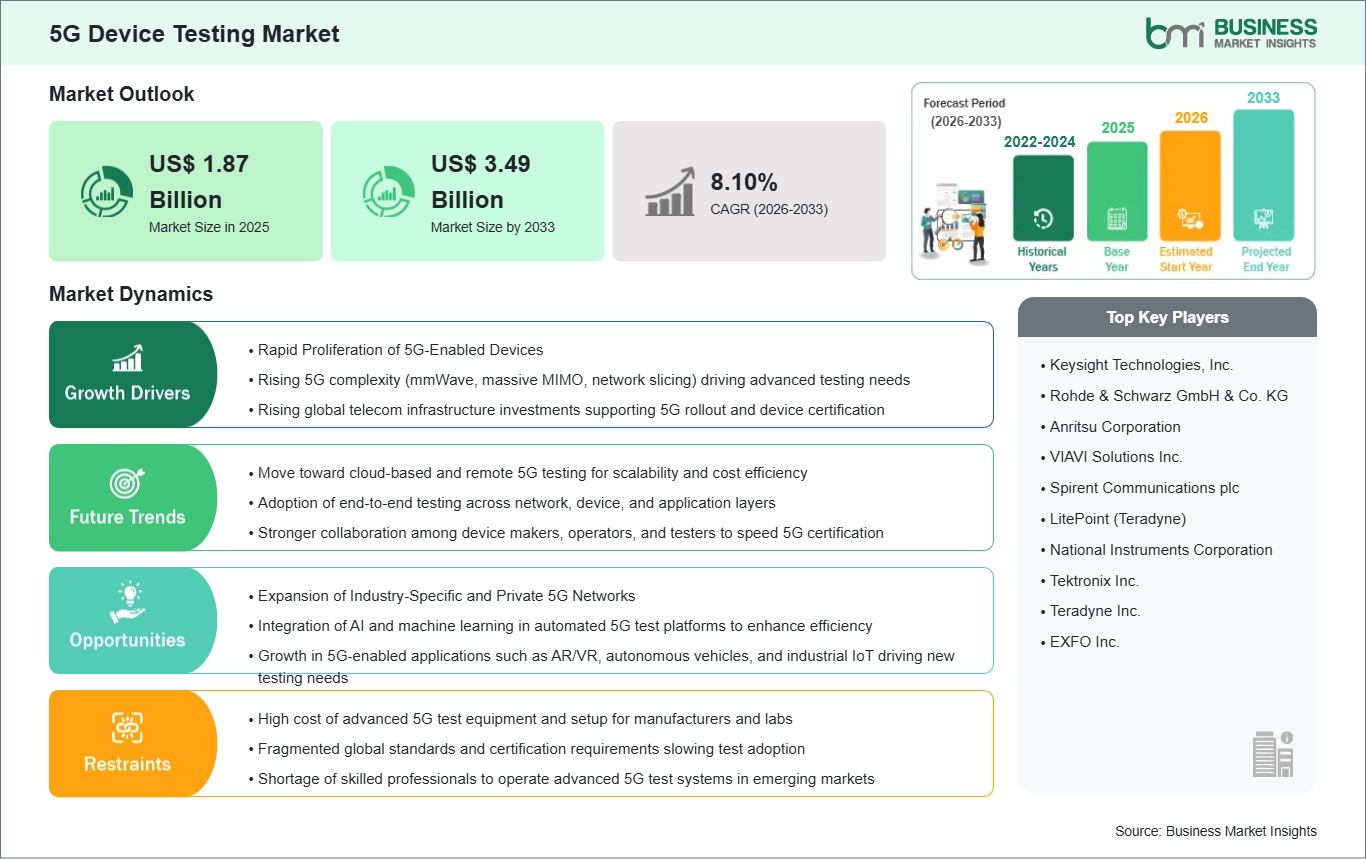

The 5G Device Testing Market size is expected to reach US$ 3.49 Billion by 2033 from US$ 1.87 Billion in 2025. The market is estimated to record a CAGR of 8.11% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The 5G Device Testing market is a critical enabler of the global transition toward reliable, high-performance, and interoperable 5G ecosystems. As 5G adoption accelerates across consumer electronics, industrial IoT, automotive, healthcare, and enterprise applications, device testing plays a central role in ensuring performance, compliance, and seamless connectivity. Advanced testing solutions enable real-time validation of device functionality, latency, throughput, and spectrum efficiency, supporting the successful deployment of next-generation wireless technologies. By leveraging automation, AI-driven analytics, and digital testing platforms, manufacturers and network operators can significantly reduce time-to-market while ensuring quality, reliability, and regulatory adherence.

5G Device Testing solutions are at the core of managing the increasing complexity of multi-band, multi-mode, and multi-standard devices. They support the validation of critical features such as massive MIMO, beamforming, network slicing, and ultra-low latency communication. As device ecosystems expand and usage scenarios become more diverse, robust testing frameworks enable stable network performance, improved user experience, and scalable deployment across global markets.

