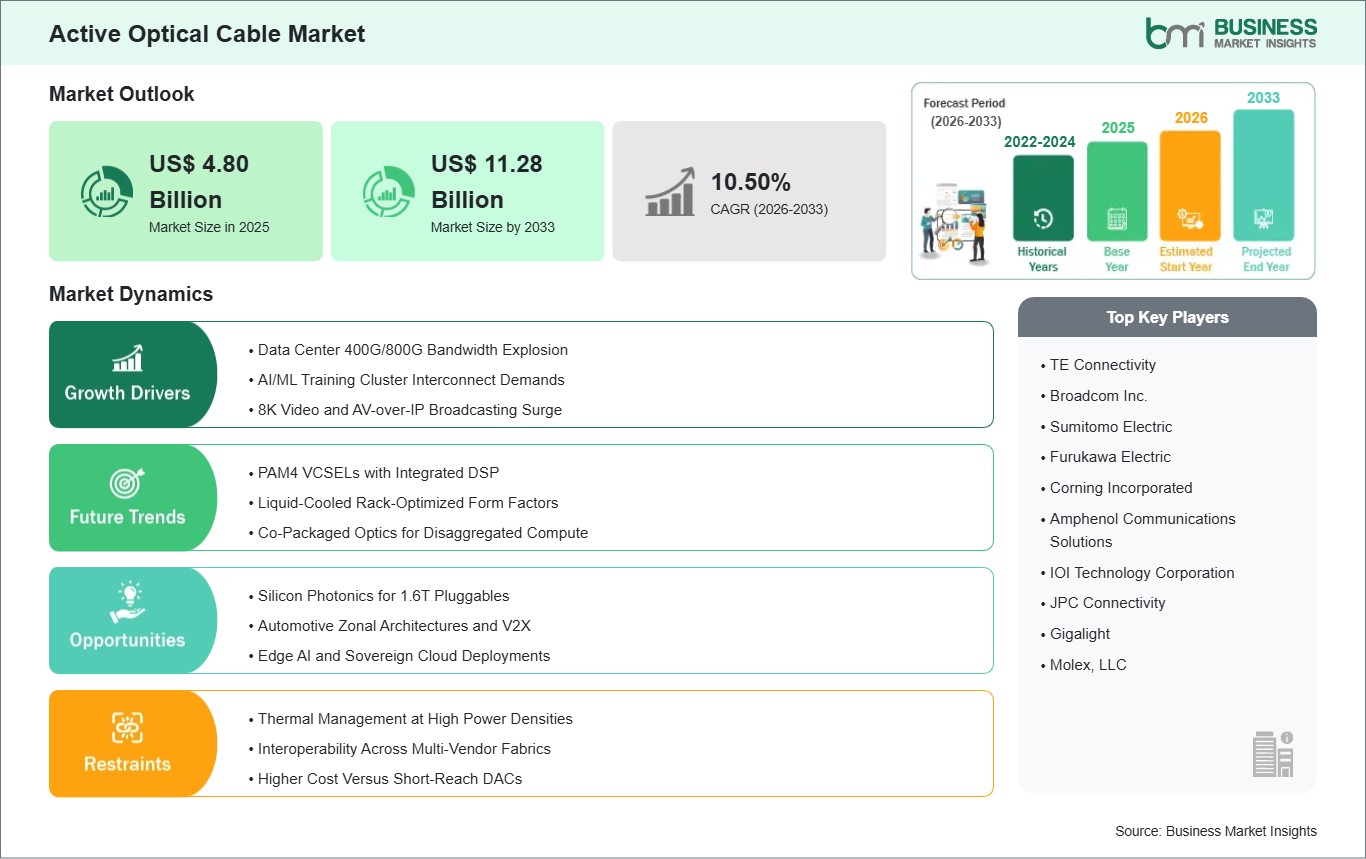

The Active Optical Cable Market size is expected to reach US$ 11.28 Billion by 2033 from US$ 4.80 Billion in 2025. The market is estimated to record a CAGR of 11.27% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global active optical cable market leverages integrated optical engines and multimode fibers to facilitate fast data transmission for bandwidth, heavy applications. These cables come with lasers, VCSELs, and transceivers enabling 100G+ speeds over the distances that copper cannot. Hence, data center, 8K display, and 5G fronthaul connectivity’s are performed at low latency. Among the most significant benefits are EMI immunity, 70% weight reduction when compared to DACs, and plug and play simplicity, which position AOCs as a must, have for AI clusters, hyperscale clouds, and immersive AV ecosystems.

A solid increase accompanies the 400G/800G ramps, edge computing spreading, and AV, over, IP broadcasting as the volume of unstructured data is skyrocketing. The main drivers are data center expansions by AWS and Alibaba, along with 4K/8K TV penetration, while the scaling of the fab reduces the cost of VCSELs. On the downside, thermal management at 100W+ and interoperability standards are among the problems that the industry is currently facing. Beyond that, there exist tremendous opportunities for silicon photonics integration, 1.6T AOCs, and automotive infotainment networks.

