Blood Pressure Monitors Market

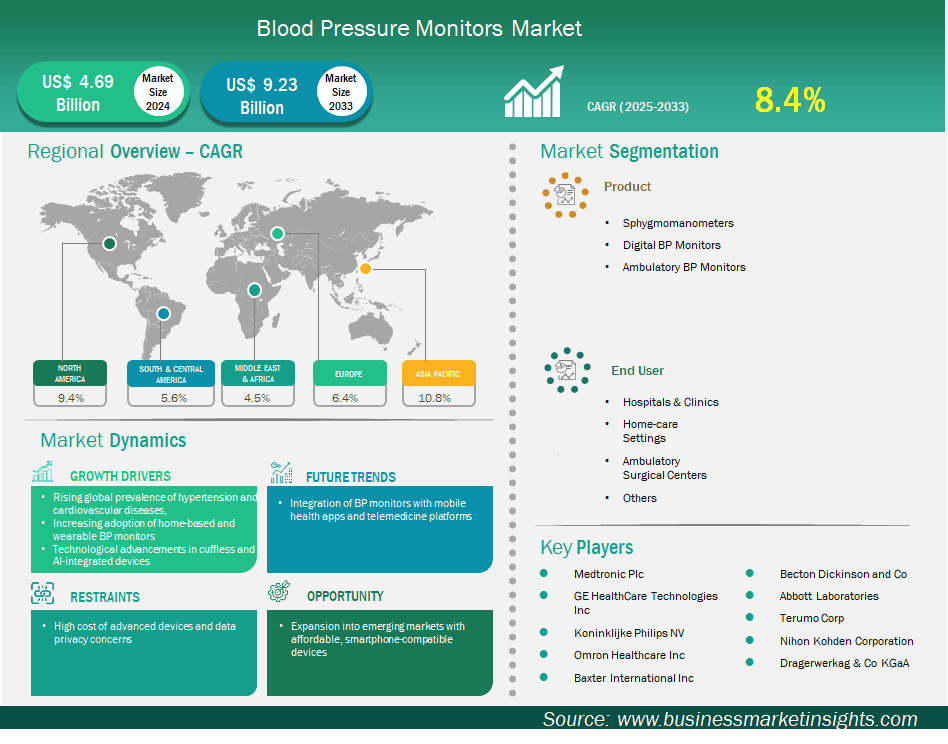

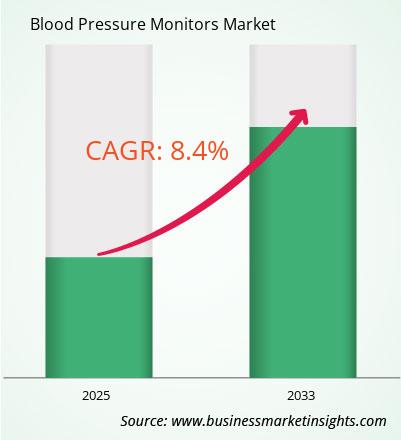

Der Markt für Blutdruckmessgeräte dürfte von 4.691,67 Millionen US-Dollar im Jahr 2024 auf 9.256,01 Millionen US-Dollar im Jahr 2033 anwachsen. Von 2025 bis 2033 wird für den Markt eine durchschnittliche jährliche Wachstumsrate (CAGR) von 8,4 % erwartet.

Der globale Markt für Blutdruckmessgeräte verzeichnet ein starkes Wachstum. Dies ist auf die weltweit steigende Prävalenz von Bluthochdruck und Herz-Kreislauf-Erkrankungen, die zunehmende Nutzung von tragbaren Blutdruckmessgeräten für den Heimgebrauch und den technologischen Fortschritt bei manschettenlosen und KI-integrierten Geräten zurückzuführen. Zu den Blutdruckmessgeräten gehören Blutdruckmessgeräte, digitale Blutdruckmessgeräte und ambulante Blutdruckmessgeräte. Der globale Markt für Blutdruckmessgeräte befindet sich aufgrund des weltweiten Anstiegs von Bluthochdruck und dessen Auswirkungen auf die wachsende ältere Bevölkerung sowie des zunehmenden Wissens über die Vorteile von Blutdruckuntersuchungen als Teil der präventiven Gesundheitsversorgung bereits in einer Phase hohen Wachstums.

Einer der Trends ist die zunehmende Verlagerung hin zur Heimüberwachung. Grund dafür sind der zunehmende Komfort und die Kosten der Technologie sowie die Verfügbarkeit intelligenter und tragbarer Blutdruckmessgeräte mit drahtloser Datenübertragung und Telemedizin-Datenaustausch. Traditionelle, nicht-intelligente Geräte haben aufgrund ihrer geringeren Kosten und ihrer größeren Verbreitung weiterhin einen größeren Marktanteil. Die wichtigsten Akteure, die diese Strategie verfolgen, bauen ihre Produktionskapazitäten aus und entwickeln KI-Integrationen, Multiparameter-Geräte und Wearables, um der steigenden Nachfrage und den sich wandelnden Verbraucherpräferenzen gerecht zu werden.