Several factors are driving the growth of the 5G Device Testing market, including the rapid rollout of 5G infrastructure, the rising penetration of 5G-enabled smartphones and IoT devices, and stringent regulatory and certification requirements. Additionally, the expansion of vertical use cases—such as autonomous vehicles, smart manufacturing, and mission-critical communications—has increased demand for comprehensive testing across the device lifecycle. Continuous advancements in test automation, cloud-based testing platforms, over-the-air (OTA) testing, and AI-assisted diagnostics are further accelerating market adoption by improving efficiency and reducing operational costs.

Despite its strong growth potential, the market faces challenges such as high initial investment requirements for advanced testing equipment, complexity in validating devices across diverse global standards, and integration issues with legacy testing systems. Cybersecurity risks associated with connected devices and test environments also raise concerns for manufacturers and service providers. Moreover, a shortage of skilled professionals with expertise in 5G protocols, RF engineering, and advanced test methodologies, along with evolving and fragmented regulatory frameworks, can slow deployment and increase compliance complexity. Standardization and interoperability across device platforms and test solutions remain key hurdles that vendors must address to ensure scalable and cost-effective implementation.

5G Device Testing Market - Strategic Insights:

Get more information on this report

5G Device Testing Market Segmentation Analysis:

Key segments that contributed to the derivation of the 5G Device Testing market analysis are equipment type, and end user.

By equipment type, the 5G Device Testing market is divided into Oscilloscopes, Signal Generators, Spectrum Analyzers, Network Analyzers, and Others. The oscilloscopes segment dominated the market in 2024.

By equipment type, the 5G Device Testing market is divided into Oscilloscopes, Signal Generators, Spectrum Analyzers, Network Analyzers, and Others. The oscilloscopes segment dominated the market in 2024.

5G Device Testing Market Drivers and Opportunities:

Rapid Proliferation of 5G-Enabled Devices

The accelerating adoption of 5G-enabled devices across consumer, enterprise, and industrial segments is a primary driver of the 5G Device Testing market. Smartphones, wearables, connected vehicles, industrial sensors, and mission-critical IoT devices are increasingly being deployed with complex 5G capabilities, including multi-band operation, massive MIMO, beamforming, and ultra-low latency communication. This growing device diversity significantly increases testing requirements across the entire product lifecycle, from design validation and conformance testing to certification and post-deployment performance assurance.

Manufacturers and network operators face mounting pressure to ensure device interoperability, regulatory compliance, and consistent user experience across different geographies and network configurations. Any performance degradation or compliance failure can lead to costly recalls, delayed launches, or reputational damage. As a result, demand for advanced, automated, and scalable 5G device testing solutions has intensified. Additionally, shorter product development cycles and intense market competition have made testing a strategic function rather than a purely technical requirement. Businesses are investing in sophisticated testing platforms to reduce time-to-market, optimize development costs, and mitigate operational risks, thereby directly driving sustained growth in the 5G Device Testing market.

Expansion of Industry-Specific and Private 5G Networks

The rapid emergence of industry-specific applications and private 5G networks presents a significant growth opportunity for the 5G Device Testing market. Industries such as manufacturing, logistics, healthcare, energy, and transportation are increasingly deploying private 5G networks to support automation, real-time monitoring, and mission-critical operations. These environments demand highly customized devices and network configurations, creating a strong need for specialized testing solutions tailored to specific performance, latency, security, and reliability requirements.Unlike traditional consumer devices, enterprise and industrial 5G devices must operate in complex, interference-prone, and safety-critical settings. This increases the importance of rigorous testing for use cases such as autonomous robotics, remote surgery, smart factories, and connected infrastructure. Testing providers that can offer end-to-end validation—including over-the-air (OTA) testing, cybersecurity assessment, and application-level performance testing—are well positioned to capture new revenue streams.

Furthermore, as enterprises lack in-house 5G testing expertise, they are more inclined to outsource testing services, creating opportunities for testing-as-a-service and managed solutions. Vendors that align their offerings with industry-specific standards and regulatory requirements can establish long-term partnerships, making vertical and private 5G deployments a high-growth opportunity within the broader 5G Device Testing market.

5G Device Testing Market Size and Share Analysis:

By equipment type, the 5G Device Testing market is segmented into Oscilloscopes, Signal Generators, Spectrum Analyzers, Network Analyzers, and Others, each serving a distinct role across the device development and validation lifecycle. Among these, the oscilloscopes segment dominated the market in 2024, driven by their extensive use in high-speed signal integrity analysis and time-domain measurements.

By end user, the market is bifurcated into Integrated Device Manufacturers (IDMs) & Original Design Manufacturers (ODMs) and Telecom Equipment Manufacturers. In 2024, Telecom Equipment Manufacturers accounted for the larger market share, reflecting their central role in the 5G ecosystem. These players are responsible for developing and deploying core network equipment, base stations, and user devices that must operate seamlessly across diverse network environments.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Keysight Technologies, Inc.

Rohde & Schwarz GmbH & Co. KG

Anritsu Corporation

VIAVI Solutions Inc.

Spirent Communications plc

LitePoint (Teradyne)

National Instruments Corporation

Tektronix Inc.