Active Optical Cable Market - Strategic Insights:

Get more information on this report

Active Optical Cable Market Segmentation Analysis:

Key segments shaping the global active optical cable market include technology, application, connector type, and transmission distance.

By technology, the market segments into InfiniBand, Ethernet, HDMI, DisplayPort, USB, and Others. The Ethernet segment dominated in 2024, optimized for cloud-scale networking.

By application, divisions cover Data Center, High-Performance Computing, Consumer Electronics, Telecommunications, and Broadcasting. The Data Center segment led in 2024, fueling AI training clusters.

By connector type, segments are SFP, QSFP, CXP, SFP+, and CFP. The QSFP segment held the top share in 2024, supporting 40G/100G breakouts.

By transmission distance, categories include Up to 30 meters, Up to 100 meters, Up to 300 meters, Up to 500 meters. The Up to 100 meters segment topped in 2024, suiting rack-to-rack links.

Active Optical Cable Market Drivers and Opportunities:

Data Center Hyperscale Expansion Powers Bandwidth Surge

The active optical cables segment is being driven by hyperscale data center builds on an explosive scale and AI accelerator deployments, as operators are focused on low-power, high-density 400G+ interconnects. Credo and MaxLinear QSFP, DD AOCs connect NVIDIA DGX clusters with NVLink switches; thus, they achieve latency within the sub-100ns range across 100m spans, which is very critical for trillion-parameter LLMs. Due to Asia-Pacific colocation regulations, there will be a 25% annual port upgrade rate alongside a backlog of over 5M units by 2030.

With the aid of CHIPS Act subsidies, US local fabs are closing the gap, thus mixing Ethernet AOCs with InfiniBand for GPU, direct storage in contested semiconductor supply chains. PAM4 VCSELs work perfectly well under 70 °C server farm conditions, whereas upgrading from the old CX4/DAC to the retrofitted ones quickly opens up profit possibilities; therefore, positioning AOCs as zero-touch fabric facilitators to handle exabytes, scale operations, liquid-cooled racks, and sustainable PUE targets below 1.2.

The Ukrainian energy crises further unveil the ground realities of energy crises and hence revolves around the issue of urgent grid stability. Hybrid SAW arrays, through the combination of humidity, pressure, and vibration sensors, help ensure pipeline integrity, thereby, leakages in the pipelines used for transporting gas in the regions that are under the control of adversaries are prevented. Gallium Nitride (GaN) based transducers are pretty much at home in the high electromagnetic interference (EMI) environments such as those created by electric arc furnaces, where they turn out signal, to, noise ratios of above 30% compared to the standard quartz crystals.

8K Broadcasting and Automotive Cockpits Unlock New Horizons

HDMI/DisplayPort AOCs are presupposed to be the main beneficiaries of the 8K broadcasting and automotive cockpit networks, reopening the entry of an entirely new world of applications in stadium LED walls and zonal architectures. Open standards have enabled QSFP AOCs to be fused with AVB for remote production, which in turn has resulted in a reduction of venue cabling by 60% when compared to copper HDBaseT for FIFA/Super Bowl streams. Mandates from consumer electronics, such as EU energy labelling, have increased the market for USB4 optical extenders under $20/meter. In contrast, Level 3+ autonomy has been the reason for 100G CFP links for LiDAR fusion costing less than $100/unit. Silicon photonics brings the dimension of chips down to 0.5mm, leading to a decrease in BOMs by 50% for edge AI gateways. Broadcasting verticals take advantage of CXP in 12G, SDI trucks following 360 UHD, R, being in line with SMPTE 2110. Such dynamics are setting the stage for suppliers to secure contracts worth $15B through 2034, with AOCs turning into pluggable hubs for disaggregated computing and immersive realities.

Active Optical Cable Market Size and Share Analysis:

By technology, the global active optical cable market segments into InfiniBand, Ethernet, HDMI, DisplayPort, USB, and Others. The Ethernet segment dominated in 2024. Powers 90% cloud traffic; PAM4 scalability drives hyperscaler adoption across 400G fabrics.

By application, segments are Data Center, High-Performance Computing, Consumer Electronics, Telecommunications, and Broadcasting. The Data Center segment led in 2024. Consumes 70% bandwidth; AI/ML workloads demand massive server-to-server interconnect scaling.

By connector type, divisions include SFP, QSFP, CXP, SFP+, and CFP. The QSFP segment held the largest share in 2024. Versatile 40G/100G/400G support enables seamless rack-scale fabric migrations globally.

By transmission distance, categories are Up to 30 meters, Up to 100 meters, Up to 300 meters, Up to 500 meters. The Up to 100 meters segment topped in 2024. Matches intra-data center rack-to-rack spans in mega-scale deployments.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

TE Connectivity

Broadcom Inc.

