronics Market?

The Aerospace and Defense Electronics Market is valued at US$ 189.1 Billion in 2025, it is projected to reach US$ 285.4 Billion by 2033.

What is the CAGR for Aerospace and Defense Electronics Market by (2026 - 2033)?

As per our report Aerospace and Defense Electronics Market, the market size is valued at US$ 189.1 Billion in 2025, projecting it to reach US$ 285.4 Billion by 2033. This translates to a CAGR of approximately 5.28% during the forecast period.

What segments are covered in this report?

The Aerospace and Defense Electronics Market report typically cover these key segments-

Component (Sensors, Communication Systems, Electronic Warfare, Navigation Systems, Power Electronics, and Others)

Application (Military, Commercial, Space, and Homeland Security)

Platform (Airborne, Land, Naval, and Space)

Sales Channel (OEM, Aftermarket)

What is the historic period, base year, and forecast period taken for Aerospace and Defense Electronics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Aerospace and Defense Electronics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Aerospace and Defense Electronics Market?

The Aerospace and Defense Electronics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lockheed Martin Corporation

Northrop Grumman Corporation

Raytheon Technologies Corporation

BAE Systems plc

Thales Group

General Dynamics Corporation

L3Harris Technologies, Inc.

Leonardo S.p.A.

Honeywell International Inc.

SAAB AB

Who should buy this report?

The Aerospace and Defense Electronics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Aerospace and Defense Electronics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Aerospace and Defense Electronics Market

Get Free Sample For Aerospace and Defense Electronics Market