Teradyne Inc.

EXFO Inc.

Get more information on this report

5G Device Testing Market Report Coverage and Deliverables:

The "5G Device Testing Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

5G Device Testing market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

5G Device Testing market trends, as well as market dynamics such as drivers, restraints, and key opportunities

5G Device Testing market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the 5G Device Testing market

Detailed company profiles, including SWOT analysis

5G Device Testing Market Geographic Insights:

The 5G Device Testing market is geographically segmented into North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. Among these regions, Asia Pacific is expected to witness the strongest growth and remain the dominant market throughout the forecast period, supported by rapid digital transformation, expanding electronics manufacturing ecosystems, and early adoption of advanced wireless technologies. The region benefits from large-scale production capabilities, strong demand for 5G-enabled devices, and continuous investments in next-generation communication infrastructure.

Within Asia Pacific, the market spans China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. Growth in this region is underpinned by robust semiconductor and electronics manufacturing output, significant investments in 5G infrastructure, and government-backed initiatives aimed at accelerating digitalization and smart manufacturing. Leading economies such as China, Japan, South Korea, and India are at the forefront of deploying advanced 5G testing solutions, driven by large-scale smartphone production, IoT device development, and expanding telecom equipment manufacturing. These countries are also integrating AI-driven analytics, automation, cloud-based testing platforms, and over-the-air (OTA) testing methodologies to enhance product quality, interoperability, and time-to-market.

Demand for 5G Device Testing in Asia Pacific is further fueled by key end-use industries including consumer electronics, automotive and connected mobility, industrial automation, healthcare devices, and telecommunications. Rising investments in high-volume manufacturing facilities, device certification labs, and compliance testing infrastructure are accelerating market expansion. Additionally, public–private partnerships, regulatory support, and skills development programs focused on advanced RF and 5G technologies are strengthening the regional ecosystem.

Get more information on this report

5G Device Testing Market Research Report Guidance:

The report includes qualitative and quantitative data in the 5G Device Testing market across component, control type, system, implementation type and end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the 5G Device Testing market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the 5G Device Testing market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the 5G Device Testing market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover 5G Device Testing market segments by equipment type, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the 5G Device Testing market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer

5G Device Testing Market News and Key Development:

The 5G Device Testing market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the 5G Device Testing market are:

In January 2026, Airbus UpNext, a wholly-owned subsidiary of Airbus, launched a new demonstrator called Airbus UpNext SpaceRAN (Space Radio Access Network). Its mission is to enable standardised global connectivity by exploring advanced 5G Non-Terrestrial Network (NTN) capabilities.

In July 2025, ANRITSU CORPORATION developed and launched new software options for its Radio Communication Test Station MT8000A, designed to evaluate the radio frequency (RF) performance of 5G devices such as smartphones. These options support key technologies specified in 3GPP Release 17, including 1024QAM modulation for downlink and Tx Switching 2Tx to 2Tx for uplink, enabling accurate and flexible evaluation of 5G devices with enhanced transmit/receive (TRx) performance.

Key Sources Referred:

International Telecommunication Union (ITU)3rd Generation Partnership Project (3GPP)Institute of Electrical and Electronics Engineers (IEEE)Federal Communications Commission (FCC) and other national regulatory authoritiesEuropean Telecommunications Standards Institute (ETSI)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - 5G Device Testing Market

Keysight Technologies, Inc.

Rohde & Schwarz GmbH & Co. KG

Anritsu Corporation

VIAVI Solutions Inc.

Spirent Communications plc

LitePoint (Teradyne)

National Instruments Corporation

Tektronix Inc.

Teradyne Inc.

EXFO Inc.

Frequently Asked Questions

How big is the 5G Device Testing Market?

The 5G Device Testing Market is valued at US$ 1.87 Billion in 2025, it is projected to reach US$ 3.49 Billion by 2033.

What is the CAGR for 5G Device Testing Market by (2026 - 2033)?

As per our report 5G Device Testing Market, the market size is valued at US$ 1.87 Billion in 2025, projecting it to reach US$ 3.49 Billion by 2033. This translates to a CAGR of approximately 8.11% during the forecast period.

What segments are covered in this report?

The 5G Device Testing Market report typically cover these key segments-

Equipment Type (Oscilloscopes, Signal Generators, Spectrum Analyzers, Network Analyzers, and Others)

End User (IDMs & ODMs, and Telecom Equipment Manufacturer)

What is the historic period, base year, and forecast period taken for 5G Device Testing Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the 5G Device Testing Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in 5G Device Testing Market?

The 5G Device Testing Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Keysight Technologies, Inc.

Rohde & Schwarz GmbH & Co. KG

Anritsu Corporation

VIAVI Solutions Inc.

Spirent Communications plc

LitePoint (Teradyne)

National Instruments Corporation

Tektronix Inc.

Teradyne Inc.

EXFO Inc.

Who should buy this report?

The 5G Device Testing Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the 5G Device Testing Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For 5G Device Testing Market

Get Free Sample For 5G Device Testing Market