Sumitomo Electric

Furukawa Electric

Corning Incorporated

Amphenol Communications Solutions

IOI Technology Corporation

JPC Connectivity

Gigalight

Molex, LLC

Get more information on this report

Active Optical Cable Market Report Coverage and Deliverables:

The "Active Optical Cable Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Active optical cable market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Active optical cable market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Active optical cable market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Active optical cable market

Detailed company profiles, including SWOT analysis

Active Optical Cable Market Geographic Insights:

The geographical scope of the active optical cable market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. The active optical cable market in North America registered the highest market share in 2024.

North America is leading through the three giant public cloud providers and AI research labs, divided among the US, Canada, and Mexico. Deployments in the US are booming with 800G QSFP, DD AOCs powering xAI's Memphis superclusters and AWS Snowball Edge expansions enabling tactical edge AI. In contrast, Canadian hyperscalers like Equinix incorporate 400G Ethernet for ML training pipelines. Mexico's maquiladora electronics manufacturing uses USB 3.2 AOCs to scale a Tier 1 automotive supplier.

Europe has made great progress with GDPR compliant Ethernet fabrics and green data center directives, partly by Germany's Nokia and Infineon developing QSFP28 for the industrial edge, and alongside the UK's broadcast CXP adoption for BBC 8K OB trucks as well as Pinewood Studios virtual production. OVHcloud of France is focusing on low-power DisplayPort AOCs for sovereign AI. The Middle East is fiercely building sovereign clouds, as is the case of Saudi Arabia's stc deploying QSFP InfiniBand for NEOM's smart city backbone and the UAE's du integrating CFP2 for 5G XHaul aggregation.

Asia Pacific is booming through China's 6G field trials and national chip ambitions, with Alibaba Cloud employing 1.6T Ethernet AOCs. Meanwhile, India's Jio and Reliance are constructing 10EF data centers with cost-efficient USB4 optical extenders, but they are still behind the Western markets in advanced CFP2 pluggables due to fab maturity gaps. South and Central America are also registering market growth during the forecast period.

Get more information on this report

Active Optical Cable Market Research Report Guidance:

The report includes qualitative and quantitative data in the Active optical cable market across technology, application, connector type, transmission distance, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Active optical cable market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Active optical cable market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the active optical cable market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover active optical cable market segments by technology, application, connector type, transmission distance, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Active optical cable market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Active Optical Cable Market News and Key Development:

The active optical cable market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the active optical cable market are:

In April 2025, Sumitomo Electric will present a variety of next-generation interface cables, including Thunderbolt™5 cables compatible with the latest high-speed transmission standard; active optical cables using optical fibers that support long-distance transmission; and DP80 active cables that are compatible with various devices adopting transmission standards, including DisplayPort connectors and Type-C connectors.

In January 2025, Other World Computing, Inc. launched the New Superlong 40Gb/s OWC Active Optical Cable. The new cable delivers supreme flexibility to consumers' workspaces. With full support for Thunderbolt 4/3 and USB4/3/2 devices, the Active Optical Cable provides up to 40Gb/s of stable bandwidth, up to 240W of power delivery, and up to 8K video resolution. But it's not just speed and power delivery that make this cable special.

Key Sources Referred:

IEEE Communications SocietyInfiniBand Trade AssociationPCI-SIGInternational Energy AgencyWorld Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Trade Administration (ITA)Company websitesCompany annual reportsCompany investor presentations

The List of Companies - Active Optical Cable Market

TE Connectivity

Broadcom Inc.

Sumitomo Electric

Furukawa Electric

Corning Incorporated

Amphenol Communications Solutions

IOI Technology Corporation

JPC Connectivity

Gigalight

Molex, LLC

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Active Optical Cable Market?

The Active Optical Cable Market is valued at US$ 4.80 Billion in 2025, it is projected to reach US$ 11.28 Billion by 2033.

What is the CAGR for Active Optical Cable Market by (2026 - 2033)?

As per our report Active Optical Cable Market, the market size is valued at US$ 4.80 Billion in 2025, projecting it to reach US$ 11.28 Billion by 2033. This translates to a CAGR of approximately 11.27% during the forecast period.

What segments are covered in this report?

The Active Optical Cable Market report typically cover these key segments-

Technology (InfiniBand, Ethernet, HDMI, DisplayPort, USB, Other Technology)

Application (Data Center, High-Performance Computing, Consumer Electronics, Telecommunications, Broadcasting)

Connector Type (SFP, QSFP, CXP, SFP+, CFP)

Transmission Distance (Up to 30 meters, Up to 100 meters, Up to 300 meters, Up to 500 meters)

What is the historic period, base year, and forecast period taken for Active Optical Cable Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Active Optical Cable Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Active Optical Cable Market?

The Active Optical Cable Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

TE Connectivity

Broadcom Inc.

Sumitomo Electric

Furukawa Electric

Corning Incorporated

Amphenol Communications Solutions

IOI Technology Corporation

JPC Connectivity

Gigalight

Molex, LLC

Who should buy this report?

The Active Optical Cable Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Active Optical Cable Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Active Optical Cable Market

Get Free Sample For Active Optical Cable Market