Wichtige Segmente, die zur Ableitung der Marktanalyse für Blutdruckmessgeräte beigetragen haben, sind Produkt, Anwendung und Endbenutzer.

The increase in use of home-based and wearable blood pressure monitors is driven by the rising global prevalence of hypertension and, at the same time, changing expectations for preventive and self-managed health care. These devices provide unparalleled convenience, portability, and ease of BP measurement, together with the ability to routinely measure BP outside the clinical setting, and this can improve early detection, adherence to medication, and proactive management of health. The advantages of technology through wireless connectivity, smartphone applications and the ability to share with cloud storage provides real-time tracking for the remote-monitoring and real-time refiling of data, enables timely interventions and development of personalized treatment plans, and alleviates some of the burden of our healthcare systems and allows for patients to take charge of their own health.

Advancing this paradigm shift is the use of smart technology, which allows wireless data transfers to smartphone apps or cloud platforms via Wi-Fi or Bluetooth. This connectivity supports remote patient monitoring (RPM) by healthcare practitioners, allowing for timely interventions, treatment changes, and proactive management of chronic diseases, such as having patients who have hypertension "controlled." In addition to improving patient engagement with their treatments and adherence to a treatment plan, RPM dramatically decreases the burden of patient visits to health centres, which lowers costs, enhances quality of life, and transforms BP measurement from a clinical experience to a home and wearable patient-centred experience, and BP measurement is also becoming integrated into patient-centred healthcare delivery with the impetus being shifted away from traditional clinic-centred healthcare delivery.

Leveraging the ongoing expansion of emerging markets, especially when packaged with affordable, smartphone-compatible devices, is an important opportunity for the blood pressure monitors category. A growing number of low- and middle-income countries are experiencing a rapidly increasing burden from hypertension because of increasing lifestyle changes and an aging population, but have very limited healthcare systems and low capacity for routine clinical monitoring. By providing affordable and easy-to-use devices that can integrate with the proliferation of smartphone ownership in emerging markets, manufacturers can reach a widely underserved and vulnerable population and enable widespread self-monitoring and early detection of hypertension - effectively filling a critical public health need. This allows businesses to tap into new revenue, as well as new market opportunities for growth.

Additionally, increased adoption of telehealth and remote patient monitoring technology in these emerging markets is another expansion opportunity for smartphone compatible blood pressure monitors. Many of these emerging markets will continue to see a trend with 3rd party vendors providing telehealth support to hospitals and/or health ministries. When using a smartphone compatible blood pressure monitor, routine blood pressure indices can be gathered without the need to visit clinics, improving disease management, medication adherence and personalized care beyond access in areas where clinics may be limited, without reliance on limited human healthcare resources.

The blood pressure monitors market is classified according to products into sphygmomanometers, digital BP monitors, ambulatory BP monitors. The digital BP monitors segment led the market in 2024 and beyond. Digital blood pressure monitors occupy largest share of the blood pressure monitor market as a result of ease of use, accuracy, and technological change suited for both professional and home use. Because of its ease of use and the minimal training involved compared with a manual sphygmomanometer, self-monitoring at home with a digital device is less challenging. Digital blood pressure monitors are also quicker to read and the digital readings are clear and easy to understand. The memory feature, which allows users to take and store multiple readings in the digital device itself, is of great value. The device also has a lower chance of human error in reading blood pressure results or inflating cuffs. There is also continued technological development that allows Bluetooth connectivity, app usage, and cloud-based sharing that allow remote patient monitoring and automatic transmission to providers. The continued rise of hypertension globally, and the improved recognition of the purpose of self-monitoring as part of preventive care overall, accounts for the increase in consumer preference for more convenient and increasingly accurate digital devices, including upper-arm digital monitors which are the most trusted for clinical-grade accuracy.

By end user, the market is segmented into hospitals and clinics, home-care Settings, ambulatory surgical centers, others. The hospitals and clinics segment held the largest share of the market in 2024. This is owing to the large number of patient encounters, the critical need for accurate and ongoing surveillance in acute care locations, and the contributions of acute care locations in developing an initial diagnosis and starting treatment. There are a wide variety of patients encountered in acute care locations, from regular check-up visits to the critically ill, and all patients referred can expect an assessment of their blood pressure for the purposes of diagnosis, treatment monitoring, and follow-up of diagnosed chronic conditions like hypertension and cardiovascular disease.

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 4,691.67 Million |

| Market Size by 2033 | US$ 9,256.01 Million |

| Global CAGR (2025 - 2033) | 8.4% |

| Historical Data | 2022-2023 |

| Forecast period | 2025-2033 |

| Segments Covered | By Product

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

|

The "Blood Pressure Monitors Market Size and Forecast (2021–2031)" report provides a detailed analysis of the market covering below areas:

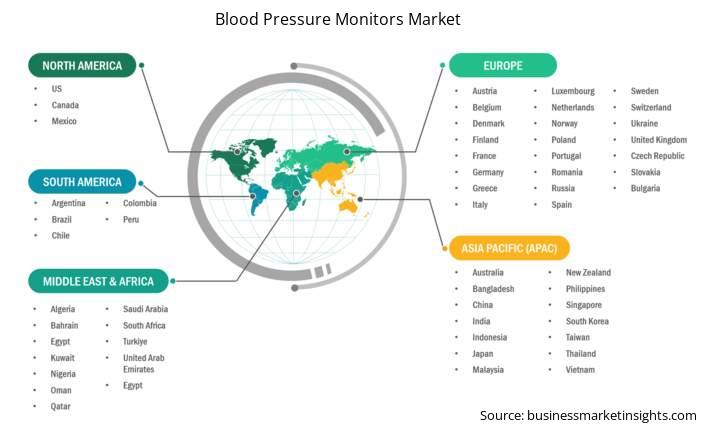

The geographical scope of the blood pressure monitors market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Blood Pressure Monitors market in Asia Pacific is expected to grow significantly during the forecast period.

Asia Pacific blood pressure monitors market includes China, Japan, India, South Korea, Australia, Bangladesh, New Zealand, Philippines, Singapore, Indonesia, Taiwan, Malaysia, Vietnam, and the rest of Asia Pacific. The combined factors of a large elderly population affected by hypertension, changing lifestyles leading to a rise in cardiovascular disease rates, and increasing awareness around preventive healthcare, mean that the Asia Pacific region is quickly becoming the fastest-growing market for blood pressure monitors. Improvements in healthcare infrastructure in the region, spending on healthcare, government-driven initiatives to promote the use of advanced medical devices, and home health management solutions are all contributing to the rapid growth of the blood pressure monitor market in the Asia Pacific region. The emergence of a middle-class with affordable disposable income for health-conscious purchases has led to an increase in the demand for portable and accessible health monitoring, which will increase the consumption of blood pressure monitors.

China is an important market within the Asia Pacific region, with many anticipated growth opportunities due to its large population and large burden of hypertension. China has experienced a rapid increase in the uptake of automated/digital and ambulatory blood pressure monitoring, and enhanced consumer awareness, advances in technology, and consumer preference for homecare solutions will likely continue to fuel growth. India is also growing strongly, especially in the home blood pressure monitoring devices market. Continued growth in India is expected to be driven by growth in awareness on health.

The blood pressure monitors market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Blood Pressure Monitors market are:

The Blood Pressure Monitors Market is valued at US$ 4,691.67 Million in 2024, it is projected to reach US$ 9,256.01 Million by 2033.

Laut unserem Bericht „Markt für Blutdruckmessgeräte“ wird das Marktvolumen im Jahr 2024 auf 4.691,67 Millionen US-Dollar geschätzt und soll bis 2033 9.256,01 Millionen US-Dollar erreichen. Dies entspricht einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von etwa 8,4 % im Prognosezeitraum.

Der Marktbericht für Blutdruckmessgeräte deckt in der Regel diese Schlüsselsegmente ab:

Der historische Zeitraum, das Basisjahr und der Prognosezeitraum können je nach Marktforschungsbericht leicht variieren. Für den Marktbericht zu Blutdruckmessgeräten gilt jedoch:

Historischer Zeitraum: 2022–2023Basisjahr: 2024Prognosezeitraum: 2025–2033Der Markt für Blutdruckmessgeräte wird von mehreren wichtigen Akteuren bevölkert, die jeweils zu seinem Wachstum und seiner Innovation beitragen. Zu den wichtigsten Akteuren gehören:

Medtronic PlcGE HealthCare Technologies IncKoninklijke Philips NVOmron Healthcare IncBaxter International IncBecton Dickinson and CoAbbott LaboratoriesTerumo CorpNihon Kohden CorporationDragerwerkag & Co KGaADer Marktbericht zu Blutdruckmessgeräten ist für verschiedene Interessengruppen wertvoll, darunter:

Grundsätzlich kann jeder, der an der Wertschöpfungskette des Marktes für Blutdruckmessgeräte beteiligt ist oder eine Beteiligung daran in Erwägung zieht, von den Informationen eines umfassenden Marktberichts profitieren.

E 1803, Panchshil Towers, Vagholi, Haveli, Pune- 412207, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For Blood Pressure Monitors Market

Get Free Sample For Blood Pressure Monitors Market